In the world of commodities, crude oil gets the headlines and gold bullion gets the infomercials, but sugar is often left out in the cold. A prime example of this is the severe decline in sugar prices. Since the beginning of October, its market value has dropped 18%. Did it cause a media uproar? Did Pat Boone urge investors to buy sugar stocks because of an imminent confiscation of sweets by the federal government?

Of course, it’s a rhetorical question. Not too many people outside of commodity traders pay much attention to the price of sugar.

Along with that point, there are not too many “pure” sugar stocks. As of this writing, only three direct plays exist: iPath Bloomberg Sugar Subindex Total Return ETN (NYSEARCA:SGG), Teucrium Sugar Fund (NYSEARCA:CANE), and iPath Pure Beta Sugar ETN (NYSEARCA:SGAR).

Of these, only SGG has somewhat respectable volume, and even then, it’s quite low, averaging only 55,000 shares over the trailing three months.

Here’s the kicker, though — sugar stocks aren’t just limited to funds tracking the actual commodity’s spot price. Rather, they include companies that procure tons of sugar as an integral part of their core business. Food makers, in particular, those specializing in confectioneries and sweetened goods, stand to gain significantly from the sugar deflation. For these sugar stocks, every basis point lost in the commodity markets means an incremental addition to profitability margins.

Best of all — at least from their perspective — sugar deflation is likely to be an ongoing reality. The U.S. Dollar Index shows no sign of abating, actually jumping up 2% for the month so far. A stronger greenback will inevitably weigh on all commodities. Then there’s the whole matter of the U.S. Federal Reserve. If Fed chair Janet Yellen pushes a hawkish policy as many are anticipating, it’s going to be a long day for sugar bulls.

That suits consumer-centric sugar stocks just fine. Declining prices benefit the bottom line, which in turn allows for extra resources to grow the top line. Here are three confectionery companies that can boom on cheap sweets!

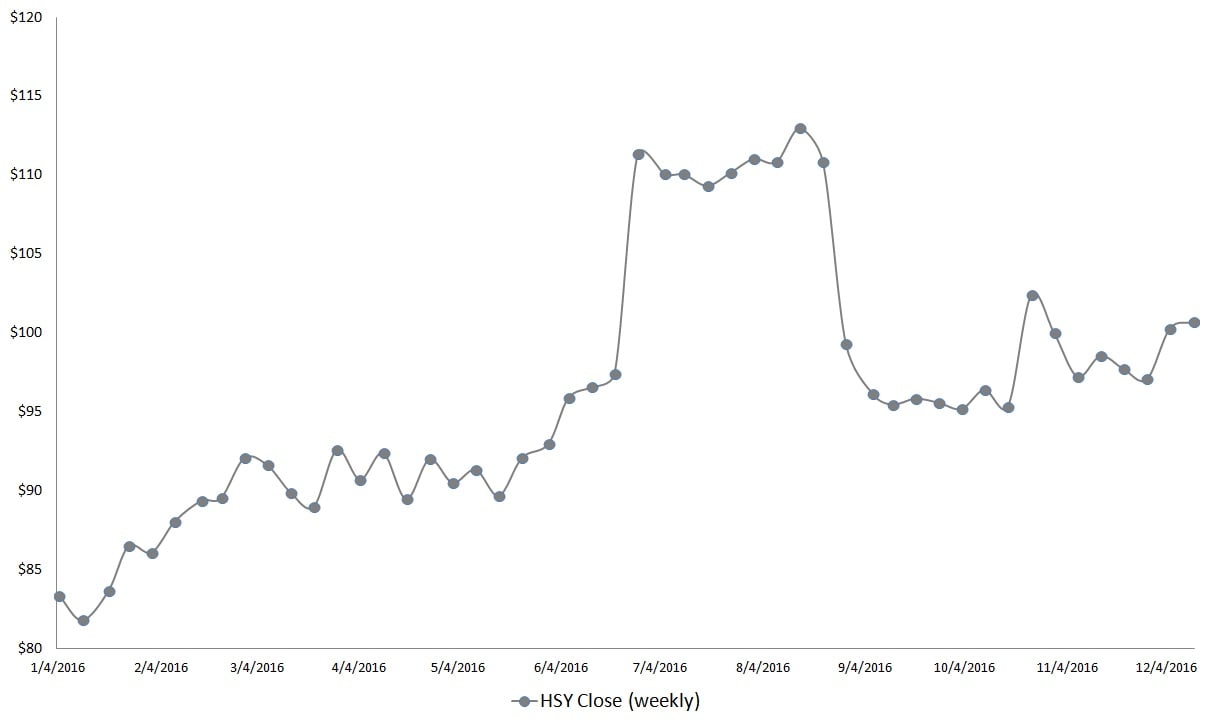

Sugar Stocks to Buy: Hershey Co (HSY)

Click to Enlarge

When it comes to sugar stocks, Hershey Co (NYSE:HSY) is one of the most famous.

According to big data aggregator Statista, HSY is also one of the most patriotic brands. That distinction was no doubt helped by the fact that in 2015, HSY grabbed over 44% of domestic chocolate demand. But another key development might push Hershey to another level.

Recently, HSY indicated that they were exploring the idea of replacing high-fructose corn syrup with sugar in certain products due to shifting consumer tastes. Of course, high-fructose corn syrup has generated a lot of controversy because of its unhealthy attributes. Food companies love it, though, because it is a low cost alternative to sugar.

But with sugar prices falling, this is a perfect opportunity for HSY to pitch its product adjustments in the name of healthy living.

The markets are definitely buying into the HSY story. Year-to-date, shares are up 15%. True, they were up a lot more when rumors of a Mondelez International Inc

(NASDAQ:MDLZ) takeover appeared to be more reality than fiction. But even with that deal collapsing, HSY has charted a steady path to what looks like a full recovery.

With commodity pricing making it a lot easier for sugar stocks to operate, HSY is a name you can’t afford to ignore.

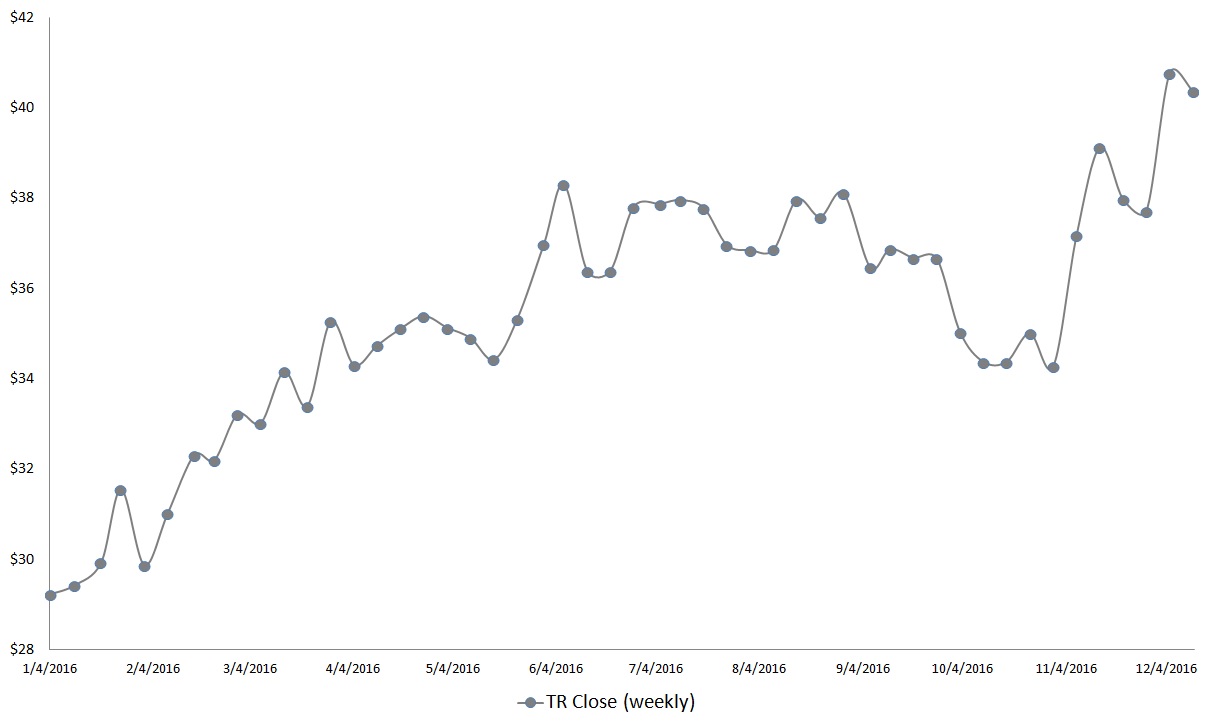

Sugar Stocks to Buy: Tootsie Roll Industries, Inc. (TR)

Click to Enlarge

No company among sugar stocks has as rich and compelling of a history like Tootsie Roll Industries, Inc. (NYSE:TR).

Founded in 1896, inventor Leo Hirschfield names the candy for his daughter. At the time, his hand-rolled candy sold for a penny. During World War II, Tootsie Rolls were included in American soldiers’ rations as a source of “quick energy.”

Today, TR makes 64 million of their core product every day, which equates to 740 pieces of candy per second!

While that sounds like an incredible figure, TR stock hasn’t always had a great time translating production into profits. The one-year period between the late summer season of 2013 and 2014 were particularly rough as TR dropped around 17% of its value. Many questioned whether the company was too old-fashioned for its good. However, TR eventually proved that patience is a virtue. For 2016, the company is up 30% in the markets.

That’s momentum that I expect to continue well into 2017 and beyond. A cursory look at the financials for TR reveals a wealth of positives. It has a cash-rich and stable balance sheet. Free-cash flow is consistently high and fueling its daily operations. Profitability margins are in the upper echelons of sugar stocks, and the deflationary sugar trend will definitely lift all boats.

In short, TR is a smart company with a rich pedigree that should continue to provide reliable returns.

Sugar Stocks to Buy: Rocky Mountain Chocolate Factory, Inc. (RMCF)

Click to Enlarge

Admittedly, Rocky Mountain Chocolate Factory, Inc. (NASDAQ:RMCF) is one of the sugar stocks that’s laced with spice. It’s a speculative opportunity trading in the dark alleyways of the Nasdaq Index.

On a YTD basis, RMCF is down more than 2%. That’s not something to be proud about, especially when so many sectors are experiencing robust rallies.

Despite the obvious choppiness and volatility, I believe there’s an opportunity for RMCF stock. Against the first of June, Rocky Mountain is up over 6%. Although there’s nothing spectacular about that performance in and of itself, it shows a slow transition from bearishness to bullishness. The point becomes more obvious when you realize that in 2015, RMCF lost nearly 16% in the markets. Sentiment started to stabilize in spring of this year, hence my optimism.

Mix in the fundamentals, and RMCF sheds some of its speculative image. For one thing, its balance sheet is fairly stable and it maintains consistent free cash flow. Its profitability margins are ranked in the upper half among sugar stocks, and its trailing three-year revenue growth is quite favorable. Declining sugar prices will just make it more easier for Rocky Mountain to accentuate its strengths.

RMCF is not an investment for everybody. Still, it’s a smart gamble where technical momentum is feeding off industry enthusiasm.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.