Investors were spied buying a downgrade in First Solar, Inc. (NASDAQ:FSLR) in a good sort of way. And if you still don’t mind being a contrarian, a modified fence will put you in stronger position to participate, as FSLR stock continues to heat up off and on the price chart. Let me explain.

Two weeks ago I wrote an article in support of FSLR stock following a terrific earnings beat and solid guidance. It didn’t hurt that Wall Street has not been a fan of First Solar or its alternative energy colleagues for quite some time and shares appeared cheap both on and off the FSLR chart.

Following our analysis, FSLR stock did begin to fire up. Shares of First Solar tacked on roughly 10% over the next several sessions. Then came this past Wednesday’s broad-based ‘Trump Slump.’

We don’t need to get into the ‘what or why’ of the Trump Slump, but needless to say FSLR was, along with the majority of risk assets, a casualty in giving up nearly 5%. But apparently the fairly stiff reversal in FSLR shares wasn’t enough for some analysts, who now remain on the defensive.

On Thursday Baird & Co. cut First Solar to “neutral” from “outperform” while reiterating a price target of $38.

With shares of FSLR rising strongly over the past month analyst Ben Kallo noted concern detrimental tariffs for the U.S. solar markets and would like to see additional “clarity on First Solar’s Series 6 margins or better entry point before becoming more constructive on the stock.”

It sounds reasonable, right? What wasn’t mentioned is Baird’s fairly poor track record in FSLR. The firm’s “outperform” rating was maintained over FSLR’s entire decline from the March 2016 high near $74 and was only consistent in issuing above-the-market and behind-the-curve price target cuts.

Having said that, I’m fairly confident I can do better in FSLR stock looking elsewhere. And for me it continues to be the company’s underlying affirmations of being best-in-breed in the solar complex and now — a supportive chart that suggests other traders aren’t buying what Baird is selling.

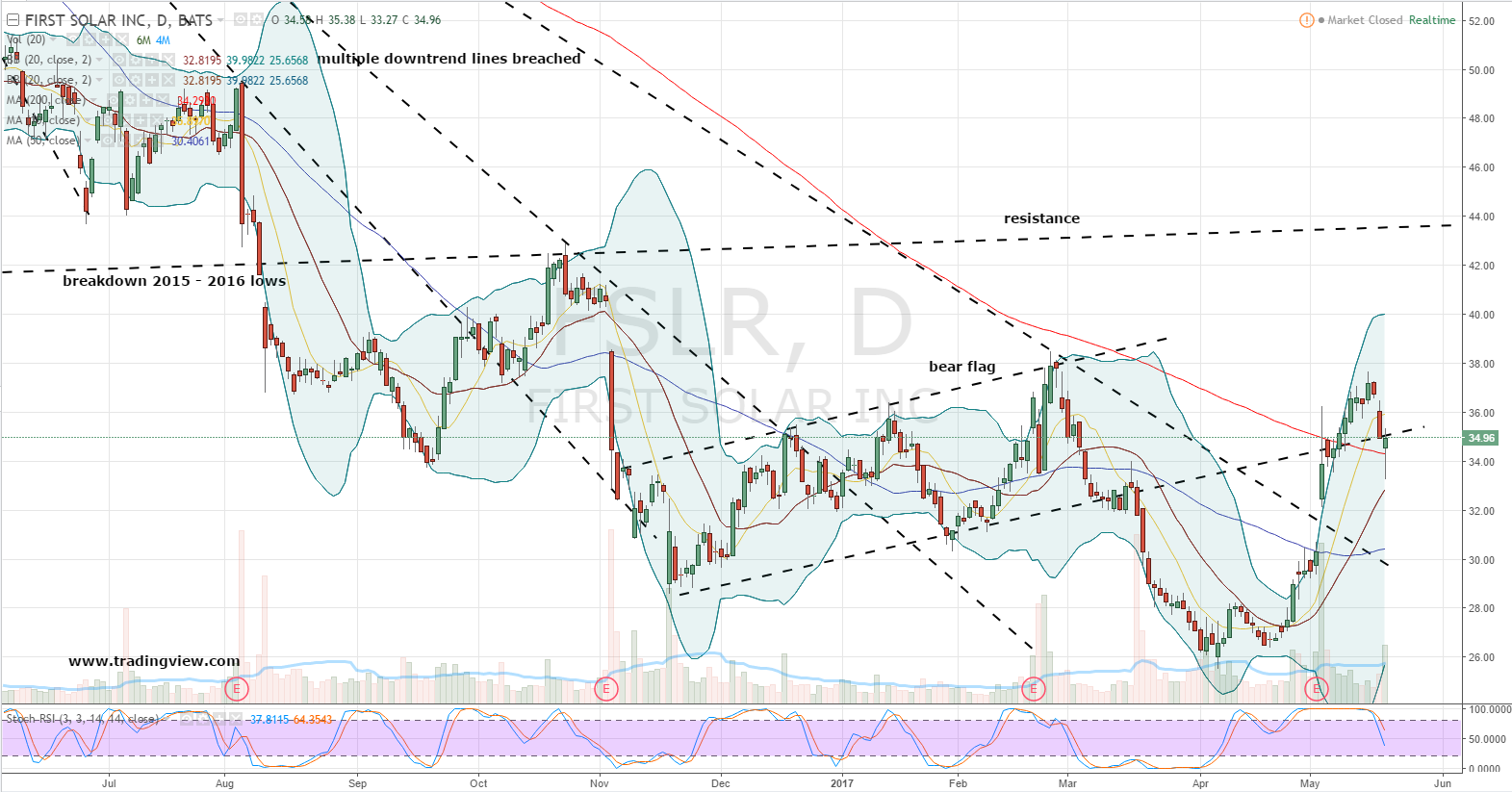

FSLR Stock Daily Chart

Click to Enlarge

Personally, I wasn’t ready to throw caution to the wind with First Solar butting heads with the 200-day simple moving average. Nevertheless, conditions looked ready for higher prices, an eventual confirmation of a new uptrend and a modified collar as a reflection of that view.

I believe a good deal of that desired support occurred Thursday in FSLR stock. A pullback from this week’s relative high has established a very strong-looking bullish hammer positioned around the key long-term moving average.

The bullish reversal strongly suggests other traders weren’t buying Baird’s recommendation, but were instead buying shares of First Solar. In our view the hammer candlestick serves as key pivot low and evidence a bullish price trend is developing, as long as the candlestick remains intact.

FSLR Stock Modified Collar Strategy

Considering the overall bullish view for FSLR stock, I like the idea of approaching shares with a modified fence strategy. The irony here is there’s nothing new under the sun as I discussed this same opportunity this past Monday as part of a gallery article on solar plays.

With First Solar shares closing at $34.96, buying the July $40/$42.50 bull call spread while selling the July $32.50/$30 bull put spread is priced for a mid-market credit of roughly 30 cents.

What’s that get the trader? From $32.50 to $40 at expiration the full credit is captured. That’s nice, but the real heat is above $40. Above the purchased call strike the trader is holding a bullish vertical worth up to $2.80 above $42.50.

And what about the downside? This modified fence combination maintains a breakeven of $32.20 and risk is kept to a max of $2.20 below $30, should FSLR’s bullish earnings reaction price gap get filled.

I don’t know about you but that sounds like more of a reason to consider buying shares at a discount, though Baird & Co. might digress.

Investment accounts under Christopher Tyler’s management do not currently own positions in any of the securities or their derivatives mentioned in this article. The information offered is based upon Christopher Tyler’s observations and strictly intended for educational purposes only; the use of which is the responsibility of the individual. For additional market insights and related musings, follow Chris on Twitter @Options_CAT.