AI glasses are coming for your smartphone… how to invest… a headwind and tailwind pushing on today’s market… why the crypto market has been sucking wind… the key “bull-or-bear?” level to watch

META is one of the Magnificent 7 and a nearly $2 trillion company.

It could double from here…

But if so, it won’t happen by selling more ads or tweaking a newsfeed. Instead, it’ll be a result of owning the next computing form factor – AI smart glasses.

If CEO Mark Zuckerberg’s bet on these AI glasses pays off, the tech giant could enjoy growth rates reminiscent of early Facebook days as it replaces (or at least somewhat displaces) the smartphone – and benefits from the redirect of the nearly $600 billion global smartphone market.

This is the broad setup that veteran trader Jonathan Rose just highlighted:

It’s really not a question of if AI smart glasses will finally have their iPhone moment.

At the rate consumers are buying them up, they could replace or at least displace the smartphone as our primary interface over the next decade.

When that happens, investors who see it early are the ones who will capture all the generational upside.

But while META investors would love a 100% gain from here, Jonathan says the portfolio-transforming returns will be found elsewhere:

The truth is, META may be selling the goods – but the real opportunity lies with a whole wave of stocks powering the key tech behind these devices.

The strategy to parallel the smartphone rollout

Jonathan points to a supply chain that mirrors the early iPhone era when component makers delivered the true 10-baggers:

Here are the major picks I’m watching right now:

- Core Silicon: Qualcomm (QCOM) supplies the Snapdragon AR1 platform already inside Meta’s glasses.

- Optics & Eyewear: EssilorLuxottica ADR (ESLOY) manufactures and distributes Ray-Ban and Oakley frames.

- Audio & Voice Interface: Knowles (KN), Cirrus Logic (CRUS) — MEMS mics and audio processors.

- Connectivity: Skyworks (SWKS), Qorvo (QRVO) — RF front ends for Wi-Fi/Bluetooth.

- Displays: Kopin (KOPN) — micro displays, speculative but leveraged to HUD adoption.

- Materials: Corning (GLW) — specialty glass and optics for future display models.

- Cloud AI Backbone: NVIDIA (NVDA), Broadcom (AVGO), Marvell (MRVL), AMD (AMD) — the data-center muscle behind multimodal AI.

(Disclosure: I own QCOM, GLW, and AMD.)

Jonathan notes that Nvidia is probably the only name on this list the average Main Street investor recognizes – the rest are virtually invisible.

And that’s exactly the point: These are the biggest supply-side players in the space, and Jonathan argues the real multi-bagger potential lies here.

When everyday investors finally catch on and start pouring in, these overlooked stocks could see explosive gains over the next few years.

Two approaches to profiting from the AI smart glasses ecosystem

The “make it simple” version is to create a basket of likely AI smart glasses winners that represent the broad ecosystem, invest equally across the entire opportunity set, then hang on.

Some may fizzle, others may post solid returns but nothing mind-blowing, and hopefully, you’ll find yourself in the one or two picks that become the 10X (or even greater) winners of tomorrow.

The other approach is to trade these AI suppliers, waiting to put your money down until you see specific money flows that suggest a big move is imminent.

This is Jonathan’s preferred method. He tracks the options market looking for Unusual Options Activity (UOA). He built a scanner to detect unusually large options trades – often the footprints of institutional players placing high-conviction bets.

Time and again, these trades have foreshadowed major price moves before they hit the mainstream radar. For traders who see them, and position themselves accordingly, it can result in fast triple-digit trading returns.

Back to Jonathan:

It happened in Broadcom before the iPhone boom. And make no mistake: I expect it to happen again in the stocks fueling this big moment for AI glasses.

Names like KN, CRUS, KOPN, GLW, SWKS, QRVO aren’t crowded. They’re overlooked — until the smart money tips its hand.

With UOA, I’ll see it first, and I’ll bring it to you.

Unusual Options Activity is at the heart of Jonathan’s trading service Advanced Notice, which you can learn more about here.

And if you’d like to get a better sense of Jonathan and how he views market opportunities in general, join him for his daily Masters in Trading: Live episodes, each day the market is open at 11:00 a.m. Eastern. They’re full of ideas, specific stocks to consider, and best of all, they’re free! You can learn more right here.

Circling back to AI smart glasses, if this is really the device that overtakes the smartphone, I don’t need to tell you how big this will be.

Invest accordingly.

Tracking today’s late-inning bull market

In yesterday’s Digest, we launched a “Crazy Map” to help track how long to ride today’s bull market before exiting to sidestep the worst of the eventual bust. As part of this, over the coming months, we’re going to highlight various market tailwinds and headwinds.

Tom Yeung, Eric Fry’s lead analyst in Fry’s Investment Report, just flagged a tailwind that might not seem so bullish on the surface…

Today’s all-time highs.

From Tom:

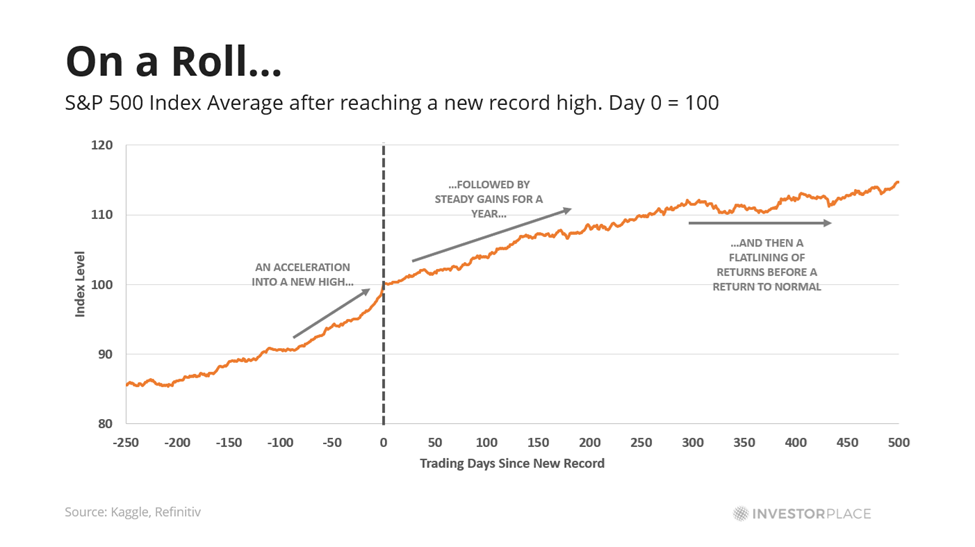

I’ve reviewed S&P 500 data since 1927 and recorded each instance where the U.S. index hit a new all-time high.

To prevent double-counting, record highs within 12 months of another one are ignored. So, if the S&P 500 hit a new record on April 4, and then another one on April 5, only the first date is counted.

That leaves us with 35 instances of new S&P 500 records from the past century. And here’s what the average return looks like over the following two years (roughly 500 trading days).

The graph above clearly shows an acceleration into a new record high, followed by a steady one-year return of 9.9% between trading day 0 and 252. Stocks then flatline for a while before returning to normal growth rates.

So, on average, buying at fresh record highs is great for your wallet.

In past Digests, I’ve highlighted work from Meb Faber, a quant specialist and CIO at Cambria Investments, who’s reached a similar takeaway. Meanwhile, William O’Neil, who founded Investor’s Business Daily and created the very popular swing-trading system known as CANSLIM, had a quote on the topic:

It is one of the great paradoxes of the stock market that what seems too high usually goes higher and what seems too low usually goes lower.

But yesterday also brought a “headwind”

The Wall Street Journal ran a piece highlighting how the credit market has Wall Street on edge:

U.S. credit markets are running hot—maybe too hot.

Investors are gobbling up corporate debt like it is going out of style—even though the rewards, by some measures, are lower than they have been in decades.

The frothy mood has some on Wall Street worried that the market is priced for perfection and ripe for a fall.

The piece points toward the growth of lending to riskier borrowers in recent years, stating:

The longer that credit boom lasts, the more likely it is that defaults will rise.

Likewise, the higher the valuations of corporate bonds and loans, the more susceptible they become to selloffs.

The risk this poses to the investment markets

The big problem with today’s hot credit market starts with the added risk that investors are taking. The additional return they’re getting for holding bonds over “risk free” U.S. Treasuries is near all-time lows.

Back to the WSJ:

The overarching concern on Wall Street is that the exceptionally high valuations for corporate debt are concealing excesses in the market and insufficiently compensating investors for taking risks.

[The spread between investment-grade corporate bonds and U.S. Treasurys] fell to 0.74 percentage point in September, its lowest level since 1998, according to ICE Data Indices.

The spread for junk-rated bonds is about 2.75 percentage points, near the record low set in 2007.

That alone isn’t comforting. But the real danger is how investors are financing these bets – with borrowed money.

We pointed toward this risk in yesterday’s Digest where we highlighted some “Crazy Map” milestones – one of which was “easy money and leverage”:

Margin debt and other forms of borrowing surge, ramping up today’s gains while setting the stage for tomorrow’s trainwrecks.

Strictly speaking, margin debt tracks equities, not bonds. Still, the concern is broader: leverage, whether through repos, derivatives, or credit lines, is being used to juice bond returns.

Barron’s underscored this with comments from Deutsche Bank credit strategist Steve Caprio, who tracks equity margin debt as a sentiment gauge:

“We care about margin debt, as it is a useful gauge of when market sentiment is on the verge of going from ‘red-hot’ to ‘white-hot’” …

“We have tracked this indicator for years now, but only have written on it today, given that the rate of increase is starting to flag as ‘too hot’ by our metrics.”

Caprio’s team may focus on credit, but they see equity margin debt as a proxy for the kind of euphoria that spills over into bonds as well.

Stepping back, we have one point for bulls with stocks at all-time highs – and one point for bears with leverage fueling much of those gains.

Our takeaway: Stay with the strongest corners of this market but recognize the risk.

This is what Tom and Eric are doing. Back to Tom:

We believe that there are still more gains to be had, especially in fast-growing sectors like artificial intelligence.

That’s why Eric, along with InvestorPlace analysts Louis Navellier, Luke Lango, put together the Day Zero Portfolio. This portfolio holds a carefully selected group of companies that are exposed to the next wave of AI exponential progress, giving those with access targeted exposure as well.

Sticking with the risks of leverage…

Crypto has been acting poorly in recent sessions – and part of it has to do with bad, leveraged bets getting unwound.

Let’s go to our crypto expert Luke Lango:

Wall Street was nearly certain coming into [last] week that the Federal Reserve would cut rates again in October.

Then got stronger-than-expected economic and labor market data, including a huge upward revision to second-quarter GDP and the weakest jobless claims numbers we’ve seen in months…

The 10-year Treasury yield simultaneously popped back up to 4.2%.

Remember: crypto is the definition of a long-duration asset… Future values get discounted harder when yields rise, putting pressure on today’s prices.

And once Bitcoin started to slip, the dominoes fell fast. The crypto market is always heavily levered. That means even small pullbacks can snowball into large liquidations.

[Last] week’s cascade of forced selling turned a modest macro repricing into a full-on selloff.

This Digest is running long, so let me jump to Luke’s takeaways for investors…

The recent crypto selloff isn’t due to fundamentals. It’s a reaction to the Fed, bond yields, and leverage. It’s a reset – not the end of this crypto cycle.

Luke says to watch the 200-day MA which is just above $104,000. This is the line in the sand that separates bull markets from bear markets:

If BTC bounces there, dip-buyers will likely rush in, and the “healthy reset” narrative will gain traction.

If it breaks, algorithms could force a sharper flush toward $100K or even $95K–$97K.

Luke is betting on a bounce as this setup looks more to him like a correction than a collapse. We’ll keep tracking this and will report back.

Have a good evening,

Jeff Remsburg