Energy infrastructure company Kinder Morgan Inc (NYSE:KMI) just inked a major deal that will go a long way in its recovery efforts. Signing a ten-year contract Nucor Corporation (NYSE:NUE), the $900 million deal allows Kinder Morgan to continue providing handling, processing, warehousing, and marine services for the steel producer.

Even better than the raw numbers, the contract reflects the effort by KMI to diversify its business. This is part of a broader strategy to recover from the ongoing energy market crisis. But the big question is … will it be enough for KMI stock to break free?

Even better than the raw numbers, the contract reflects the effort by KMI to diversify its business. This is part of a broader strategy to recover from the ongoing energy market crisis. But the big question is … will it be enough for KMI stock to break free?

This could be one of the toughest debates in the markets. Year-to-date, KMI stock is up 34%, a fairly heady performance given the energy sector’s tumultuous ride. In addition, the Kinder Morgan executive team is making the right and often-tough decisions to ensure long-term success. At the same time, the commodity and energy markets aren’t exactly reliable partners.

Although Brent Crude Oil is firmly in double-digit territory YTD, it’s down sharply since early June. Another concern is that the international oil benchmark is down 9% post-Brexit.

On the bullish front, it would be remiss not to include the human touch. KMI, like many of its competitors, operated as a master limited partnership. As InvestorPlace contributor Ryan Fuhrmann notes, the MLP legally skirts the double taxation dilemma that dogs public corporations. That blessed Kinder Morgan stock with generous dividend yields.

Unfortunately, those yields are no longer sustainable in the current environment. Recognizing this, KMI execs made the tough call to curb dividends to a level that can satisfy investors and keep the business running effectively.

KMI’s Strategy

This decision aligns perfectly with the strategy to focus on the most profitable projects and cut down on unnecessary overhead. Since it can no longer afford to rely haphazardly on debt to finance future endeavors, KMI made the decision that its competitors will eventually be forced to make.

Significant progress is already being made, with selling, general and administration expenses in the first quarter of fiscal year 2016 down 12% from the year-ago quarter. Subsequently, Kinder Morgan stock met earnings expectations for Q1 after a lengthy period of bad misses.

Another aspect that could embolden KMI stock buyers is the historical performance of energy infrastructure firms like Williams Companies Inc (NYSE:

WMB).

Click to Enlarge

Since its initial public offering in 1982, Williams’ averages 23% in annual returns. What’s more remarkable, the worst performing years in each of the last four decades average -49%. Yet WMB has found a way to bounce back.

With better leadership, Kinder Morgan stock should at least be able to do just as well as Williams.

Having laid out the bullish argument, it’s not all flowers and bubblegum for KMI. Superior strategy alone won’t overturn the double-digit losses in quarterly revenue overnight. In addition, the balance sheet has been weakened by the volatility in the energy markets. Again, that will take time to reverse, and may stretch the patience of current KMI stock investors.

The Brexit is also an unexpected headache. While it’s not directly related to KMI stock, the dark cloud hanging over the future of the European Union has sent many international markets tumbling. Among them of course is energy. If the appetite for risk continues to be pressured by the Brexit, it could be a long year for just about everybody.

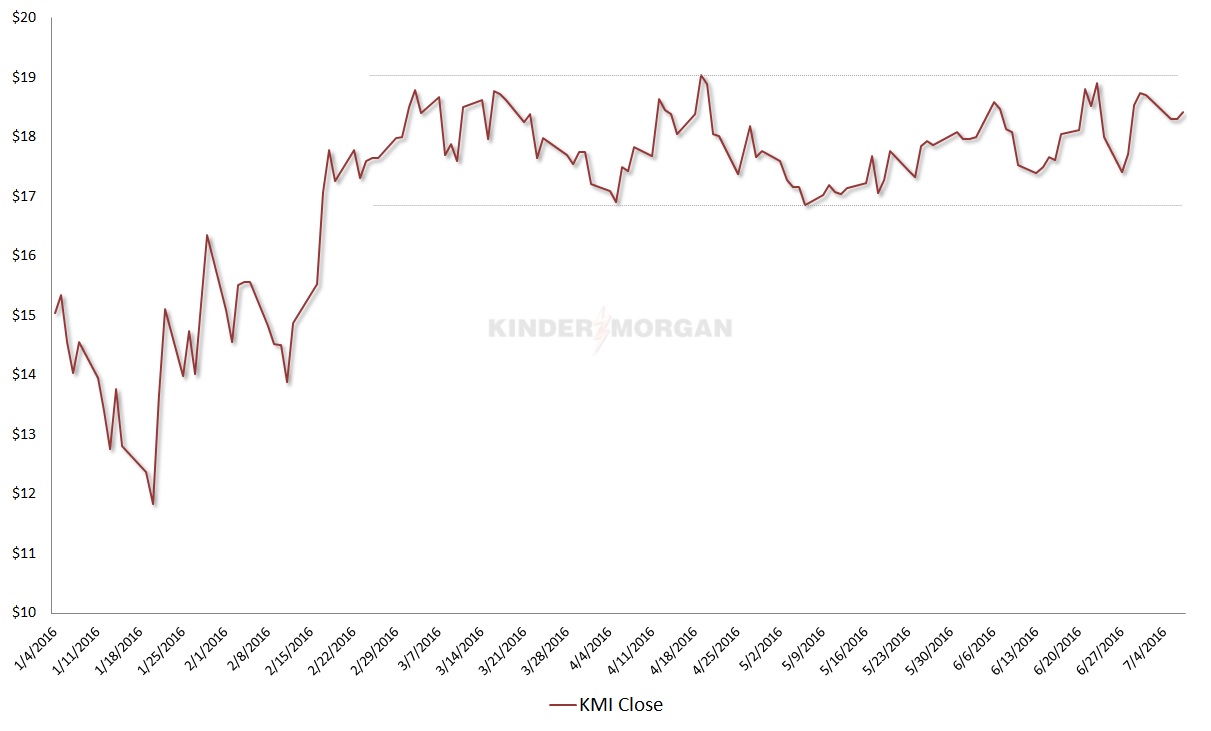

But the real debate for KMI stock hinges on the question: to base or not to base?

Click to Enlarge

Since gaping up in mid-February of this year, Kinder Morgan stock has entered into a tight consolidation pattern. On the upside, KMI finds resistance at $19. On the downside, there’s a support line just under $17. In technical analysis terminology, this phenomenon is known as basing.

Basing is a very common occurrence, usually reflective of a “resting” phase before a stock continues its dominant trend. The problem with KMI stock is that it has been basing for nearly five months.

At some point, there will likely be either a breakout or a breakdown. Some experts see it as a potential reversal. But there’s also risk that Kinder Morgan shares continue to trade sideways. If that happens, even directionally neutral strategies may fail due to lack of net movement.

The basing problem for KMI stock is agonizing, as there are three very real ways to get this wrong. But the one clear factor is this — among its peers, Kinder Morgan stands out.

Management is not just about chasing metrics. Instead, they’ve made tough decisions for the future of KMI. Ultimately, that could be the key that swings the markets in their favor.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.