Micron Technology, Inc. (NASDAQ:MU) is working on a rebound in early 2018. After stumbling in late December, Micron stock is trying to prove the doubters wrong and blow through current resistance. Bulls argue that a strong underlying business and low valuation should propel MU stock higher. Bears argue that the fundamentals are beginning to erode.

So who’s right?

Oddly, it seems like both might be. Micron’s NAND and DRAM businesses continue to do well as technology products are in heavy demand from consumers and corporations. On the flip side though,NAND pricing power and concerns over DRAM pricing are real issue that could hurt profitability.

Investors will duke it out on whether these will be fundamental challenges or just bumps in the road. The question facing them is whether paying a paltry 7.3 times last year’s earnings — or 5.5 times this year’s earnings — is too much, not enough or just right.

Where We Stand

Eroding pricing power is a concern and it hurts more than just Micron. It weighs on equipment companies like Applied Materials, Inc. (NASDAQ:AMAT) and Lam Research Corporation (NASDAQ:LRCX), as well. It also hurts others that produce NAND and DRAM products, like Samsung Electronics and Intel Corporation (NASDAQ:INTC).

However, it could benefit chip buyers, including Cisco Systems, Inc. (NASDAQ:CSCO), HP Inc (NYSE:

HPQ) and Apple Inc. (NASDAQ:AAPL).

For Micron’s part, last quarter’s top and bottom-line earnings beat pushed its streak to six straight quarters. Last quarter, DRAM prices represented 67% of total revenue. Smartphones, cloud servers and data centers helped drive DRAM revenue higher by 13% sequentially and 88% year-over-year (YoY). Average selling prices (ASPs) rose in the “mid-single-digit range,” management said on the conference call.

NAND, which represented 27% of Micron’s revenue in the quarter, saw revenue climb 2% sequentially and 47% YoY. ASPs fell in the “low single-digit range.”

In a nutshell, NAND revenue is growing more slowly than DRAM revenue, while its gross margins are in decline. The current situation is not as bullish as when both NAND and DRAM ASPs were both increasing. However, I’d rather see ASPs slip on NAND vs DRAM, which is almost three times larger from a revenue perspective.

We made the case that this year’s analyst estimates — although calling for huge growth — may not be high enough. If fiscal Q2 is any indication, that looks to be the case. Management’s outlook calls for earnings per share of $2.51 to $2.65 on revenue of $6.8 billion to $7.2 billion. Consensus expectations were looking for earnings per share of just $2.03 on $6.21 billion in sales.

Trading Micron Stock

The concern now is that DRAM pricing will erode much like NAND pricing, hurting Micron’s profitability. In any regard though, we have to assign some sort of value for Micron’s business. Generally speaking, Micron stock usually trades with an incredibly low valuation. Making the case that Micron stock price should at least trade with a market multiple is usually a futile effort.

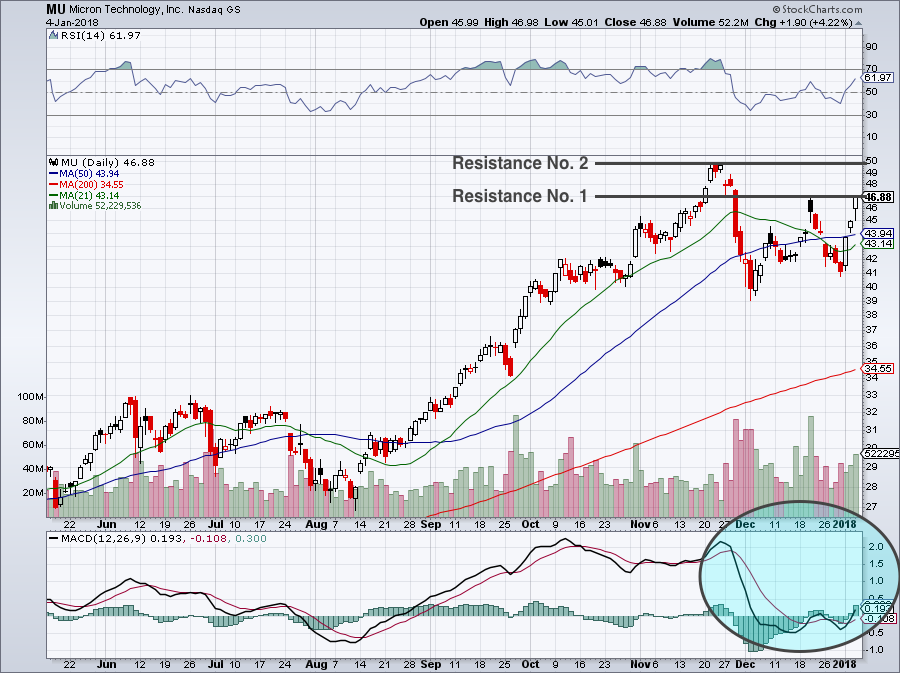

Click to Enlarge

Assigning it a market multiple and saying it should trade at $85 is simply irresponsible and lazy work, in my opinion. The problem with assigning a valuation is that it’s usually opinion. Just because we think it should have a higher valuation, doesn’t mean it will, even if it deserves it. The fact of the matter is, Micron has an ultra-low valuation and betting that it will change its trend now is far from a guarantee.

Analysts forecast 36% sales growth this year and almost 100% earnings growth. Even if 2019 has zero growth, we’re still talking about a company that theoretically could be trading north of $70 by this time next year. That’s assuming the same 7.3 trailing P/E ratio applies, which isn’t unreasonable even for a no-growth company.

On the charts, Micron is looking surprisingly good so far this year. MU stock is near first-line resistance. A push above $46 gets us to target No. 2 near $50. If Micron stock can push through both levels, we have a breakout on our hands, which should be bought so long as the shares stay above $50.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.