Micron Technology, Inc. (NASDAQ:MU) had become a favorite pick for investors in 2017. But does 2018 hold the same fate for Micron stock? I wouldn’t bet on another year of 87% returns. However, I feel bullish on MU stock moving forward.

In December, Micron alleviated concerns over its business when it beat on earnings per share and revenue expectations. More important than its fiscal first quarter results, though, was management’s outlook for next quarter.

At the time, the company was expecting revenue of $6.8 billion to $7.2 billion and earnings of $2.51 to $2.65. Both figures were vastly ahead of analysts’ expectations, which were looking for a laughable $6.21 billion in sales and $2.03 in earnings per share.

But wait, it gets better.

Amid the nasty volatility engulfing the stock market earlier this week, management put out some good news Monday. It now sees revenue of $7.2 billion to $7.35 billion and earnings per share of $2.70 to $2.75.

Analysts were only expecting sales of $7.02 billion and earnings of $2.57 per share.

But it still gets even better.

Valuing Micron Stock

What gets better than strong guidance and then revising guidance higher intra-quarter? How about the valuation. Micron stock trades at a ridiculously low valuation. Let’s put it this way: MU stock trades at roughly 15 times second quarter earnings estimates.

With analysts coming up short on initial second quarter guidance, as well as not being high enough on the revised estimates, why would we expect their full-year estimates to be accurate? In any regard, current estimates call for earnings of $10.03 per share. In other words, Micron stock trades at about four times this year’s earnings.

That’s despite estimates calling for 40% growth in sales and 102% appreciation in earnings.

So what’s the deal?

Because Micron stock operates in a boom-and-bust industry, investors aren’t willing to pay up for the stock. Far from a premium multiple, they aren’t even willing to pay a market multiple for MU stock despite the robust growth. Trading at just 6.5 trailing earnings, Micron stock trades at about one-quarter the valuation of the

S&P 500.

That’s not right. So what’s a fair valuation? In my mind, 10 times earnings is more reasonable, but that doesn’t mean the market will do it. In fact, I don’t expect it to. On the bright side, we’re not overpaying for MU. Even if NAND and DRAM pricing is starting to waver, I think there’s enough demand to keep the drive alive.

I’m not alone, either. Two analysts this week — Needham and Stifel — have assigned price targets of $76 and $85, respectively. In fact, the “worst” upgrade this week calls for Micron stock to rally to $53. There were other price targets in between, but even at $53, we’re talking about almost 40% upside.

Trading MU Stock

Despite the positive news and bullish outlook, MU stock is not trading all that well. In fact, it’s given up almost all of its gains associated with management’s uplifting outlook. So what’s an investor to do?

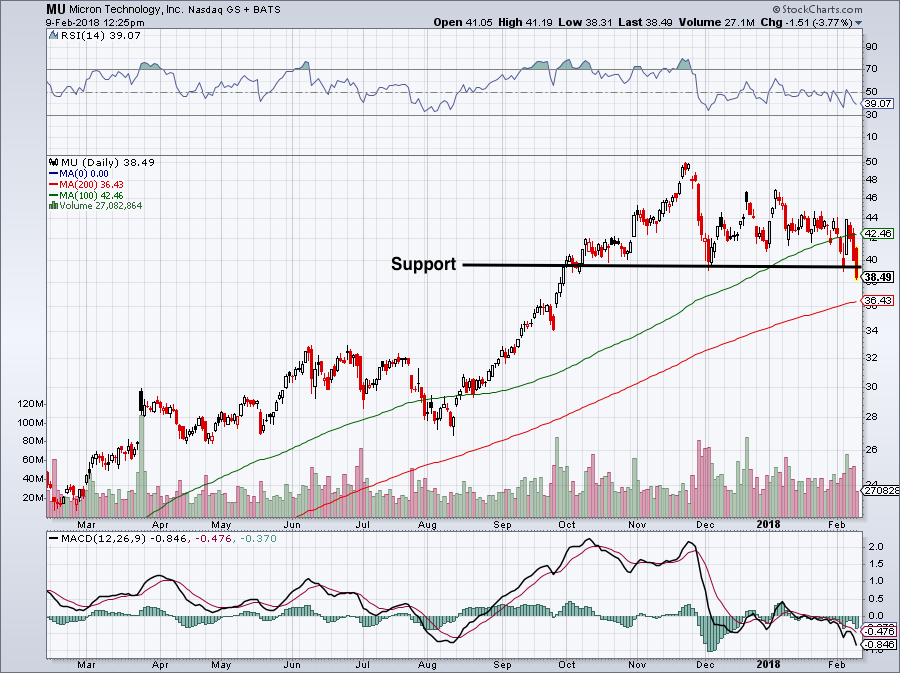

Click to Enlarge

You can see on the chart that there’s been a tight range between $41 and $45. At times, MU stock breaks above or below these levels, but it’s only been temporary since entering this range in October.

The worry now is whether it will hold, as MU stock is currently out of range and below support. Making matters worse, the 50-day moving average has been nothing but resistance this year, while the 100-day does nothing on the support side.

Simply put, Micron stock is not trading well. Because of the strong fundamentals, though, I can’t help but be bullish in this name. What’s it going to trade for, 2 times this year’s earnings? I guess it’s possible, but once the market’s volatility cools a bit, I expect a rebound in MU stock.

If management didn’t revise guidance higher, maybe I would have more doubts about Micron. But the profitability is just too strong to ignore right now. This action feels overdone and temporary.

I have three targets for Micron stock, especially after this round of good news. Target No. 1 is channel resistance near $45, target No. 2 is $47, and target No. 3 is the previous high at $50. Above that, Micron could gain upside momentum.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.