Benjamin Graham, Warren Buffett’s renowned mentor, once said that when you buy a stock you should buy it as you would anything in the supermarket. That is, always question how much you’re paying.

In the case of AMZN stock, the answer would be too much. In the past five quarters, AMZN posted a net loss in three, and the others only barely edged into the black. Investors should be asking when Amazon’s (AMZN) hefty capital investments will come back as higher returns.

So far, with Amazon willingly forgoing profits for revenue growth, the answer is in the very distant future. That’s not necessarily the “norm” but, so what, this is Amazon!

Yet, if you believe that Amazon is somehow exempt from the rules of investing, you’d better think again! Wall Street’s history is jam-packed with companies that acted as though the “financial rules” didn’t apply to them. In almost all cases, this ended very badly for investors.

The way Amazon looks today, it seems as if the AMZN stock may be heading in the same direction.

AMZN Stock: Margin and Debt Problems

When a company is profitable and grows, it makes perfect sense to sacrifice some profit margins for more growth. But when a company loses money every other quarter? Then those shrinking margins only reduce the likelihood of future returns.

Click to EnlargeAmazon profits, of course, were barely there in Q2 and posted in the red in Q1. Just a quick look at the company’s gross margin and its 10% shrinkage demonstrates that future profits for AMZN stock are questionable.

Below we compare Amazon’s EBITDA margin against its “net income before taxes” margin. You can clearly see that a widening gap has emerged. Of course, it can’t be tax which is excluded on both sides of the equation. So if it’s not tax causing the gap, what is?

Click to EnlargeIts debt, which AMZN has accumulated quite quickly over the past few years. And that debt is a significant hurdle for AMZN’s profitability.

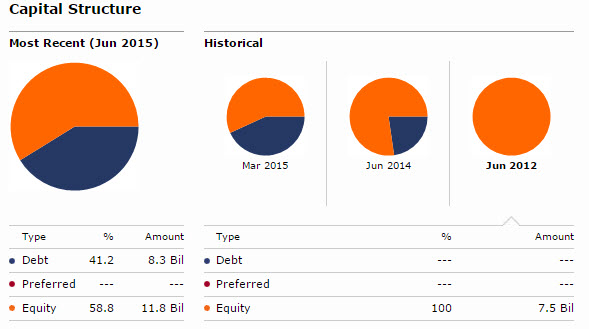

According to the latest capital structure data from Morningstar, AMZN stock had roughly 0% net debt only three years ago. As of June 2015, debt now represents 41.2% of Amazon’s capital structure. Clearly, that’s a massive rise in what amounts to a very short time span.

It’s no wonder that interest payments are burdening the company’s profits. We could derive some comfort if most of AMZN’s debt was maturing in the very long term. Then, long-term funding costs could be locked down on a relatively low basis.

But most of this accumulated debt is set to mature in the next five to 10 years, meaning that Amazon will have to recycle it at a much higher cost. If interest payments are burdening AMZN stock now, what will happen when AMZN has to face much higher funding costs in five years? Most likely, the story isn’t going to end well.

Click to Enlarge

AMZN Stock vs. AMZN Bonds

Many will argue that AMZN stock and its forward P/E ratio of 100 does not reflect the risk of the company. They’ll say that AMZN stock, with revenues that top $20 billion a year, can weather the storm, whenever it comes. That’s a very likely conclusion.

But, let’s consider the aforementioned “marginal” problem and then answer the following questions. Would you rather own AMZN stock at a 100x multiple and hope AMZN somehow flips and becomes meteorically profitable? Or would you rather own AMZN bonds which should guarantee a return of 10% in accumulated yield for the next four years?

Can we be confident that AMZN stock, with its already massive premium, will be higher by 10% in four years? Most likely not. If it’s better to be a company’s creditor than a company’s shareholder then it’s a very bad sign of things to come. To this writer, that’s a sign that AMZN stock is simply not good for its shareholders.

As of this writing, Lior Alkalay did not hold a position in any of the aforementioned securities.