These are the six most undervalued mid-cap stocks to buy now. These stocks have market capitalizations between $500 million and $10 billion and have low valuation multiples. They also have good earnings prospects going forward, recession or not. If they don’t, they are generating large amounts of free cash flow.

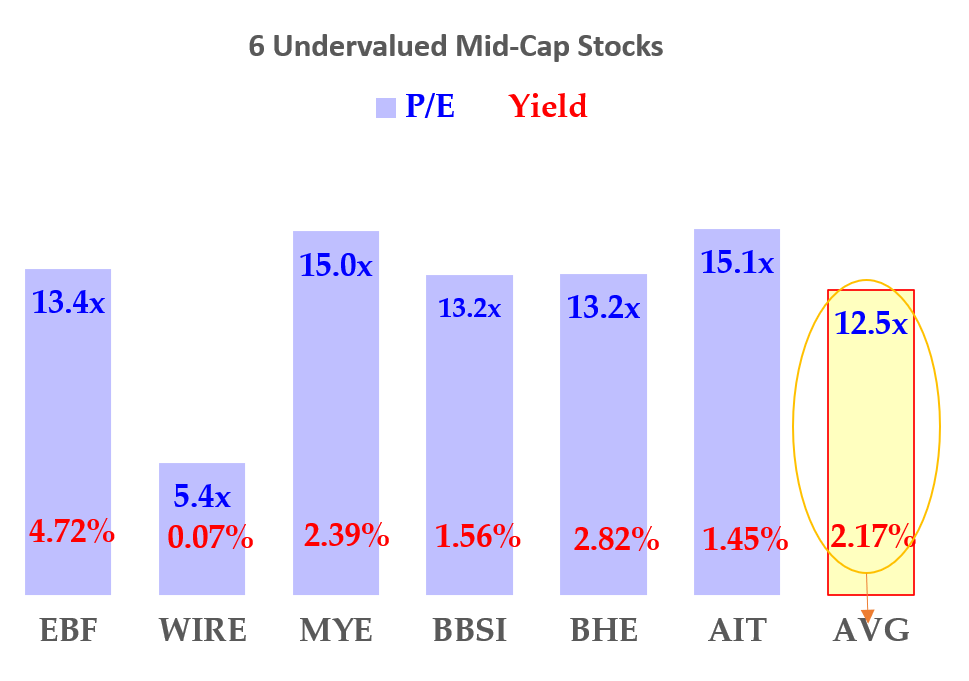

These stocks are also very inexpensive right now. As a result, the average P/E multiple of this group is 12.5x and they have an average dividend yield of over 2%. This can be seen in the chart on the right.

Click to Enlarge

It’s not uncommon as well for these kinds of mid-cap stocks to have significant upside potential as well. In most cases, I will point out the average upside target prices that analysts have for the stock.

This article will focus on those stocks with the best of both worlds – cheap valuations and above-average growth rates.

Let’s dive in and look at these undervalued mid-cap stocks.

| EBF | Ennis | $21.18 |

| WIRE | Encore Wire Corporation | $113.72 |

| MYE | Myers Industries | $22.59 |

| BBSI | Barrett Business Services | $76.75 |

| BHE | Benchmark Electronics | $23.39 |

| AIT | Applied Industrial Technologies | $93.71 |

Undervalued Mid-Cap Stocks: Ennis, Inc (EBF)

Market Cap: $523 million

Ennis (NYSE:EBF) is a mid-cap stock that is known for its production and marketing of printed business products. Believe it or not, this is still a big business. Ennis makes items like checks, promotional products, envelopes, pressure seals, presentation products, plastic cards and multimedia packaging.

For example, for the quarter ending May 2022, it produced revenue of $107.7 million, which was $8.82 million higher than expected, according to Seeking Alpha. Analysts project revenue of $419.97 million for the year ending February 2023. That will be 5% higher than the revenue of $400 million last year.

In addition, analysts expect the company will make $1.58 per share, up 38.6% over the $1.11 per share it made last year. At $21.18 on July 19, this puts the stock on a forward P/E of just 13.4x for the year ending Feb. 28, 2023.

So far Ennis has not raised its quarterly dividend of 25 cents, which it has paid for the past 5 quarters, or $1 per share annually. That gives it an annual dividend yield of 4.7%. This is a very attractive dividend for most investors, especially since it is well-covered by earnings per share.

Moreover, Ennis is cash-flow positive, even after capex spending. For example, last quarter it produced $14.2 million in operating cash flow and spent $1 million on capex. The resulting $13.2 million in free cash flow represents a margin of 12.2% from its quarterly sales of $107.7 million.

That $13.2 million in quarterly FCF more than covers the $6.5 million cost of its dividends and even $1.1 million in share repurchases. Moreover, the stock has an average target price of $26 per share or 22.7% over today’s price.

Encore Wire Corporation (WIRE)

Market Cap: $2.13 billion

Encore Wire Corporation (NASDAQ:WIRE) is an extremely profitable manufacturer of electrical building wires and cables for interior electrical wiring. Analysts project that its revenue will rise by 9.4% this year to $2.84 billion. And for 2023, analysts project revenue of $2.85 billion, just slightly higher. It trades for 5.4x earnings this year and 8.3x for 2023 because of projections of lower earnings.

However, Encore Wire produces large amounts of free cash flow. Last quarter it generated $117.7 million in operating cash flow and had $32 million in capex spending. That $85.7 million in free cash flow (FCF) represents 11.85% of its $723 million of revenue last quarter. That implies that its annual FCF will be higher than $336.5 million this year.

But instead of paying a large dividend (although it does pay a small dividend), it uses most of that cash to buy back large amounts of its shares. Last quarter it repurchased $58.4 million of its shares and used over 68% of its $85.7 million in FCF. This means it could spend 68% of its $336.5 million in FCF, or $229 million.

So that represents 10.75% of its $2.13 billion market cap. This is the real appeal of WIRE stock — it’s buying back large amounts (over 10% annually) of its market value. That will push the stock higher over time.

Moreover, analysts now project that its price target is $175.00, or 53.9% higher, based on a survey by TipRanks.com.

Myers Industries (MYE)

Market Cap: $800.3 million

Myers Industries (NYSE:MYE) operates in two areas: pallets and materials handling equipment in one division, and tire and wheel repair equipment in the other division. Sales are forecast to

rise 14.7% this year to $873 million and up 5.9% next year to $924 million.

Moreover, the company is very profitable. Analysts project EPS of $1.51 this year, up 55.7% from 97 cents last year. And for 2023, they forecast EPS of $1.85 per share, up another 22.5%. At $22.59 on July 19, this puts the stock on a forward 2023 multiple of just 12.2 times. That is very inexpensive, especially for the level of growth it is experiencing.

On top of this, Myers pays out a dividend of 54 cents annually. This gives the stock an annual dividend yield of 2.4%. This dividend payment represents just under 36% of its earnings forecast for this year, making it very sustainable.

Barrett Business Services (BBSI)

Market Cap: $544 million

Barrett Business Services (NASDAQ:BBSI) provides business and management consulting services to small- and mid-cap companies. It signs contracts where it’s “assuming responsibility for payroll, payroll taxes, workers’ compensation coverage, and other administration functions for the client’s existing workforce.”

The company is very profitable and growing nicely. For example, sales are forecast to rise almost 10% to $1.05 billion from $955 million in 2022. And for 2023, analysts forecast sales will move 6.1% higher to $1.11 billion.

Moreover, those analysts project earnings per share of $5.83 this year and 10% higher next year at $6.43 per share. So, at $76.75 per share on July 19, the stock is on a forward P/E of just under 12x for 2023 (11.9x).

For the past three years, Barrett Business Services has paid the same dividend of $1.20 annually and it might be close to raising it soon. Right now this gives BBSI stock a dividend yield of 1.6%.

However, the company has been increasing its share repurchases which are four times higher than its dividend payments. Right now it is on a run rate of $35.2 million in buybacks annually. That represents a buyback yield of 6.47% of its $544 million market value.

So investors in the stock receive a total yield of 8% annually. In fact, analysts surveyed by TipRanks puts its target value at $99.50, or 30% over today’s price. That makes it one of the best undervalued mid-cap stocks on this list.

Benchmark Electronics (BHE)

Market Cap: $798.2 million

Benchmark Electronics (NYSE:BHE) is an electronics engineering services company that is growing quickly and is very profitable but whose stock is inexpensive. That is the opportunity here.

For example, its forward P/E for 2023 is just 12.1x, down from 13.2x for 2022, and it has a dividend yield of 2.8% at July 19’s closing price of $23.39.

Moreover, it is buying back a good amount of its shares — about $8 million quarterly, or $32 million annually. That works out to 40% of its market value. So shareholders receive a total yield of 6.82% with this stock, which makes it worth buying for the long term.

Analysts project that its average price target is $32 per share, or 36.8% higher.

Applied Industrial Technologies (AIT)

Market Cap: $3.48 billion

Applied Industrial Technologies (NYSE:AIT) is a sophisticated and very profitable distributor of engineering products and things like fluid power components and systems. This fiscal year ending June 30, analysts project revenue will be 15.2% higher at $3.73 billion. Next year, it will be at least 3.5% higher at $3.86 billion.

AIT stock is also on a forward P/E (for June 2023) multiple of just 14.5x.

Moreover, Applied Industrial Technologies produces large amounts of free cash flow. In Q1 alone, it generated $52.6 million in operating cash flow and had just $4.2 million in capex spending. The resulting $48.4 million in FCF represents a 4.93% margin on sales of $981 million for the quarter.

This allows the company to both pay a dividend (with a 1.45% dividend yield as of July 19) and buy back its common stock shares.

Moreover, analysts surveyed by TipRanks give AIT stock an average price target price of $124.67, or 33% higher than today. This makes it one of the most undervalued mid-cap stocks on this list.

On the date of publication, Mark Hake did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.