It’s my favorite time of year: earnings season.

This is when we find out the companies that deliver… and those that don’t.

Good earnings tend to come out early, and so far, they are better than Wall Street expected.

The strategists thought earnings for the S&P 500 would decline 5.4% in the third quarter. On the other hand, the analyst community projected earnings would increase 2.4%. In my experience, the analysts are usually right.

In today’s Market 360, we are going to take a look at two highly anticipated earnings reports that were released this week: Netflix, Inc. (NASDAQ:NFLX) and Tesla, Inc. (NASDAQ:TSLA). I’ll also share where I expect the best earnings to come from in the quarters ahead…

Netflix, Inc. (NFLX)

Netflix reported earnings Tuesday after the market close.

Analysts were expecting revenue of $7.85 billion and earnings per share of $2.17 for the third quarter in fiscal year 2022. They were also looking for 1.1 million paid subscriber additions for the quarter, after losing subscribers for two consecutive quarters.

The company reported revenue of $7.93 billion and earnings per share of $3.10 during the third quarter – solidly beating analysts’ estimates.

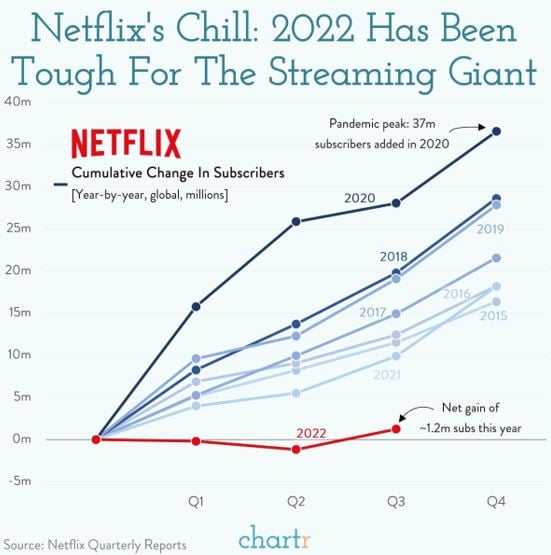

Furthermore, Netflix added 2.41 million subscribers, topping expectations. Company management also said they expect to add 4.5 million subscribers during the fourth quarter.

Much of Netflix’s recent growth can be attributed to content, specifically the popularity of Stranger Things Season 4 over the summer, the recent release of Monster: The Jeffrey Dahmer Story and Cobra Kai, which was the most-watched show on any streaming service in mid-September.

During the conference call, co-CEO Reed Hastings said, “Thank God we’re done with shrinking quarters. [It’s] a big deal to go back to positivity.”

Shares of Netflix shot up 14% in after-hours trading.

The fact is, even with subscriber growth picking up, Netflix still has growing competition, mainly from The Walt Disney Company’s (NYSE:DIS) Disney+ and Warner Bros. Discovery, Inc.’s (NASDAQ:WBD) HBO Max.

But even with Netflix’s third-quarter growth and fourth-quarter projections, the streaming giant is growing at its slowest pace.

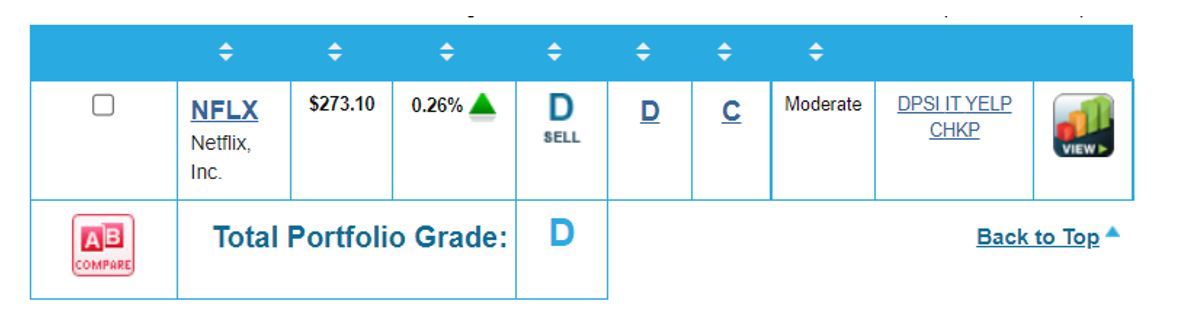

Taking a look at Portfolio Grader, the company still has a D-rating, indicating it’s time to sell if you haven’t already.

Tesla, Inc. (TSLA)

When I last talked about Tesla earlier this month, I noted the company reported disappointing delivery numbers, sending shares down more than 8%. (Remember, Tesla’s deliveries are the best way for analysts to determine actual sales.)

As you may recall, Tesla had reported 343,000 total deliveries, which missed analysts’ expectations of 364,660.

That said, as reported by the Wall Street Journal, deliveries were up roughly 42% from last year’s third quarter, when Tesla delivered 241,000 vehicles.

I said, while they fell short of expectations, the company’s deliveries are expected to help Tesla post its highest quarterly sales and record profits of $3.34 billion.

So no, the company didn’t deliver as many cars as analysts wanted. But the fact is, Tesla has survived the chip shortage better than most automakers because the company learned how to reprogram its cars. If the company could report an earnings beat, I expected shares to climb.

Well, Tesla did report an earnings beat for its third quarter last night. Earnings of $1.05 per share beat expectations for earnings of $1.01. However, that wasn’t enough to get the shares to rally.

While the company also reported its highest ever quarterly revenue of $21.5 billion, that still fell short of expectations for $22.09 billion.

Vehicle pricing helped Tesla grab almost $3.3 billion in profit during the third quarter, just shy of the company’s record in the first quarter.

Back on the vehicle delivery front, Tesla would have to deliver 500,000 cars in the next three months to hit its 2022 target of boosting vehicle deliveries by 50% year-over-year. To that end, the company expects to come up just shy.

During the call, CEO Elon Musk cited ongoing supply chain issues for the company’s miss.

He said:

There weren’t enough boats, there weren’t enough trains, there weren’t enough car carriers. Tesla got too big. I can’t emphasize enough we have excellent demand for [the fourth quarter] and we expect to sell every car we can make as far in the future as we can see. To be frank, we’re very pedal to the metal come rain or shine. We are not reducing our production in any meaningful way, recession or not recession.

Tesla shares fell about 5% in after-hours trading and, as of this writing, they are down more than 6% today.

Unfortunately for Tesla, we’re in a market environment where a company can’t just report good earnings, it must also guide higher. And while Elon Musk did provide strong fourth-quarter guidance, it didn’t work to help the stock price. Clearly, he’s losing some of his credibility, which I find interesting.

While Tesla currently holds a B-rating in Portfolio Grader, I wouldn’t be surprised if the stock is downgraded to a C-rating next week; so I wouldn’t view the pullback in TSLA as an opportunity to buy the dip.

Earnings Lifts Stocks

While not as good as other quarters, earnings so far have been good enough. As a result, the market has been breaking higher over the last week.

As I’ve been saying folks, fundamentally superior companies will be lifted by earnings – while the weaker companies will continue to struggle.

This is why I am so confident my Growth Investor Buy List stocks will do well this earnings season. The fact is that my Growth Investor Buy List stocks are characterized by 64.2% annual sales growth and 473.9% annual earnings growth. Plus, the analyst community has revised my Buy List stocks’ earnings estimates 22.3% higher on average over the past three months.

By being proactive, we filled out my Growth Investor Buy Lists with companies that can thrive in an environment with a strong U.S. dollar and rising inflation. Namely, companies in oil and energy, fertilizer and food.

In fact, I expect our energy companies to continue to outperform as we head into 2023. As I mentioned last week, FactSet recently reiterated that the energy sector is the sole sector to benefit from positive analyst revisions over the past three months. Third-quarter earnings are now forecast to soar 119.4% year-over-year, up from previous estimates for 103.4% average growth.

Plus, I expect crude oil to rise to $120 per barrel in the spring as seasonal demand perks up. Any economic recovery will shoot up demand even further.

There are a number of energy companies on my Growth Investor Buy List. For the names and full details, click here.

Sincerely,

Louis Navellier

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below:

The Walt Disney Company (NYSE:DIS)