History likes to play a tricks on us. When we read about the big events over the years that shape a generation, far too often it will make it seem as though it showed up one day out of the blue.

But when you start digging into the story, most “overnight success” stories usually took years to build.

When you bring up The Beatles, most folks will point to their appearance on Ed Sullivan in early 1964 and suddenly they were the biggest band in history. But that completely ignores the six years they spent in small bars and nightclubs working their way up in the industry and the charts.

We see the same situations play out in business and finance all the time. These kind of revolutionary events don’t announce themselves.

There’s no bell ringing, no confetti on CNBC.

They build up in the background, on the fringes quietly, working their way through the plumbing of the global system. What’s sudden is the rest of us catching up and realizing everything’s changed.

That’s exactly what’s happening right now with something most investors still think of as “just crypto.” But this isn’t about Bitcoin or wild meme coins.

It’s about money itself — the way it moves, the way it earns, and the way it’s poised to transform the stock market next.

And the company at the center of it alland the story behind it might be the most important trade hiding in the market today.

The $60 Billion That Moves in an Instant

Let’s start simple.

Imagine wiring money to a friend in another country.

The bank says it’ll take three to five business days.

You shrug, but think — why? We can send a video across the planet in seconds, but not dollars?

This is the frustration that gave birth to stablecoins.

For the uninitiated, a stablecoin is a type of cryptocurrency designed to maintain a stable value, usually by being pegged to a real-world asset like the U.S. dollar, the euro, or even gold.

Here’s how they work. You give a company $100. They hold that $100 in a bank account or short-term Treasury bill (T-Bill).In return, they issue you 100 digital dollars — tokens that live on a blockchain.

Those tokens are backed one-for-one by the real cash sitting in the vault. That’s why they’re called stable coins.

They’re not trying to replace dollars. They mirror them.

Right about here you might be thinking that this is a lot of trouble to go through to buy a cup of coffee, but the real magic is in the movement: these digital dollars transfer instantly, 24/7, anywhere on earth.

No banks closed on weekends waiting for accounts to settle. No intermediaries or clearinghouses. No wire-fees. No waiting.

The entire transaction from start to finish is completed digitally in the time it takes to send a text.

And while most people still associate stablecoins with crypto exchanges, their real adoption is happening outside that world.

In Latin America, freelancers use stablecoins like USDC to escape inflation.

In Southeast Asia, importers use it to pay suppliers in hours instead of days.

Even charities have started using stablecoins to deliver aid directly to people’s phones.

Once people realized they could create a digital mirror of the dollar — a reflection that moved faster and worked smarter — the question became inevitable: what happens when the mirror starts reflecting everything?

Not just tokenizing money, but the markets themselves…

The Mirror Market Revolution on the Horizon

Stablecoins have already given us the blueprint for a kind of mirror market:

- A custodian locks up 100 shares of Apple stock.

- Against them, 100 digital Apple tokens are issued — each backed one-for-one by those real shares.

And once those tokens are minted, they can trade instantly, globally, even fractionally, and around the clock.

No settlement delays. No middlemen. No need to wait for the market to “open.”

It’s the same logic that makes USDC powerful — only this time, the mirror reflects stocks instead of cash.

Back in June, Robinhood (HOOD) gave us a preview of what that might look like.

At a European event, they tokenized small blocks of private-company shares — SpaceX, OpenAI, and others—and let customers trade them as digital tokens.

For most retail investors, it was the first chance to “own” pieces of companies usually reserved for venture capital and hedge funds. The reaction at the event was electric. The headlines? Not so much.

OpenAI quickly issued a statement clarifying it hadn’t authorized the promotion. Lawyers got involved. Regulators perked up.

But the experiment proved the concept: tokenization works.

And Robinhood isn’t the only actor experimenting with this idea…

Big banks are quietly experimenting with tokenized bonds and money-market funds.

BlackRock’s digital liquidity fund already clears trades on blockchain rails.

Even governments — from Singapore to Switzerland — are running pilots for central-bank digital currencies.

They’re not doing this because it’s trendy.

They’re doing it because the infrastructure is faster, cheaper, and global.

The big wrinkle in the setup right now is that the rulebook needs time to catch up.

To me that moment feels a lot like the early internet. Everyone can see the potential, but no one had agreed on the standards yet.

So for the time being, the “mirror market” is small compared to the traditional system. But it has the potential to explode in scale once the light flips from red to green.

Why Wall Street Can’t Ignore It

For decades, the global financial system ran on slow, paper-based infrastructure.

Even when trades went digital, the backend didn’t.

That’s why you can buy a stock in seconds but still wait two days for it to “settle.” It’s a relic of the 1970s — held together by clearinghouses, custodians, and overnight batch jobs.

Tokenization changes all of that.

It compresses the entire process into a single, programmable transaction.

That means less counter-party risk, faster liquidity, and lower costs.

For hedge funds and banks, that’s efficiency.

For retail investors, that’s opportunity.

Because once the mirror market scales, trading will no longer depend on geography, time zones, or even stock exchanges. It’ll just happen.

The Company Behind the Curtain

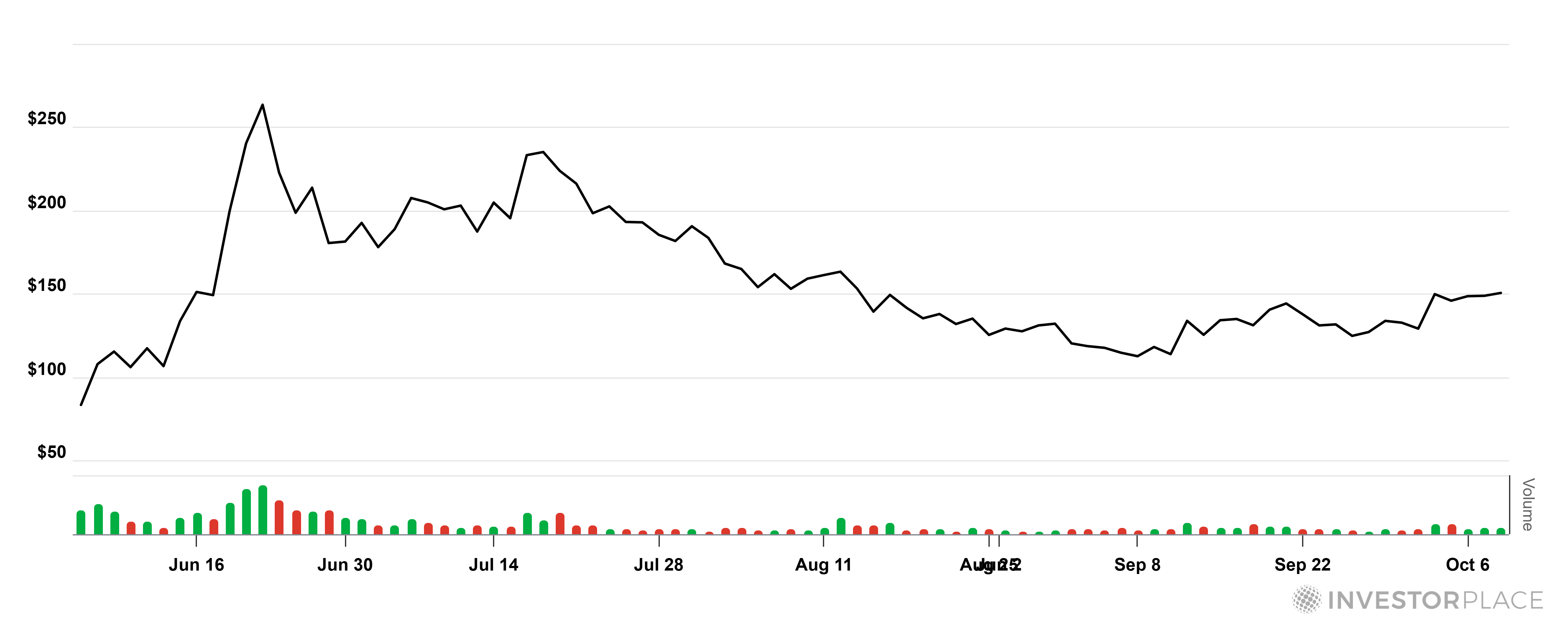

Among all the stablecoin issuers, Circle (CRCL) stands apart. Its product, USDC, is the clean-cut kid in a rough neighborhood.

It’s fully backed by cash and Treasuries. It publishes monthly attestations. And it’s favored by the kind of companies that normally keep crypto at arm’s length like BlackRock and Visa. In particular, Visa has been using USDC to help settle transactions within its payment network since 2021.

Today, there’s over $60 billion worth of USDC circulating around the world.

Each of those tokens represents one real U.S. dollar sitting in Circle’s reserves. And that pile of reserves is the secret to the company’s profitability.

Because when you’re sitting on tens of billions of customer deposits, you’re not only holding money, but earning interest.

The Quiet Cash Machine

In the second quarter of 2025, Circle reported more than $630 million in quarterly interest income. That’s not from trading or speculation. That’s from T-bills.

When the Federal Reserve holds rates near 5%, every billion dollars in reserves earns roughly $50 million a year.

Multiply that by sixty billion in USDC, and you’ve got a serious profit engine.

But here’s where things get interesting.

Those profits are tied directly to interest rates.

On one side, the Federal Reserve. When rates are high, Circle earns fat interest on its reserves.

On the other side, adoption. When crypto activity rises, demand for USDC surges — and so do reserves. That’s because all that tokenized activity still needs a stable, digital dollar to move around—and USDC is already the default rail.

So the company’s future sits at the intersection of monetary policy and digital-asset growth.

That’s why I call it the “Hidden Rates Trade.” Here’s the math behind it:

| Rate Cut | Revenue Hit | USDC Growth Needed to Offset |

| 0.25% | -$78M | +$3.8B (~6% more USDC) |

| 0.50% | -$154M | +$7.6B (~12% more USDC) |

| 1.00% | -$309M | +$15.3B (~25% more USDC) |

Think of owning CRCL as being long rates, long crypto adoption.

So if rates fall and crypto demand stays flat, we want to be bearish CRCL either by shorting the stock or going long puts.

But if rates fall and crypto demand surges we want to be neutral CRCL and look to collect premium with credit spreads or selling options against stock..

The Bottom Line

Every financial revolution looks obvious in hindsight.

Stablecoins were the proof of concept… If you can mirror a dollar, you can mirror a stock. And if you can mirror a stock, you can mirror an entire market.

That’s the world we’re moving toward — a mirror market where every real-world asset has a digital reflection that trades instantly, globally, and transparently.

Circle sits right in the center of that shift. Its business is simple on paper — issue digital dollars, hold the real ones in reserve, and earn interest on the spread. But its future depends on two powerful forces pulling in opposite directions: the path of interest rates and the pace of crypto adoption.

It’s the story of how money itself is changing — from paper to pixels, from banking hours to 24/7.

And when the rest of the world finally wakes up to it, it’ll look like an overnight success that was years in the making.

For traders who understand it early, it could be the edge of the decade.

Because soon, trading dollars, stocks, even private companies through smart contracts won’t be unusual.

It’ll be the rule.