Most retail stocks have been leveled under the e-commerce regime, but a few are not only weathering the storm, they’re thriving. Costco Wholesale Corporation (NASDAQ:COST) is one of those companies.

Costco stock, which was on our list of 8 Stocks That Can Win Despite Amazon, is up 20% over the past year. But can Costco continuing winning against Amazon.com, Inc. (NASDAQ:AMZN)?

That’s always been the concern. The rhetoric over the past few years is that Costco’s unique shopping experience isolates it from the likes of Amazon. Shoppers not only have a unique product offering (bulk), but also a unique and satisfying shopping trip.

Because of its membership fees, Costco is able to generate a ton of revenue right up front, before even worrying about its actual sales. Sort of like Amazon Prime.

Amazon may eventually catch up and wear Costco down. But if that’s the case, it’s true impact will take some time to shine through.

What to Expect From Costco Stock

COST reports earnings on Thursday after the close. Analysts expect Costco stock to earn $1.31 per share on $28.52 billion in revenue for the quarter. That’s good for 5.5% earnings growth and 6.5% sales growth — both solid figures. For the year, analysts expect earnings growth of 5.8% and revenue growth of 7.3%. Obviously Costco is doing good — but not great — in the face of Amazon.

The problem with Costco stock isn’t earnings growth — it’s valuation. Shares trade at a surprising 27 times forward earnings and 32x trailing earnings. That’s a big valuation given mid-single digit earnings growth for 2017.

In finance, predicting the future is hard. Predicting it for retail is even harder. For COST, analysts expect 13.3% earnings growth next year and ~10% annual growth for the next five years. Even if that comes to fruition, 27x forward earnings is still lofty in my view. It doesn’t help that Costco stock only yields about 1.15%. In other words, there could be upside, but it may be limited.

With that said, COST stock has almost always traded at a premium multiple. Given its ability to grow sales and earnings in this environment, one could argue that Costco stock is more valuable than ever.

The fact that Costco can and is raising membership prices next month tells a good story as well. First, higher membership prices equals higher revenue. Secondly, that Costco can even do such a thing in retail’s current state just goes to show how much its customers truly love the experience.

Trading Costco Stock

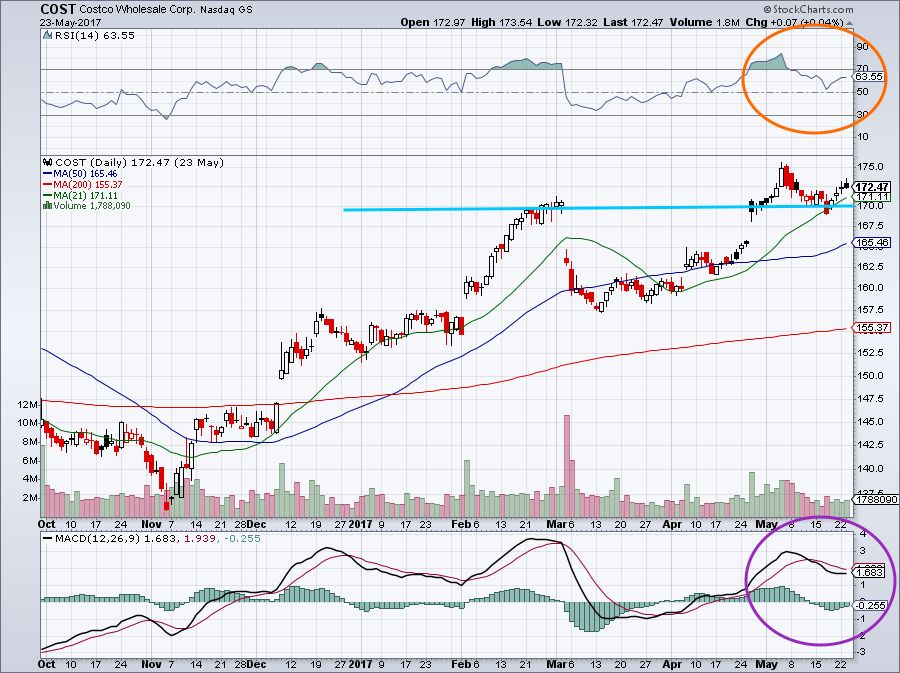

Click to Enlarge

So we’ve established that Costco stock is a modest grower, with a not-so-modest valuation. But what does its stock price say?

Recent resistance near $170 has become support (teal line). COST stock has also worked off its previous overbought condition (orange circle). It’s now working on turning its momentum bullish (purple circle).

Despite the somewhat iffy fundamental debate, the charts actually look pretty good. A break below $170 would be a negative development. Although if it finds support at the 50-day moving average near $165, bullish traders could take a stab at COST.

The fundamental outlook does brighten for Costco in the second half of 2017; and if its technicals align, shares that are currently up 8% in 2017 could add to the gains.

So is Costco Amazon-proof? Right now its stock and business have been doing good — but again, not great. At least through year-end, that looks set to continue.

On that basis alone, it’s hard to bet against COST, despite a high valuation and low yield. The trend is your friend — don’t bet against it until it breaks. Maybe that will happen with Costco’s earnings report on Thursday. But betting that it will is only guessing at this point.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held no positions in any security mentioned.