Despite its relevant technologies and popular-culture status, Fitbit Inc (NYSE:FIT) can’t get any love from the markets. Year-to-date, Fitbit stock has cratered nearly 30%. The only real good news from a technical perspective is that shares seemingly hit bottom. Of course, I and other bulls reiterated that story line, sadly to no avail. Do FIT investors have any reason to hope?

Encouraging, the analyst landscape is not. Recommendations currently register straight down the middle. Experts aren’t cold on the Fitbit stock idea, but nor are they hot on it.

Toward the end of last year, and in January of this year, we witnessed several analyst downgrades. Furthermore, the average price target for FIT is $7.04. Fitbit shares opened Tuesday at $5.16. Don’t be surprised to see more downgrades.

InvestorPlace has a lot of depressing articles about Fitbit’s depressing future. Even “bullish” articles about FIT stock have major caveats and largely focus on short-term technical momentum.

But the key reason that my colleagues tell you to run from FIT stock is the competition. As InvestorPlace writer Tom Taulli reports,

“Fibit has suffered a major drop in market share. According to a report from IDC, the company is now the No. 3 player (in terms of global shipments), behind Apple Inc. (NASDAQ:AAPL) and Xiaomi.”

Richard Saintvilus notes that, “Fitbit’s competitive position seems to worsen just as the overall wearable device market is expanding.” While Laura Hoy warns us of the dangers ignoring red flags, comparing FIT stock to BlackBerry Ltd (NASDAQ:BBRY).

Can the upcoming second-quarter earnings report help turn the frown upside-down?

Can Q2 Earnings Provide a Reprieve for Fitbit Stock?

Initially, neither the numbers nor analyst sentiment speak volumes for Fitbit stock. Wall Street consensus pegs earnings per share to come in at a dismal 15-cent loss. Not only that, the estimate is only one penny above the forecast spectrum low, which ranges from $-0.16 to $-0.08.

To provide some context, analysts expected 11 cents in per-share earnings for Q2 fiscal 2016. The actual results produced one penny better, leading to a 10% positive surprise. In Q2 of 2015, consensus called for an 8-cent EPS. Instead, FIT unleashed a massive 162.5% earnings beat.

On the revenue front, the Street expects the wearable-device maker to haul in $341.1 million. Like the earnings estimate, this is near the low end of the spectrum — it ranges from $331.7 million to $364.9 million.

As previously mentioned, sales is where Fitbit stock is most vulnerable. Investors don’t appreciate recent mediocre results against expectations. Additionally, the annual top-line trend has worryingly sputtered.

The one positive, as fellow contributor Joseph Hargett mentioned, is lowered expectations. Although I’m not personally a fan of this kind of thinking, it actually does work. During the presidential debates in 2000, George W. Bush leaped over a ridiculously low standard. In contrast, his rival Al Gore disappointed against extremely high standards.

FIT stock, like any other investment, ultimately runs on human emotions. You can throw all the legitimate reasons why you should avoid the company. Still, if people perceive underappreciated value in Fitbit, guess what? Shares have a solid chance of moving higher.

It’s certainly not fair, and it’s not logical. However, I think the relative sideways action — as opposed to an outright collapse — in Fitbit stock is meaningful.

Give FIT a Chance

While critics will argue that FIT has no place in the retail markets, I disagree. According to Statista.com, the biggest competition doesn’t originate from brand-name players like Apple or Samsung Electronic (OTCMKTS:SSNLF). Instead, no-name brands dominate the wearable device market.

Granted, that’s not necessarily a good thing. However, the argument that Apple is stealing market share doesn’t hold as much water based on one quarterly report. Thus, the biggest challenge for Fitbit stock is for management to convince potential buyers that they have a better and more compelling story than some cheap, Chinese knock-off. I propose that is an easier obstacle to conquer than cage-fighting Apple or Samsung.

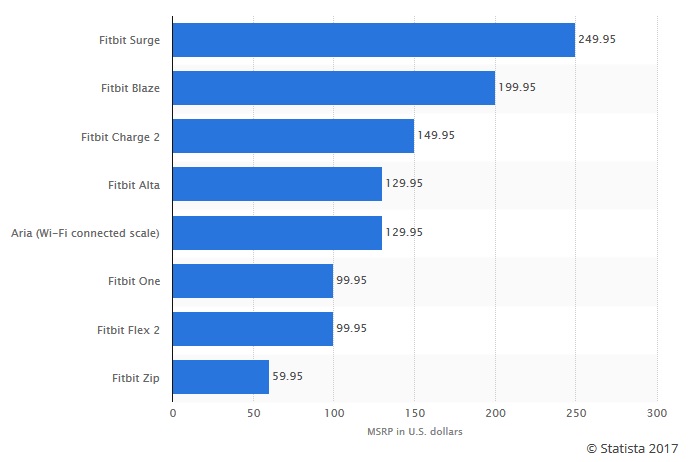

Another argument that doesn’t really come up in analyst circles is Fitbit’s broader product-price range.

Click to Enlarge

The most expensive FIT device is cheaper than Apple’s cheapest digital watch. Granted, the Apple Watch Series 1 has more functions than the Fitbit Surge. But the question is, who will risk an expensive device for activities that could result in breakage?

Undoubtedly, trendsetting active individuals will show off their latest acquisitions. But for the general public who may want a superb fitness device without onerous costs, Fitbit offers great options that won’t break the bank.

Now, to be clear, I’m not suggesting to go all-in on Fitbit stock. But if you’re looking for a speculative, contrarian investment, this is it. FIT is troubled, but not to the extent that the bears will have you believe.

The company is also relevant, offering multiple products for a diverse range of demands. Finally, no one expects Fitbit to do anything but fall. Going against the grain could be quite lucrative.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.