From a bird’s-eye perspective, DoorDash (NYSE:DASH) seemingly has the right qualities to be one of the top players for the Roaring 2020s. Utilizing connectivity platforms to bolster the age-old consumer delivery industry, DASH stock merits enthusiasm. However, you’ll never win as an investor if you’re willing to fork over any sum for a particular company.

Simply put, DASH stock has jumped too far to warrant a confident bullish position. On a year-to-date basis, DoorDash shares have gained over 51%, which makes the food-delivery service an ideal candidate for selling into strength.

Yes, the business is relevant — there’s no question about that. Prior to the novel coronavirus pandemic, experts had pegged the online food delivery market to generate $200 billion by 2025. That’s a hefty sum on its own. But when you bring the present health crisis into the picture, it’s possible that this forecast is an underestimate.

Still, this shouldn’t give you the greenlight to buy DASH stock. While the online delivery space should expand, attempting to identify individual winners and losers could end up being a fool’s errand. For one thing, delivery services isn’t exactly rocket science. Therefore, the lower barrier to entry invites competition — and they will almost certainly come.

Second, these types of market subsegments are vulnerable to commoditization. Let’s face reality. The consumer doesn’t really care how the product arrives, only that it does and in an acceptable format. Sure, there are some differentiation opportunities in terms of superior customer service. But the benefits are stuffed in the minutia and thus may not matter in the end.

Unfortunately, this means the consumer will choose the cheapest delivery option available. Further, if we encounter economic weakness in the months ahead, this will force DoorDash into a war of price attrition. That’s not necessarily a game you want to play.

Why the Covid Catalyst Is a Distraction for DASH Stock

Recently, I’ve come across many arguments that suggest DASH stock is due to move higher because of the new normal. Consumers want to go out and purchase stuff, but they want to do so safely. I get that. However, you have competing narratives that don’t augur well for DoorDash.

You shouldn’t read into this that I’m picking on DASH stock. Rather, the narrative for the broader industry is suspect. As the New York Times pointed out right before the U.S. and the rest of the world momentarily went belly up, consumers who use online food-delivery services can expect to pay up to 91% more than they would have had they bought directly from the underlying restaurants.

Even in the wildest and most uncontested bull market, you’d be hard-pressed to find households who will frequently pay double-digit premiums for services they can realize themselves. Add in the uncertainty of the coronavirus and you have a tough backdrop for DASH stock.

True, many people will take advantage of online delivery services. However, they’ll also be looking to narrow those premiums, thus risking a widescale price war.

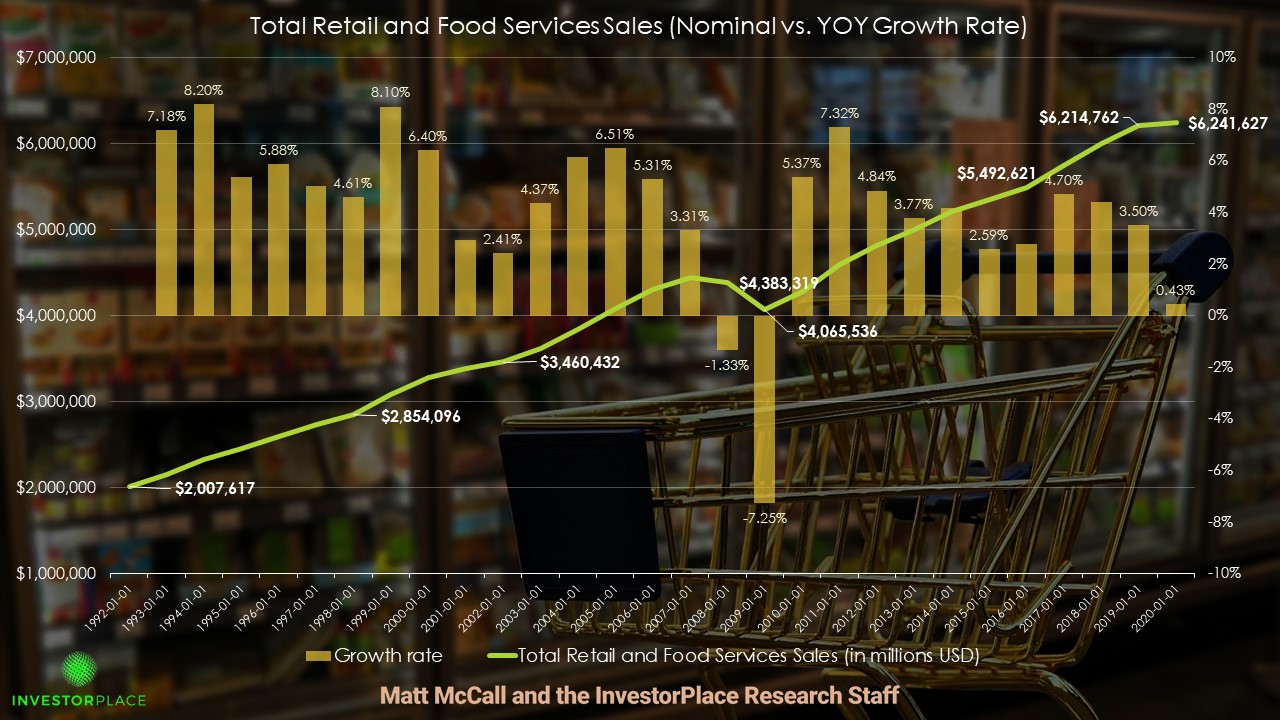

We also have evidence that the Covid-19 catalyst for this industry is a temporary one. Between 2010 and 2019, the annual growth rate of total retail and food services sales averaged 4.3%. However, from 2019 to 2020, the growth rate was a measly 0.43%.

Click to Enlarge

Obviously, the pedestrian growth rate was due to the sudden erosion of retail demand in the early days of the pandemic. Nevertheless, year-over-year growth in the fourth quarter of 2020 was the same as YOY growth in Q4 2019: 4%.

In other words, the demand spike that we see in certain retail subsegments — such as online food deliveries — may not be net accretive. Instead, consumer dollars that would ordinarily have gone to disrupted businesses went to delivery services.

Once society truly returns to normal, the temporary catalyst benefitting DASH stock should fade.

Get In at the Right Price

As I stated earlier, online deliveries are relevant. And it’s possible that DASH stock could come down to a price where it makes sense. However, that time is not now.

In prior write-ups about DoorDash, I mentioned that the market capitalization of the company kept attracting premium after premium. That’s just not going to work in a sector that’s rife with competition and begging for a war of attrition.

Further, when restaurants open back up, the dining out via takeout or delivery experience will lose its luster. That’s why I mentioned that the delivery service model isn’t accretive. It’s a robbing Peter to pay Paul effect. Once everything normalizes, some sanity will return to food deliveries.

Indeed, you might see a swing up for in-restaurant dining due to pent-up demand. That will force a correction in names like DASH stock, which of course wouldn’t be ideal.

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now.