2025 was supposed to be the year AI finally took over everything.

Every major AI champion from Sam Altman to Elon Musk was making the same pronouncements about AI’s immediate future.

Entry-level positions handled by AI. AI handling in mere seconds tasks that would typically take humans hours to complete. And the big dream – artificial general intelligence (AGI) right around the corner.

You could connect the dots pretty easily. Beyond-human intelligence everywhere. Humans becoming obsolete.

For the biggest players, all of these pronouncements seemed like dogma delivered by the AI gods. And the markets absolutely ate up all the hype.

Surging valuations for AI stocks have dominated the headlines. Hyperscalers (AI infrastructure and cloud providers) like Nvidia are gobbling up more and more market share. And an ever higher global concentration of stocks are riding the AI wave as I write to you.

In short, we’re seeing what looks like an AI bubble taking shape similar to the one we saw during the original wave of dot-com startups. And just like that moment, the markets are minting AI winners and losers as I write to you.

In the past six months, I’ve helped readers capture double- and triple-digit gains from both major AI names and smaller, overlooked players.

AI’s moment is coming. But it hasn’t turned into the huge, world-changing year many people thought it would be.

We didn’t see robots taking everyone’s jobs or super-smart computers suddenly running everything. Still, we are seeing the early signs of something much bigger starting to unfold — a structural shift that will reshape industries far more profoundly than the hype cycles suggested.

AI is forcing a complete rethink of the future of work and income.

And here’s what’s really happening: it’s part of a much larger economic shift that’s unfolding faster than markets, policymakers, or most investors realize.

Which means practically nobody’s positioned for it… yet.

The Labor Market Is Already Showing Signs of Structural Stress

Just how fast is this shift happening?

Consider the biggest headlines over the last year alone

Amazon cut 14,000 corporate roles – its largest corporate layoff of 2025.

Verizon eliminated 13,000+ jobs, citing modernization and automation.

IBM is slashing back-office roles and freezing hiring wherever AI can handle repetitive tasks.

And those are just the headline names…

Over 4,200 more companies announced layoffs or hiring freezes this year as AI becomes a bigger part of their operations.

The institutions are validating this shift, too. The United Nations’ International Labour Organization (ILO) warns that clerical and cognitive tasks are highly exposed to generative AI. The ILO for Economic Co-operation and Development also confirms “renewed concern” about displacement in AI-exposed jobs

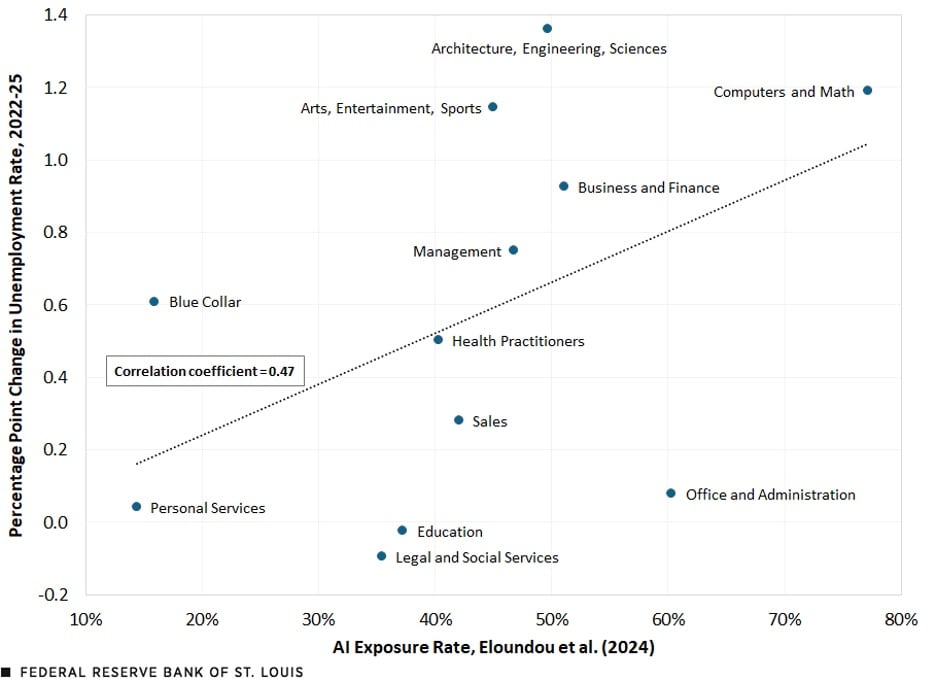

And the St. Louis Fed is studying AI as a driver of rising unemployment risk. Its findings? Just take a look at the chart below:

This chart shows sectors where higher AI exposure led to larger unemployment between 2022 and 2025.

Computer and mathematical occupations – predictably among the most AI-exposed – saw some of the steepest unemployment rises. Meanwhile, blue-collar jobs and personal service roles experienced relatively smaller increases.

So the short-term effects are already playing out. That tells us this shift in the future of work is already well underway.

Those figures above might trigger some hand-wringing. But I don’t want us to lose sight of the key opportunity emerging here. This is actually where it gets interesting for investors.

Yes, AI will displace workers. But I don’t see it taking humans out of the equation entirely.

AI’s real value comes from helping us, not replacing us. Workforce retraining and income stabilization will become larger pillars of the new economy taking shape under AI.

And for traders? This paradigm shift creates a major, underappreciated, and investable macro trend.

We’ve already banked early gains on AI’s mass market moment. Last year, we collected over 200% and 400% gains trading C3.ai – one of the biggest AI startups out there.

We’ve also hit massive triple-digit winners on the supply side – pure metals plays like The Metals Company (TMC) and MP Materials (MP) that are fueling the AI build-out.

In 2026, the opportunity gets even bigger for us. And for everyone reading this, the time to act is now.

I recently went live with a special webinar called The Profit Surge Event. I designed it to show you exactly how to systematically track hidden infrastructure plays and pair them with a simple tweak that can multiply the payoff on great stock ideas.

AI is one of the biggest sectors I’m watching right now. With this event, I’m giving you the tools to profit from the biggest gains in AI right now. You can learn all about the system – and my key stock picks – right here.

I’ve shown you a little of how AI is transforming work. And I’ve explained just how big the structural shift we’re seeing could be for early investors.

Now, let me show you how monetary policy and money itself are being transformed by AI’s mainstream moment.

The Fed’s Tools Don’t Work for This Problem

The Federal Reserve has a well-known dual mandate: Maximum employment and price stability.

And in order to carry out that mission, the Federal Open Market Committee (FOMC) has two levers it can pull on:

- Interest rates — raising or lowering the amount of interest charged on its loans to encourage or discourage borrowing.

- Balance-sheet operations — buying or selling bonds to add money into the financial system or take some out, making it easier or harder for banks to lend.

These tools work because they influence the cost of borrowing money.

So when the economy slows or unemployment rises, the Fed cuts rates.

Access to cheaper capital encourages businesses to borrow, invest, expand and hire workers to make it possible… At least, that’s how it used to work.

But this is the kernel of a growing problem — that playbook assumes companies need people to grow… But in a world increasingly built on AI and automation, that assumption is starting to fall apart.

Cheap Capital Doesn’t Create Jobs in an AI Economy

If the Fed cuts rates today, there’s little doubt it will make life easier for businesses…

But now, instead of scaling operations that require more manpower to grow, lower rates push companies to scale the systems that aim to replace workers in the long-term.

Instead of buildings full of new employees buzzing away the work day, AI gives us warehouses full of servers whirring away 24/7.

Every dollar of cheap capital becomes a dollar that accelerates automation.

That means the Fed has a bigger problem on its hands that it can’t fix with its usual tactics.

Rate cuts might shore up markets during a recession, boost earnings, improve balance sheets, and lift stock prices. But they can’t fix a structural reset like what AI is causing.

AI won’t return the clerical jobs it has already replaced.

Robotics won’t reopen the logistics roles it has made unnecessary.

Machine-learning systems won’t give back the administrative positions they’ve taken over.

What we’re seeing right now is early-stage job disruption visible across 2025 labor data.

Long term? The most valuable work won’t disappear. Like I said, workforce retraining and automation will help upskill workers for the AI era.

Still, displacement is a huge concern that will only grow from here. And that’s where the next factor comes in that’s pushing us toward a whole investing megatrend few are aware of.

The World Is Going Digital – And It’s Already Happening

It isn’t just physical labor getting phased out. Physical money is steadily getting pushed aside for completely digital transactions.

The worldwide transition to fully digital money rails is quietly reshaping how income and payments work. And as this digital transition happens, it’ll provide the fiscal support needed for the labor market shift I’m telling you about.

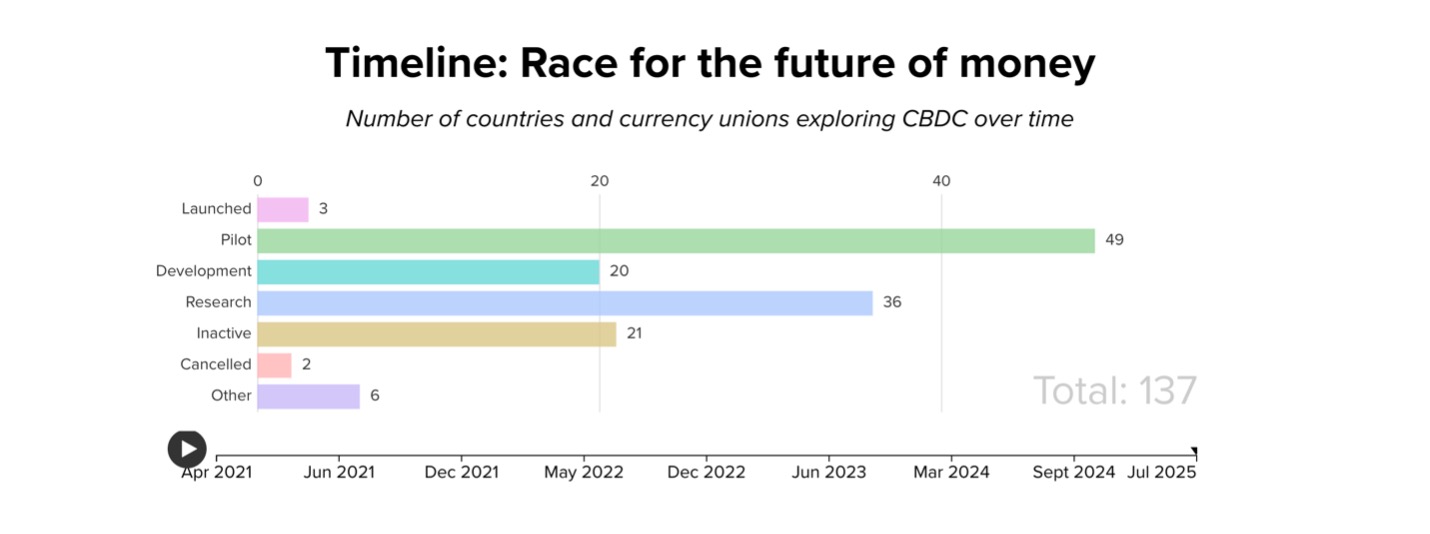

At the center of this new monetary architecture sits the most important shift of all: Central Bank Digital Currencies. Think of it as digital currency pegged to a country’s economy – like a completely digital dollar or digital euro.

Right now, over 130 countries are exploring or piloting CBDCs. Cross-border CBDC networks from El Salvador to China are already operational. Digital identity and wallet systems are also rolling out globally.

Bodies like the International Monetary Fund (IMF) are pushing tokenization and real-time settlement standards as I write to you.

And we’re seeing the same shift right here at home.

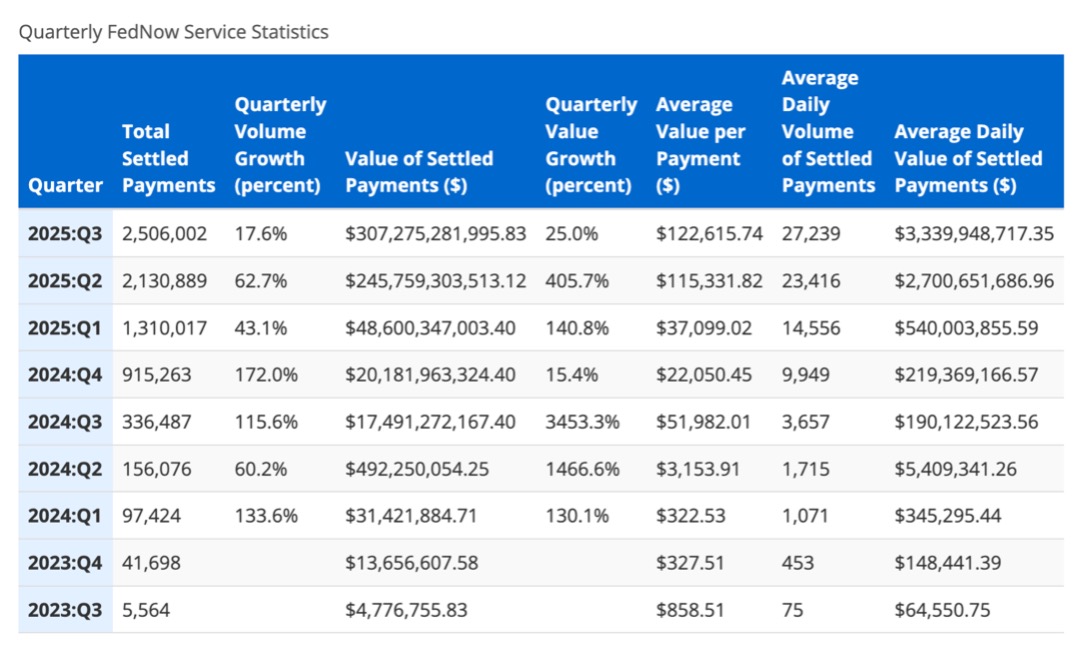

In July 2023, the Federal Reserve launched FedNow, a 24/7 instant-payment network that lets banks send and settle money in real time. It’s not a CBDC, but it is the new digital plumbing the U.S. financial system will run on going forward — the foundation for instant, fully digital money movement.

It lets banks and credit unions send and settle payments instantly — not in hours or days, like ACH or traditional bank transfers. It’s designed to modernize the U.S. payment system and create the foundation for real-time digital transactions nationwide.

It’s not just government rails being built.

While retail CBDC proposals face political resistance, private-sector digital rails – Visa, Mastercard, PayPal, fintech processors – are already making this shift possible.

And they’re best positioned to become the practical distribution layer for any future income-support mechanism.

The digital plumbing for large-scale income distribution exists now. That’s true even if the public narrative hasn’t caught up.

Here’s How This All Connects

With AI accelerating structural unemployment, it’s becoming obvious that monetary policy isn’t enough to steady the ship.

So what else could it take to start stabilizing the system? One potential solution is to use the new digital infrastructure to deliver direct fiscal income support.

It could take many different forms — a minimum income floor, wage-stabilization programs, automation offsets for the fields hit hardest by AI, emergency income payments, even something framed as a “Freedom Credit” or “Automation Dividend.” The terminology will vary, but the underlying mechanism will be the same.

As income support moves across digital rails, electronic money flows will rise, and the value will concentrate in the companies that operate those rails.

These rails include payment networks, instant-settlement processors, digital identity engines, and verification layers — the infrastructure that will carry the next generation of money movement.

And here’s what most investors haven’t priced in: the companies controlling this infrastructure are dramatically undervalued relative to the potential role they’re poised to play.

Who Benefits From This Shift?

You’ve already heard about players like Visa, Mastercard and PayPal. And while all those names are great ways to gain exposure to this trend, digital-first platforms like Coinbase also represent another major landgrab for readers.

In my view, Coinbase is quietly becoming one of the most important publicly traded companies tied to U.S. digital-dollar infrastructure. One of its core revenue engines is the stablecoin USDC, and that comes with multiple streams: payment flows, reserve income, institutional custody, settlement — the whole stack.

And if you’re new to this, stablecoins have effectively become the private-sector version of a retail CBDC in the United States. They’re already doing the job long before the government gets there.

So if income support goes digital — and the rails carrying those payments run through private platforms — the companies issuing and moving digital dollars become structural winners. Coinbase is right at the center of that architecture.

Remember, this all sits inside a global payments ecosystem worth $2.4 trillion today. McKinsey expects it to reach $3.1 trillion by 2028, and that projection doesn’t even include digital income-support flows.

Layer in recurring income delivered digitally, and the economic impact gets much larger — and so do the opportunities for the companies powering those rails.

Why You Need to Act Now

System-level changes don’t announce themselves. They surface in the numbers first, then in the flow, and finally in the price action.

We’ve got job disruption. A central bank that can’t address it. And global digital money rails expanding rapidly.

The value these companies offer as AI and money converge isn’t reflected in their valuations yet. It’s a highly asymmetric setup the markets aren’t seeing right now.

The way I see it, what we’re witnessing is a massive disconnect between today’s pricing and tomorrow’s economic architecture.

We have a chance to be early on the biggest macro shift of the coming decade.

The political resistance trying to hold things back won’t last forever. They’ll become the practical distribution layer for future income-support mechanisms.

The digital plumbing is already built. And while the spotlight stays on AI, there’s a deeper shift underway that many investors simply haven’t connected to the broader macro story yet.

Make no mistake – institutional traders are building huge stakes in companies like Coinbase and other private firms offering digital payment architecture.

That gives us an opportunity to get in on the ground floor of this revolution before the market fully appreciates the scale of what’s coming.

But recognizing the shift is just the first step.

The real edge comes from knowing how to turn a structural thesis into a structured trade. I’m talking about trades with defined risk and asymmetric payoff. And a framework that keeps you from getting shaken out when volatility hits.

Over the last year, I’ve helped members of Masters in Trading capitalize on the biggest shifts happening in everything from AI to quantum.

I want everyone reading this to have the same tools to spot huge structural shifts like we’re seeing with AI and currency before they happen.

That’s why I recently went live with something very special – The Profit Surge Event.

I showed everyone who signed up how to systematically track those hidden infrastructure plays and pair them with a simple tweak that can multiply the payoff of great stock ideas.

I even invited three of the most respected stock pickers in the business — Louis Navellier, Eric Fry, and Luke Lango — to highlight their highest-conviction names.

We walked through how this approach has historically turned strong recommendations into stronger trades.

This includes big winners that show how you can your boost profit potential by 500%-plus. I also explained why our recent track record shows average winning gains of 267% in just 36 days.

I’m reopening access to my Profit Surge Event – plus a free report with three high-conviction stock ideas the team believes are positioned for outsized upside – for free. That means you get one more chance to learn all about the key picks we’re watching. Just click here to watch the replay of the Profit Surge Event right now.

Remember, the creative trader wins

Jonathan Rose,

Founder, Masters in Trading