Micron Technology Inc. (MU) is having a year to forget.

After blowing up the markets with a 428% slingshot between January 2013 and the end of 2014, the finance gods struck MU stock hard over the next eight months, essentially halving its remarkable rally.

After blowing up the markets with a 428% slingshot between January 2013 and the end of 2014, the finance gods struck MU stock hard over the next eight months, essentially halving its remarkable rally.

Those who got in early are still reaping the benefits, but the Micron latecomers are singing a decidedly different tune. Year-to-date, MU shares are down nearly 56%, and on the surface level, there’s not much evidence for optimism.

MU Stock By the Numbers

The primary concern for MU stockholders is in the health of the balance sheet, which reveals some worrying trends. Micron’s long-term debt jumped 236% since the end of fiscal year 2011, an ascent that shows little sign of abating. Over the last four quarters, the memory chip maker added 35% to its debt obligations, a fact that doesn’t sit well with MU investors.

Worse yet, its on-hand cash continues to subside, losing more than 39% over the same time period.

Micron found an especially bad time to be carrying so much weight on its books. With a forecast-busting 271,000 jobs added to the economy for the month of October, the U.S. Federal Reserve is even more incentivized to green light a much-discussed interest rate hike in December. That likely implies further strength in the dollar and more onerous financing charges on future debt.

It may also mean hindrances in longer-term business strategies at a time when competition is increasingly consolidated.

The issue that plagues MU stock and the memory chip industry as a whole is eroding market share. Micron and its Korean rivals Samsung Electronics Ltd. (SSNLF) and SK Hynix Inc. already produce enough memory chip products to comfortably swallow what little demand is out there. Bringing another unpleasant surprise is Intel Corp

. (INTC), which recently announced that it will be spending as much as $5.5 billion to convert its China-based semiconductor fabrication factory to a memory chip producer — putting Intel into direct competition with Micron.

The Good News

Fortunately, the news is not all bad.

After missing the earnings-per-share estimate for the third quarter of fiscal year 2015, MU stock came back hard for Q4, hitting an EPS of 37 cents and exceeding Wall Street consensus by over 15%. In fact, it was the strongest earnings showpiece by Micron since Q1 of fiscal year 2014, when MU stock almost doubled its EPS estimate.

Furthermore, MU stock has significant advantages in its favor, specifically in the realm of profitability.

Both Micron’s operating and net margins are well above average for memory chip makers, with the company making efforts in keeping its inventory and business expenses in check with reality.

Combined with its severely depressed share price, MU stock is — at least from a trailing price-to-earnings perspective — one of the most undervalued technology companies available.

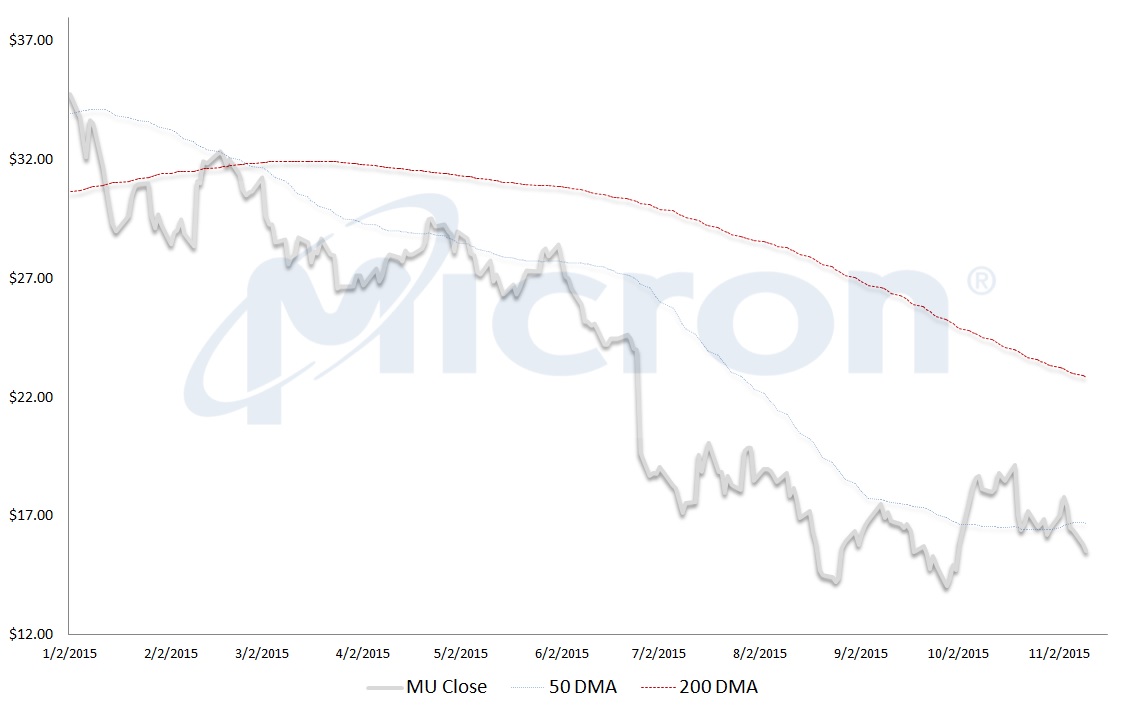

Click to Enlarge

Technically, one could make the case that bearish momentum has subsided, potentially setting up an imminent reversal. We can determine this by the length of days that MU stock has spent when its 50-day moving average is beneath its 200 DMA — the so-called “death cross” signal.

Since its initial public offering, MU stock has flashed the death cross 18 times, with the most recent occurrence on Feb. 25. On average, MU spends 163 days submerged in the death cross zone following the initial signal. Barring anything unusual, Micron shares are on pace this year to hit upwards of 200 days. Based on historical statistics, the bearishness in MU stock is a bit long in the tooth, which may mean a potential return to upward mobility.

Bottom Line

Ultimately, MU stock is a higher risk, higher return opportunity.

Micron has fundamental strengths that make it more than just a speculative bet on the “cheapness” of its share price. In addition, shares appear to be stabilizing over the past few months, which is in line with statistical expectations.

However, the markets historically have been very volatile towards MU, and the memory chip industry overall faces an uphill battle.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.