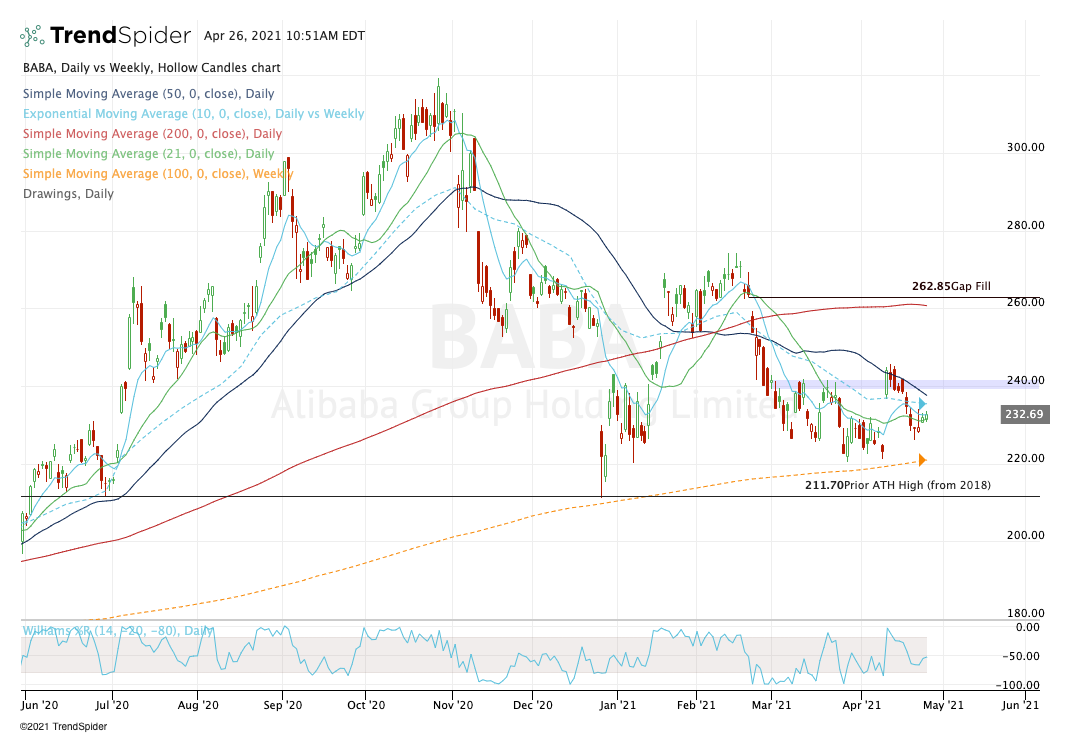

With stocks near all-time highs, it’s worth looking over the stocks that are not notching new highs at the moment. Alibaba (NYSE:BABA) is most certainly one of those names, with BABA stock down 27.3% from its all-time high set in October.

Of course, the counterpoint to that is obvious: Why buy into relative weakness, don’t we want stocks that are performing well?

Our argument is also simple: It depends on your timeframe, while also using some perspective. Traders and short-term investors must use strong price action to their advantage. They need to ride the hot stocks to new highs to secure their gains.

For long-term investors though, weakness is an asset. When we have stocks suffering deep declines while the businesses are completely fine — even thriving — then that’s when we want to pounce. Maybe it takes a quarter or two. Perhaps it takes a year for that value to be realized.

But it will be realized.

Why BABA Stock Represents Value

Shares are technically in a bear market, since BABA stock is down by more than 20%. At its lows, the stock was down almost 34%. That all sounds quite scary, but let’s use some perspective.

Alibaba stock is trading above its pre-coronavirus high from January 2020 (which was also its all-time high prior to the summer rally). It’s also trading back down to where it was in July. So it’s not like we’re at multi-year lows with no end in sight as the company works through a massive turnaround.

In fact, after such a decline, I would argue that Alibaba is a value growth stock, not just a growth stock. That assessment comes from the company’s culmination of assets, growth and valuation.

Current estimates call for 39% revenue growth this year and 31% growth next year. That’s very impressive, particularly given the company’s $628 billion market capitalization.

On the earnings front, analysts expect 24% growth this year and 9.3% growth next year. Personally, I believe next year’s growth estimate is too conservative, but that’s quite far away. For now, let’s focus on the double-digit top- and bottom-line growth for 2021.

Should Alibaba report in-line earnings, it will earn more than $10 per share this year. That leaves the stock trading at just 23 times this year’s earnings. There are a number of consumer packaged goods and consumer staples with stagnant growth that trade around the same valuation.

BABA stock is also trading at a discount to its other mega-cap tech peers, although those companies are based in the U.S.

Finally, its assets are top notch. The company owns the most active e-commerce sites in China, which boasts a population of 1.4 billion people. Those sites — Tmall.com and Taobao.com — are also some of the most popular websites in the world. For some perspective, Tmall is the third most popular website worldwide.

Why Alibaba Is a Buy

Click to Enlarge

If Alibaba has great growth, a cheap valuation and incredible assets, why on earth is the stock almost 30% off the highs?

That’s a great question and there’s a simple answer: China.

While China represents incredible long-term opportunity, the ride can also be volatile. Remember when I mentioned the U.S. based tech stocks and the higher valuation they command?

That’s partly because there’s more certainty surrounding those names. Investors don’t like uncertainty and with BABA stock, there’s been plenty of it. Most of that is based around regulators, as they look to crack down on Alibaba for its anti-competitive practices.

That all came to a head in the fourth quarter, when the Ant IPO — an entity Alibaba owns a one-third stake in — was nixed just days before its debut.

However, Alibaba was hit with a smaller-than-expected fine from Chinese regulators earlier this month. That should remove a large headwind of uncertainty, although the stock price wouldn’t have you thinking that.

Perhaps we’ll need to hear from the company at its upcoming earnings report for more transparency. However, by the way things are setting up now, BABA stock could be looking at a powerful second-half rally should it put these issues behind it.

With or without more short-term pain, we’re buyers of Alibaba.

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now.