After posting dreadfully poor employment numbers in the closing months of summer, the U.S. Department of Labor pleasantly surprised Wall Street with a string of positive jobs reports for October and November.

In those two months, the economy added 509,000 non-farm jobs, with October’s tally of 298,000 being the biggest monthly haul so far this year. With the current unemployment rate unchanged at 5%, this in theory sets the stage for a hearty recovery.

As good as a hypothesis that may be, reality has proven exceptionally unkind to the mining and energy sectors — namely, oil and gas exploration — which continue to cut workers en masse. Naturally, this has taken a huge bite out of construction stocks.

The problem is two-tiered. First, the jobs recovery is significantly allocated toward low-paying retail positions — good for padding government statistics, but not really substantive enough to spark broad strength. Second, even though hiring within the construction sector has risen roughly 18% since 2011, the present growth rate has rapidly subsided against previous years.

The bottom line, however, comes down to commodities. If there’s less need for high-level projects and the transportation of raw goods and materials, companies that offer such services and equipment won’t find much business. Few insiders are predicting a rally in commodity prices any time soon, which means volatility among construction stocks may continue to be the norm.

With that in mind, here are three firms that are particularly at risk.

Construction Stocks at Risk: Caterpillar (CAT)

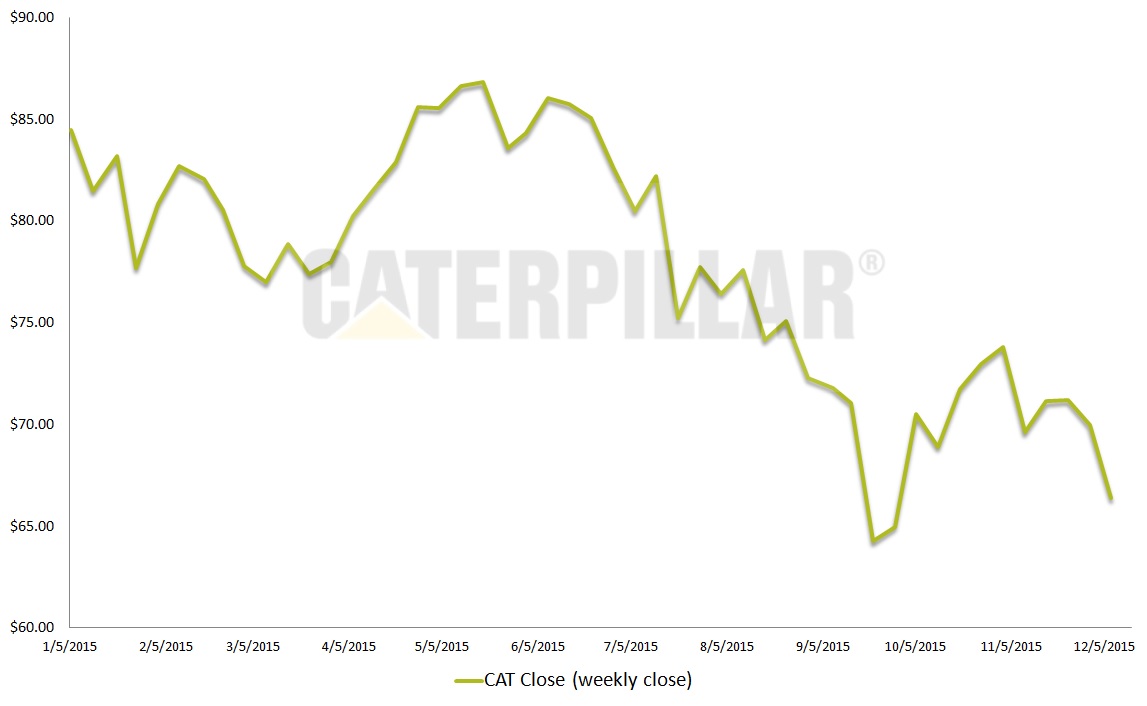

Click to Enlarge

While undeniably a leading stalwart among construction stocks, CAT simply can’t catch a break from falling commodity prices. The mining and energy exploration industry is its core business. Improvement in construction subsectors — most notably real estate starts — are helpful, but are less dependent on heavy-duty equipment.

The paradigm shift in commodity prices is quickly altering CAT’s corporate culture. Rather than committing full bore into equipment sales, management is instead focusing on maintenance and parts services for already sold machinery.

Initially appearing as a rather peculiar idea, the concept makes sense: Trailing revenue is well off the pace set over the past four years and that will not change in 2016, a point conceded by the company in its last earnings report.

Technically, CAT stock finds itself on shaky ground. After CAT charged higher earlier in the year — strong earnings in the first quarter of fiscal year 2015 helped significantly — CAT stock failed to breach upside resistance. As subsequent earnings performances failed to inspire confidence, more people chose to head for the exits. Currently, CAT stock is down nearly 30% this year.

Management’s decision to adapt to the new reality of commodity prices is a creative approach to a perniciously difficult problem. There’s hope yet for CAT, but don’t expect too many fireworks in the near term.

Construction Stocks at Risk: Deere & Co. (DE)

Click to Enlarge

from a major financial institution like Barclays would be a reason to celebrate, but for Deere & Co. (DE), the response in the markets has been disappointingly muted.

For the current month, DE stock is down 1%, failing to build off a price spike stemming from a very strong Q4 FY2015 earnings beat. The likely culprit? Top-line sales, which preliminary results reveal are 20% below that of the prior fiscal year.

The quandary again is centered on the underlying industry. Deere & Co. — the international leader in farm equipment production — faces severe pressure from lower agricultural commodity prices, which then cap farmers’ profitability margins.

This in turn stymies cash flow that would normally cycle back into equipment purchases. Instead, farmers are holding onto their money, causing industry experts to predict a sizable decline in sales of agricultural machinery.

Contrarians looking to take advantage may cite a trailing price-earnings ratio of 13 as an indicator of an undervalued opportunity. Using fundamental gauges can be deceptive here, however, especially when DE stock’s net income for the current year is 38% below the combined average of the previous four years.

Not only does this signal future cost cutting, it also brings into question DE’s growth potential in light of the company’s negative guidance for 2016.

As with Caterpillar, there’s lingering concerns among DE stock holders about the trajectory of commodity prices. Although it’s not a company facing an imminent threat, industry headwinds will make it difficult going for Deere.

Construction Stocks at Risk: Komatsu Ltd. (ADR) (KMTUY)

Click to Enlarge

KMTUY’s chief executive officer, Tetsuji Ohashi, was even more pessimistic than his competitive rivals, stating that the forecast for commodity prices would be questionable even in 2017.

Ohashi’s apprehensions are certainly understandable, given very poor Q2 earnings released in late October: Net income fell by a steep 19% against its year-ago level, while KMTUY’s full-year earnings is estimated to drop 10%.

Adding to these bearish developments is operating margins, anticipated to give up almost 9%. Deflated commodity prices have taken the wind out of purchasing demand from miners, and revenue from KMTUY’s repair services of longer-held machinery is relatively marginal.

Little change can be expected in the near term, unless the Chinese markets stage a miracle rally. In the six months between April and September, Chinese sales of mining and manufacturing equipment fell by a sickening 44%.

Other major markets, not including the Middle East, also failed to meet forecasts, contributing to KMTUY stock’s YTD loss of 28%; almost identical to rival CAT stock’s return thus far.

Construction stocks are in a tough situation, and lack of global demand has left little room to hide. As a result, KMTUY stock has been left gasping for air. Unfortunately, even Komatsu’s management team believes it will get worse before it gets better.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.