Despite the national attention toward cybercrime, not all cybersecurity stocks have harnessed the momentum favorably. Of the laggards, FireEye Inc (NASDAQ:FEYE) perhaps frustrated investors the most. In 2015, for example, FEYE stock jumped to a near-58% lead at the halfway mark. However, by the end of December, FireEye shares had shed 33%.

The following year was mostly a series of failed promises. FEYE stock gyrated from extreme highs to devastating lows within short periods of time.

This volatility is ideal for day traders — they love skimming profits from speculative bursts in either direction. But for the rest of us, FireEye was a slap in the face. FEYE stock eventually lost 46% in 2016.

Today, investors are hesitant, and for good reason. FEYE stock is up 3% year-to-date, and has gained about 15% since the middle of March. The implied upside is, at minimum, a double-digit annual return, and possibly much, much more. But implications don’t mean anything for the FireEye faithful at this point.

Still, I don’t want to ignore FEYE stock simply based on past misgivings. Stopping and preventing cybercrime is big business. In the U.S. alone, the market is estimated to be worth $18 billion this year, according to InvestorPlace feature writer James Brumley.

That’s a major tailwind for cybersecurity stocks like Check Point Software Technologies Ltd. (NASDAQ:CHKP) and Palo Alto Networks Inc (NYSE:PANW). Both of these leaders have experienced successes and failures, yet optimism remains high due to the industry’s potential.

So what’s on tap for FEYE stock?

New Reasons to Approach FEYE Stock

The biggest fundamental change may not be product-related, but cultural. The acquisitive nature of FireEye was a source of recurring criticism. However, as Mr. Brumley notes:

“… once the company pared back on its buying spree and started thinking seriously about turning a profit, a glimmer of hope started to shine. Specifically, last quarter’s loss was the first one anyone could recall that got smaller on a year-over-year basis.”

The evidence is plain to see on the FireEye financials. For the fourth quarter, FEYE stock registered an earnings per share loss of 35 cents. This represents a 60% paring of losses from the year-ago level. The improvement came most substantially from a 33% reduction in business expenses against the prior year. This shift in strategy caused analysts to bump up their ratings for FireEye.

Of course, the bullishness is not just attributed to changing internal policies. The company recently released a security application called Helix. According to Mr. Brumley:

“Helix is an all-encompassing platform that allows customers to interface with everything FireEye offers. It melds threat detection, threat intelligence and automation, and operates as on-premises software or can be run virtually in the cloud.”

Not only is Helix a potential game-changer, it could incentivize FEYE stock as a buyout target. Clearly, rival cybersecurity stocks are on notice.

Global Demand Will Propel FEYE

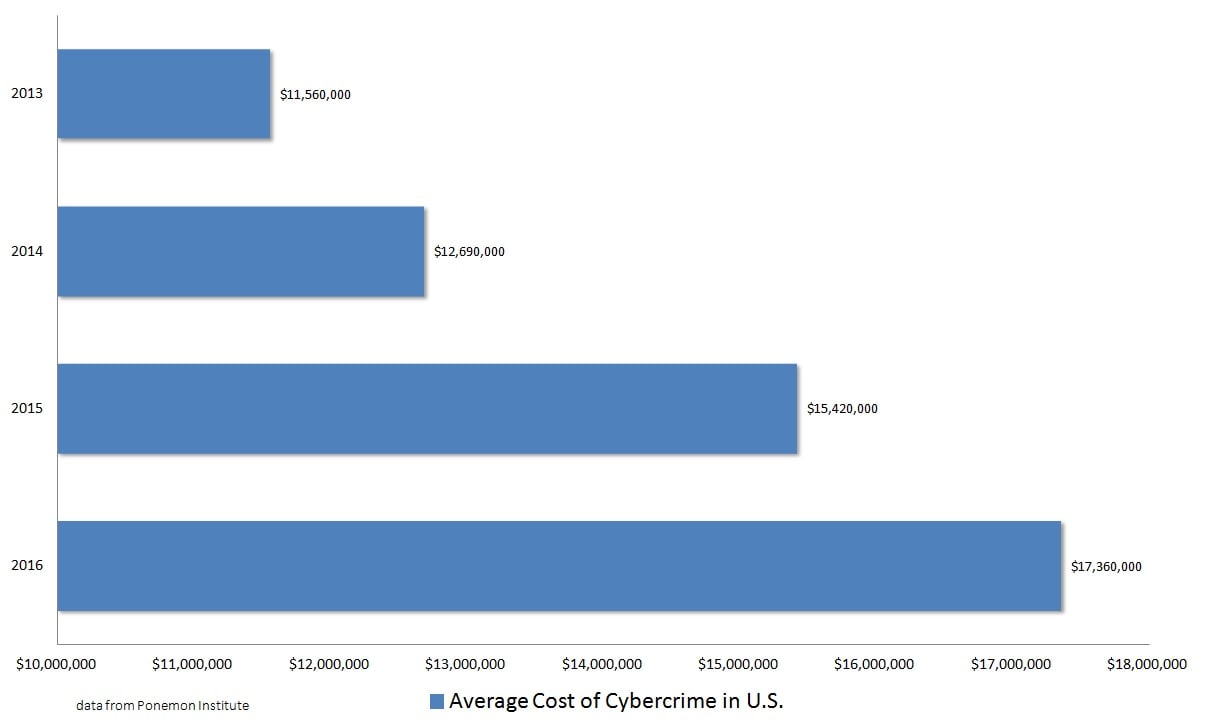

As wonderful as these bullish drivers are, I am most convinced by industry demand. According to the Ponemon Institute, costs related to corporate cybercrimes have jumped across the globe.

Click to Enlarge

But on a growth scale, other countries are witnessing a rapid rise in network vulnerability. In the U.K., average cybercrime costs jumped to $7.21 million from $4.72 million in 2013. That’s a jump of nearly 53%. Japan also has a serious problem, with cyber incidents costing $8.39 million, a near-25% increase from three years prior.

Naturally, this pool of demand is a boost for all cybersecurity stocks, particularly for industry leaders. That said, FireEye doesn’t need to perform a miracle. They must first induce fiscal discipline, which they are already doing. Then, they must stay relevant, which is the whole point of Helix.

Admittedly, the proposition is risky. FEYE stock has hurt plenty of investors. Technically, though, negative momentum appears to have subsided. That could be the markets signaling their broad approval for the changes occurring at FireEye.

I won’t lie — among cybersecurity stocks, FEYE is one of the most speculative. But it also has the greatest upside potential.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.