Hello, Reader.

Oracle Corp. (ORCL) seems to be “blessed by the Fates” this week.

The stock jumped 13% on Monday and more than 4% on Tuesday, helped by a broader, short-lived rally in software stocks and a new deal with Bloom Energy Corp. (BE), which sent that stock up 22%.

Building on an existing partnership, Oracle agreed to purchase up to 2.8 gigawatts of fuel cell power from Bloom Energy – on top of the 1.2 gigawatts already under contract and currently being deployed. These fuel cells will support on-site power generation for Oracle’s data centers and expanding AI infrastructure.

The move is unsurprising and probably a no-brainer for Oracle, as it fits neatly into its larger push into AI. But investors – and the software company itself – must remember that this progress comes with a hefty price tag…

Bloom has issued a warrant for Oracle to purchase 3.53 million shares at $113.28 each. A warrant is like a coupon that gives Oracle the right to buy stock in Bloom Energy at a fixed price. If Oracle uses the warrant, it would spend about $400 million total.

And this steep sum is just one example of Oracle’s already mountainous AI spending. So, investors should also remember that the cost of Oracle’s spending spree is more than its payments. It could be the company’s undoing.

Oracle remains well below its previous highs, and the company now has the appearance of upward momentum, or at least momentous headlines. This combination might look like an attractive opportunity to buy the dip.

But I advise caution.

In today’s Smart Money, I’ll explain why I believe Oracle to be a risky investment.

Then, I’ll point you toward more dependable, profit-generating stocks.

Let’s jump in…

The Hidden Cost of Oracle’s AI Ambition

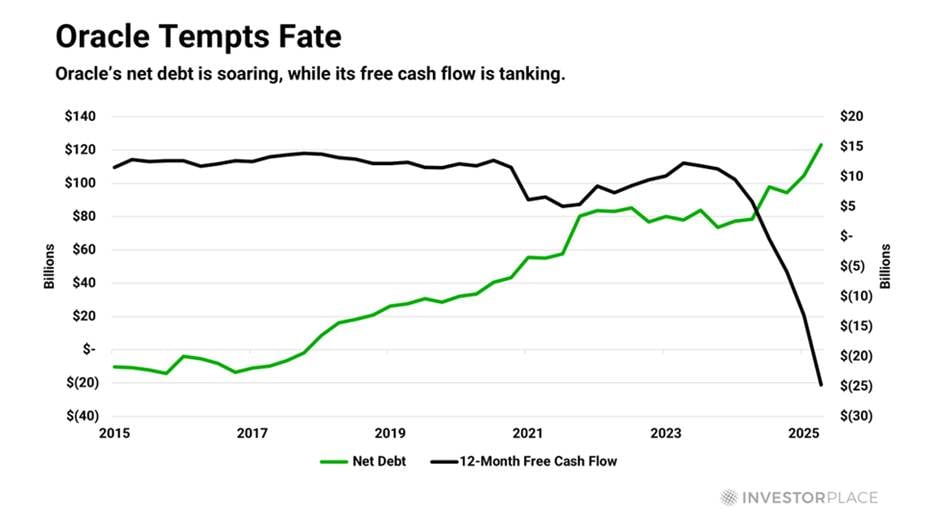

Oracle has a history of staking its future on massive AI bets – mainly AI infrastructure – which is already straining the company’s finances.

Its balance sheet now carries $120 billion in net debt and lease liabilities. Meanwhile, the company posted negative free cash flow in fiscal 2025 for the first time since 1990.

Undaunted, Oracle keeps ramping up both spending and borrowing.

One year ago, management guided to capital expenditures – the money used to grow a business or maintain existing operations – of $16 billion in the 2026 fiscal year.

Three months later, it boosted that guidance to $25 billion…

Then to $35 billion last September…

And then to $50 billion last December.

Meanwhile, the prospective profitability of the data center business Oracle is racing to build is, to put it charitably, underwhelming.

Management has guided investors toward gross margins of 30% to 40% for AI data centers, against the 80%-plus margins Oracle earns from its legacy software business.

But internal documents reviewed by The Information reveal that Oracle’s AI data center operations averaged gross margins of just 16% – lower than many non-technology retail businesses. Walmart Inc. (WMT), for instance, runs gross margins of around 24%, well above Oracle’s AI data center margins.

More troubling still, three-fifths of Oracle’s contracted backlog comes from a single customer: OpenAI – a company that, like Popeye’s Wimpy, “will gladly pay you next Tuesday for data center capacity today.”

If OpenAI cannot maintain a leading position and begin generating positive cash flow, Oracle faces the prospect of sitting atop $248 billion in lease obligations for data centers that its primary tenant can no longer fill.

Nevertheless, while Oracle insiders are running for the exits, 40 of the 50 Wall Street analysts who follow the stock rate it a “Buy.”

Such is the enduring power of “new era” narratives over “old school” risks.

But here’s why I believe Wall Street has it wrong…

Where Real Returns Are Actually Hiding

During the dot-com bubble, investors placed too much faith in technology companies’ innovations, captivated by the promise and spectacle of the future. This is similar to what’s happening today with hyperscalers like Oracle.

And you could see the enchantment in the sector’s valuations.

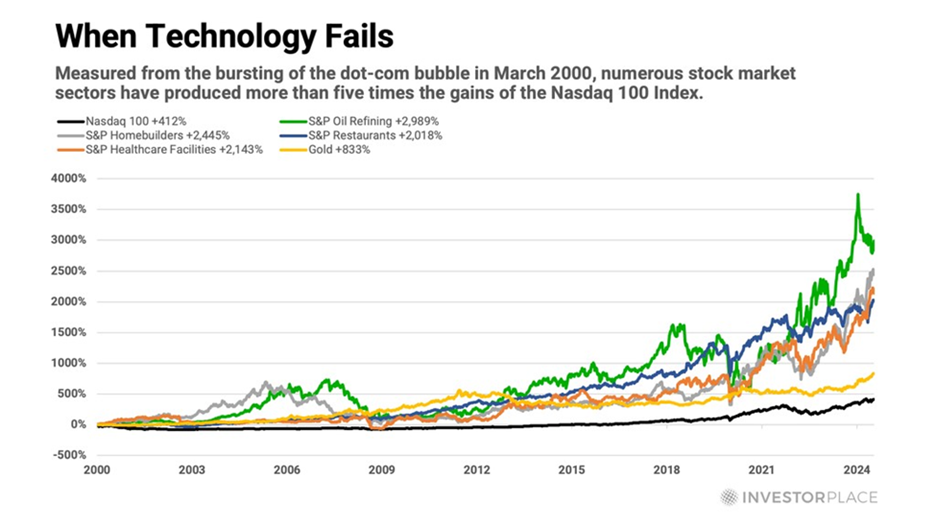

At the precise peak in March 2000, the tech-centric Nasdaq-100 index was trading for 81 times earnings! Within one year of that peak, the Nasdaq-100 had tumbled more than 70%, and it would remain a losing investment for the next 15 years.

On the other hand, any investor who paid that peak price in March 2000 and held on until 2024 would have reaped a gain of nearly 414%, or 6.9% per year.

That’s not an entirely awful long-term result, but as the chart below shows, many other sectors – specifically non-tech or traditional sectors – delivered results over that timeframe that were more than five times greater. Even gold trounced the Nasdaq-100, soaring more than 800% since March 2000.

These are the same overlooked sectors that have the potential to maximize your gains today.

Unlike Oracle, which is pouring billions into AI infrastructure with uncertain near-term returns, many “old-school” plays like commodity stocks are tied to real-world demand. These sectors aren’t risk-free, of course, but their value depends less on long-dated technological bets.

I’m talking about consumer cyclical, healthcare, energy, and gold stocks – an opportunity I just discussed in Monday’s Smart Money.

Just as in the dot-com era, today’s market is defined by high-risk, high-spending tech leaders – while more traditional sectors quietly offer stability and real earnings.

I recommend these kinds of solid plays in our Fry’s Investment Report portfolio, like…

- An independent exploration and production energy company that has delivered 41% gains in three months.

- And my newest recommendation, a medical devices company, that I recommended last Friday. The company is up following this week’s announcement of its newest analytical instruments.

Both of these companies have plenty more potential to come.

While Oracle remains crucial to AI development, its reliance on a single, capital-intensive growth driver like AI also exposes the stock to greater risk, making any misstep more likely to have an outsized impact. That is why I recommended that my readers sell the stock in November. It has fallen 20% since then.

For more information on which stocks I believe will drag down your portfolio and which can strengthen it, I recommend you watch my Sell This, Buy That broadcast.

In the presentation, I share more about the advantages of sticking to undervalued companies that are quietly driving innovation and why those dominating the headlines – like Oracle – may be tempting fate more than mastering it.

Regards,

Eric Fry