It’s official: Bed Bath & Beyond Inc. (BBBY) is filing for bankruptcy.

The company filed for Chapter 11 bankruptcy protection on Sunday at the U.S. District Court in New Jersey, listing its estimated assets and liabilities between $1 billion and $10 billion.

A statement at the top of the company’s website on Sunday said, “Thank you to all of our loyal customers. We have made the difficult decision to begin winding down our operations.” Customers also received an email about the filing around 8 a.m. that morning.

The company’s 360 Bed Bath & Beyond and 120 buybuy Baby stores will remain open for the time being – with the help of a $240 million loan from Sixth Street Specialty Lending. However, Bed Bath & Beyond stated in its filing that “it is appropriate to close and wind down all 475 remaining brick-and-mortar stores,” which is expected to be done by the end of June.

The company also stated in its filing, “The past 12 months have undoubtedly been the most difficult and turbulent in Bed Bath & Beyond’s storied history.”

Now, just because Bed Bath & Beyond filed for bankruptcy doesn’t necessarily mean that it will be closing down. Chapter 11 bankruptcy is typically used to reorganize a business, allowing operations to continue while the company makes a plan to either repay or discharge its debts. And Bed Bath and Beyond’s plan is to find a buyer.

The retailer filed motions in New Jersey bankruptcy court asking permission to auction its two brands. If the company can find a buyer, then it will stop store closings. If it doesn’t, though, the company will most likely be liquidated.

While Bed Bath & Beyond’s announcement is sad, it’s not surprising. In today’s Market 360, let’s take a look at the retailer’s financial struggles. Then we’ll consider what Reddit investors did to try to “save” BBBY stock.

Bed Bath & Beyond’s Financial Troubles

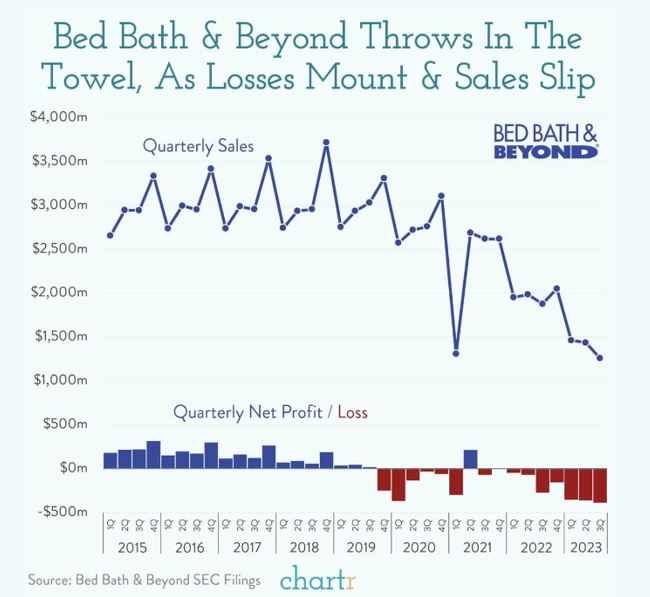

In January 2023, Bed Bath & Beyond posted a loss of $393 million for the third quarter of fiscal year 2022. The company also admitted it wasn’t able to repay loans after the dismal holiday season and started to warn about potential bankruptcy. Then, in February and March, the retailer attempted two different stock offerings that both, ultimately, flamed out.

Also in March, Bed Bath & Beyond reported preliminary results for its fourth quarter of fiscal year 2022. The company anticipated net sales of approximately $1.2 billion and comparable store sales to fall between 40% and 50%.

As you can see from the chart above, the fourth quarter’s expected losses follow a steady trend of decline. Bed Bath & Beyond has posted quarterly losses since the fourth quarter of 2019, except for an outlier in the second quarter of 2021.

Those losses are expected to continue into the first quarter of 2023, as analysts are calling for earnings per share loss of $1.75 and revenue of $1.37 billion, down from an earnings per share loss of $0.92 and revenue of $2.05 billion in the same quarter a year ago.

The fact of the matter is Bed Bath & Beyond has been struggling due in part to years of debt, competition from other retailers (namely, Amazon.com, Inc. (AMZN), and the Covid-19 pandemic.

The Meme Stock Mess

Despite the dismal fundamentals, investors flocked to BBBY stock last year – all thanks to the Reddit “meme stock” Revolution.

The Reddit Revolution first started with GameStop Corp. (GME). A group of Reddit users piled on to buy low-quality GameStop stock during the last trading week of January 2020. Their efforts ultimately created dramatic short-covering rallies that shot GameStop shares sky high. The stock’s fundamentals, however, didn’t match its popularity. The company eventually released poor earnings reports over the coming quarters, and the stock came crashing back down, leaving overzealous investors out of luck.

Bed Bath & Beyond fell victim to this same phenomenon last July.

At the end of July, shares of BBBY were trading at around $5. Then, traders on Reddit began messaging each other on the WallStreetBets thread in early August about why it made sense to buy the stock. (Note: There had been no recent positive news on the company.) Investors jumped into BBBY, and by mid-August, shares were nearly 6X higher and approaching $30.

Well, eventually the mania-fever broke, and a huge selloff followed. By Friday, August 19, the stock had its biggest intraday percentage decline ever, falling roughly 41%. Unfortunately, many investors who bought the stock during the Reddit resurgence were left holding the bag.

Unfortunately, the stock’s performance has only worsened this year…

Since its bankruptcy announcement, BBBY stock fell around 60%. Year-to-date, BBBY is down about 95%.

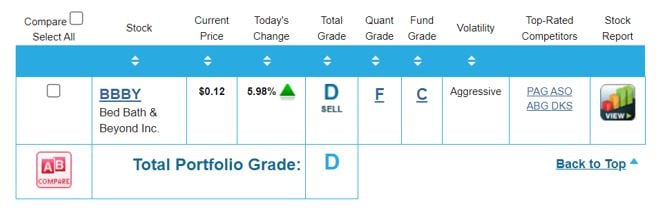

Those who follow my Portfolio Grader

would have known to stay away from the company and been spared the losses. Currently, Bed Bath & Beyond has a D-Rating, making it a “Sell,” but it’s held a D-Rating since November 2022. This is after being revised from a C-Rating, or “Hold,” following its meme stock surge.

Most importantly, though, the stock’s Quantitative Grade is an “F.” The Quantitative Grade, which accounts for about 70% of a stock’s Total Grade, measures a company’s institutional buying pressure. You can think of this as “following the money.” The more money that floods into a stock, the more momentum a stock has to rise. The opposite is also true; the more money that flees a stock, the more momentum a stock has to fall.

So, it seems that the “beyond” in Bed Bath & Beyond has actually hit its limit, as investors flee the stock and the company begins to close down operations.

This is why you want to invest in fundamentally superior companies, i.e., those that provide positive earnings and are backed by persistent institutional buying pressure.

This holds especially true during the first-quarter earnings season.

The first-quarter earnings announcement season is off to a stunning start, with more than 76% of S&P 500 companies topping analysts’ expectations so far. And companies that post strong numbers are being rewarded.

As I mentioned in yesterday’s Market 360, S&P 500 companies that have posted a positive earnings surprise have experienced an average rise of 2.2% in the two days prior to the release through the two days following the earnings report, according to FactSet.

This means that earnings are working!

So, if you want to position your portfolio for success, your best bet is with fundamentally superior stocks.

If you’re not sure where to look, then consider my Growth Investor service. We’ve taken steps to align our Buy Lists to prosper in the current environment, as we’ve “locked and loaded” our Buy Lists with stocks with accelerating earnings and sales momentum.

This includes three new recommendations I just released in today’s Growth Investor Monthly Issue for May.

If you become a Growth Investor member, you’ll have access to my newest recommendations, as well as my two Buy Lists: High-Growth Investments and Elite Dividend Payers. I also include a Top Stocks list, which is a select list of stocks from my Buy Lists that are backed by persistent institutional buying pressure and stunning fundamentals.

To join me at Growth Investor today – and gain full access to my Buy Lists – click here.

Sincerely,

Louis Navellier

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below:

Amazon.com, Inc. (AMZN)