Shares of Priceline Group Inc (NASDAQ:PCLN) have been on fire this year, up a whopping 29% in 2017. The question is, will that momentum continue after the company reports earnings on Tuesday after the close?

Priceline has the wind at its back when it comes to favorable trends. For the first time in what feels like a decade, consumers seem optimistic about the economy. When consumers feel good, they spend more money and hopefully, in Priceline’s case, take more trips.

Over the past 12 quarters, PCLN has not missed on earnings expectations once. In that same period, they have beat revenue expectations all but twice. Simply put: It’s a solid track record from a solid company.

Expectations for Priceline

So what can we expect from Priceline this time around? Given its track record, it’s hard to imagine PCLN won’t beat expectations once more. The question is, will it be enough?

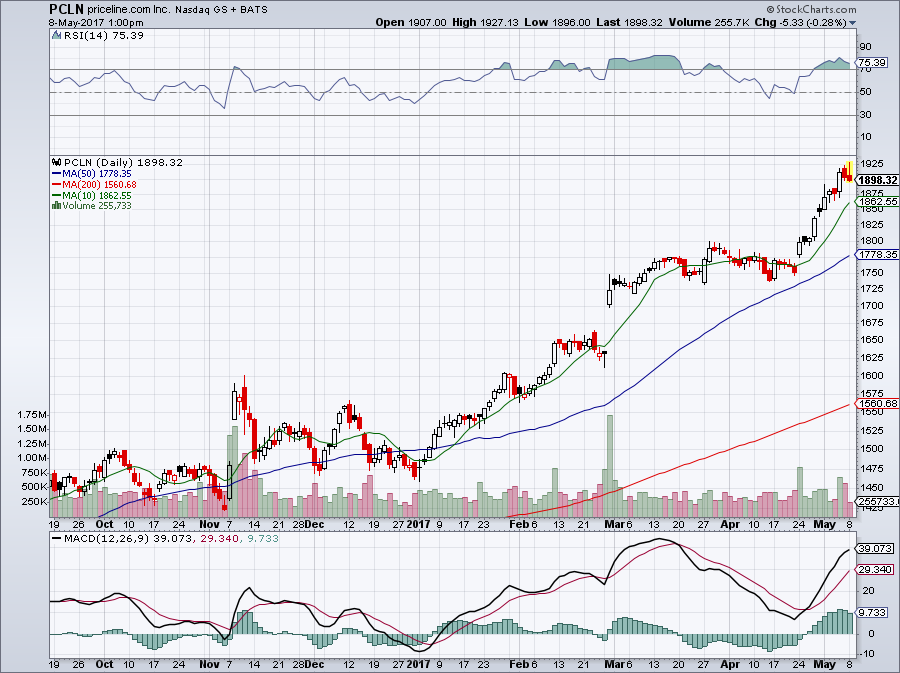

PCLN stock is up 52% over the past 12 months. That’s a sizable rally for any stock, let alone one that sports a $93 billion market cap. As if the rally alone weren’t enough, some have pointed to the valuation as being too high.

Trading at 44.6 times last year’s earnings, PLCN stock appears egregiously overvalued. However, its forward price-to-earnings ratio of 22 is more reasonable. Analysts expect earnings to grow 13.6% this year and 16.6% next year. Given these expectations, the forward P/E ratio is still somewhat high, despite being more reasonable than its trailing counterpart.

The valuation is a little rich for my blood, but it depends on the circumstances. Short-selling on this alone is hard to justify. Likewise, initiating a new position is difficult given the rally and valuation.

For this specific quarter, analysts are looking for earnings per share of $8.89. If it comes to fruition, this would represent a year-over-year decline of 3.4%. Next quarter, though, EPS is forecast to grow 19.3%.

As for revenues, analysts expect YOY growth of 14% to $2.45 billion. Next quarter, expectations are for $3.02 billion or 18.1% growth.

Trading PCLN Stock

I love Priceline as a trending stock — it’s hard not to. It has been a beast and hasn’t found any resistance on the charts. For investors who have been long, there’s nothing wrong with taking some chips off the table after notching a big win.

That being said, there’s nothing in the charts that says the trend will reverse any time soon.

With a strengthening global economy and both consumers and businesses traveling more often, Priceline and its peers like Expedia Inc (NASDAQ:EXPE), Tripadvisor Inc (NASDAQ:TRIP) and Orbitz Worldwide, Inc. (NYSE:OWW) should all do well.

Click to Enlarge

At some point, yes, PCLN stock will struggle. Its stock will not go to infinity. Who knows, it could even be this earnings report that brings it back to earth. If anything, a slight pullback to at least its 10-day moving average could be in the cards.

That’s far from being bearish, of course. Its 10-day average is just a few percentage points below current levels. However, it’s hard to be wildly bullish with a high valuation and a red-hot stock over the past year.

Those who are long PCLN stock can either book some profits or continue to ride the wave until momentum gives way. For those looking to initiate a long position, waiting for a pullback seems prudent. For short-sellers … well, good luck.

Bret Kenwell is the manager and author of Future Blue Chips. He’s on Twitter via @BretKenwell. As of this writing, Bret Kenwell held no positions in any security mentioned.