The healthcare sector, as measured by the Health Care Select Sector SPDR ETF (NYSEARCA:XLV), is down 1.5% so far in 2018, but even as the group as a whole struggles one of my favorite NexGen healthcare names is up more than 20%: Teladoc Inc (NYSE:TDOC).

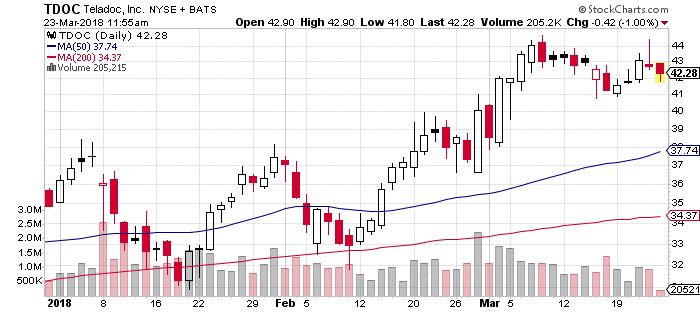

Teladoc is the leader in the emerging telehealth industry. And TDOC is consolidating after hitting a new all-time high on March 8. It successfully tested its breakout level at $40 and support around $38. And now it’s taking a breather ahead of its next leg to the upside.

Lots of Long-Term Benefits for TDOC

In the future, the days of spending hours in a doctor’s office only for them to tell you that you have a sinus infection and need some antibiotics will be non-existent. This type of visit — which accounts for a large percentage of all doctor’s appointments — will instead be done via telehealth platforms like the one TDOC provides.

Your doctor will be at your fingertips — almost literally. You’ll be able to connect with him or her via videoconferencing on your phone or computer rather than having to drag yourself out of bed and likely catch some other bug by sitting in a stuffy room with a bunch of other sick people.

Not only with this save you time and help you rest and recover more quickly, it will also be covered by your insurance the same way a normal doctor visit is. About 75% of health systems currently offer or plan to offer telehealth services. And as more people become comfortable with this new approach the numbers for TDOC will only continue to grow.

Another long-term positive for this company is the expansion of these services into Medicare Advantage. A new law allows plans to include telehealth in their bids to the Centers for Medicare and Medicaid Services in 2020.

The Bottom Line for TDOC

Teladoc is losing money currently, and that’s expected to remain true for the next couple of years. However, revenue and customer and user growth are increasing in big ways. The $2.6 billion company’s 2018 outlook for revenue growth is 52%, adjusted EBITA is 169% and total visits is 33%, with visits for fee-only members expected to grow from zero to 18 million.

This is a clear leader in NexGen technology and healthcare, and considering it’s still only a small-cap stock, I have no doubt an investment will pay off handsomely in the years ahead.

Matthew McCall is the founder and president of Penn Financial Group, an investment advisory firm, as well as the editor of FUTR Stocks and the ETF Bulletin. Matt just launched two new investment advisories focused around the “next” generation investing theme. His trademark three-prong investing approach targets the mega-trends old Wall Street is missing out on. Click here for more information on the “NexGen” Experience.