Defense stocks have been catching some bids lately, with many hitting multi-month highs. Should that tempt investors on the long side or is this a rally to sell into? The nice thing about defense stocks is that there is a recurring secular market.

Specifically, defense spending seems like the one thing our government can agree on. The government continues to pour hundreds of billions of dollars into various military branches. That bodes incredibly well for aerospace, defense and military-focused tech stocks.

So what are some defense stocks to buy? Let’s look at 3 high-quality names that are on the move.

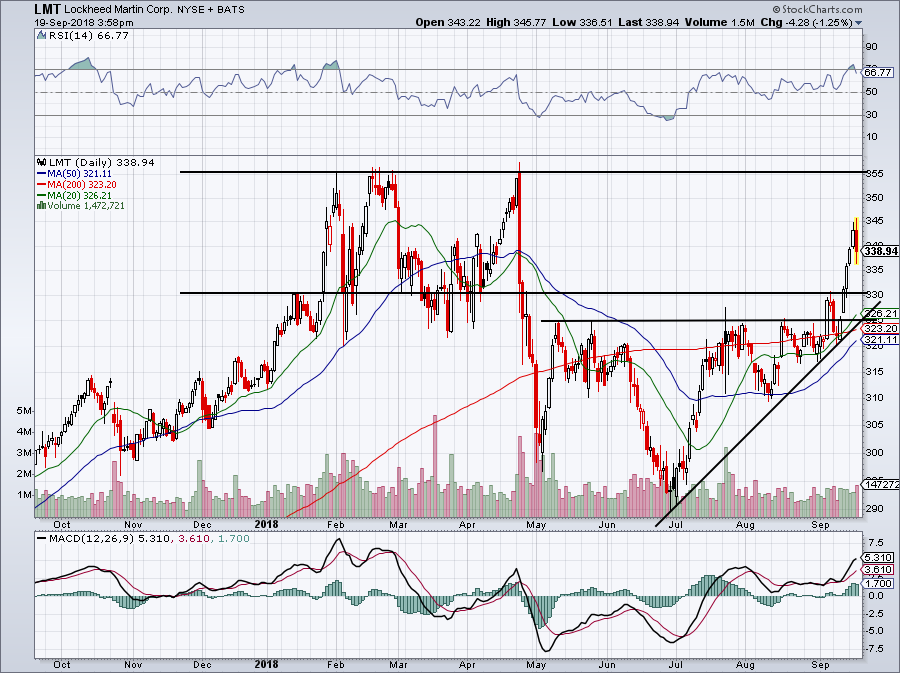

Lockheed Martin (LMT)

Click to Enlarge

One of the biggest and the best names in defense stocks is Lockheed Martin (NYSE:LMT). The stock has certainly had its share of struggles, triple-topping in March and May at $355.

LMT stock lost plenty of altitude, falling below $300 in June and July, finally bottoming near $290.

A week ago, shares were at $320 and now we’re already seeing LMT fight against the $345 level. It’s been a quick rally, but a pullback would be a great opportunity to get bulls re-involved with the name. Specifically, a decline into the $325 to $330 range would bring LMT into various levels of support, as well as uptrend support and moving average support.

I would consider LMT a sure-fire buy should it pullback into that range and hold. That will also give it the energy it needs to retest its $355 highs and possibly push higher.

Analysts expect earnings of $17.10 per share this year, meaning LMT stock trades at just under 20 times earnings. While 3% revenue growth this year and 5% growth next year aren’t extraordinary, 12.4% earnings growth in 2019 is solid.

Plus, the valuation isn’t that bad for a top-quality defense stock that yields almost 2.5%.

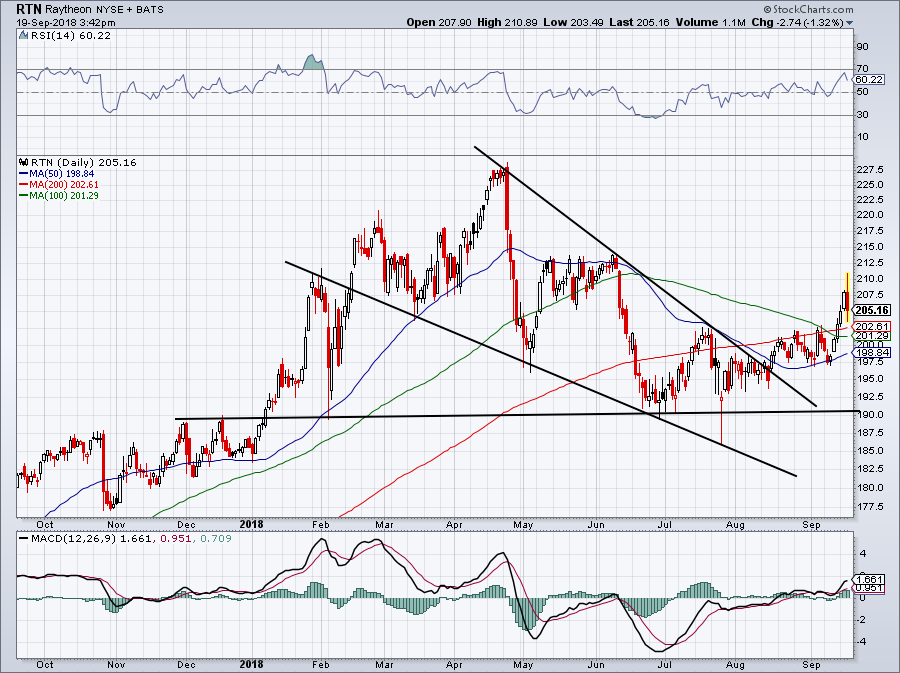

Raytheon (RTN)

Click to Enlarge

Raytheon (NYSE:RTN) might be my favorite defense stock. While it yields less than LMT (just 1.7%) and has a slightly higher valuation, I like the company’s prospects more.

For starters, analysts expect 6.5% sales growth this year and 5.5% growth in 2019. On the earnings front, they expect 30% growth in 2018 and 16.6% growth in 2019. Both metrics are quite solid, particularly given that RTN stock “only” trades at 20.5 times this year’s earnings.

For some, that will be too expensive. But RTN has some of the best missile defense systems available today. That should lead to strong demand for its products in the future, as nations continue to look for defensive ways to counter an enemy attack.

As for the charts, we need to play offense. $190 clearly held as support and that allowed Raytheon to break out of its downtrend channel. Wednesday’s reversal looks ugly though, at least in the short-term.

I would love to see this $198 to $202 level hold as support. If so, RTN is a buy.

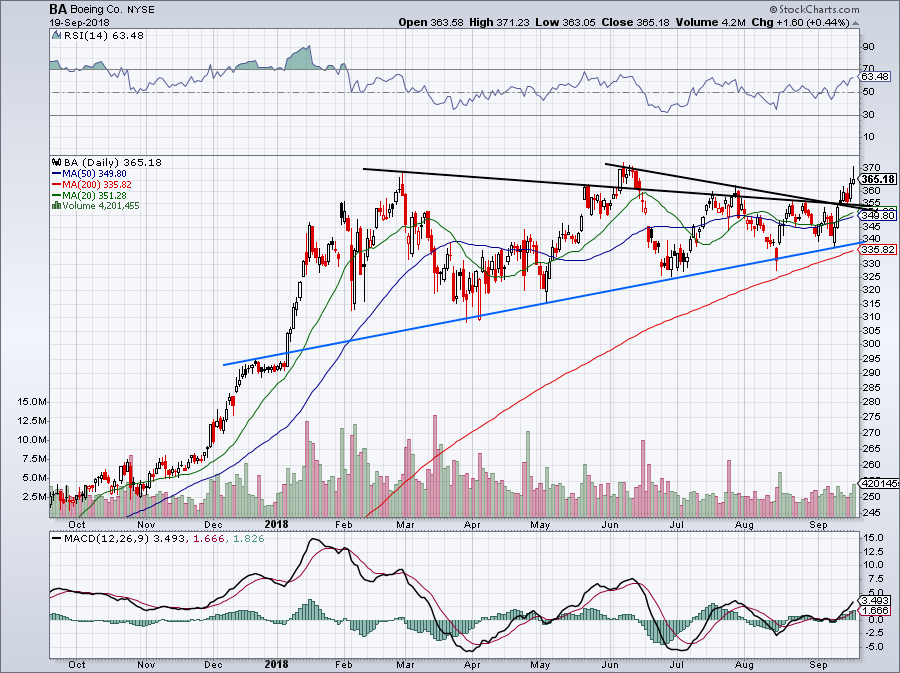

Boeing (BA)

Click to Enlarge

I was very, very tempted to go with L3 Communications (NYSE:LLL) for our third spot, but after Boeing’s (NYSE:BA) breakout, it’s just too hard to ignore.

Shares broke out over two downtrend marks, both near $355. That level will be important to watch on a pullback. Keep it simple with BA. If a pullback into the $350 to $355 area holds as support, it’s a buy. It gave its prior highs near $370 a shot on Wednesday and couldn’t push through. That may cause it to consolidate for a few days.

On the flip side, long-term uptrend support (blue line) has been holding. Any substantial pullback in the stock market or in BA specifically could bring us back to this level.

From a fundamental standpoint, BA stock is a bit pricey at ~24 times this year’s earnings. However, it’s got a huge backlog of orders and is a free cash flow machine. That bodes well for its massive buyback plan and consistent dividend, which yields about 2%.

The company has beat earnings and revenue expectations for four straight quarters, making analysts’ estimates perhaps too conservative. As they stand though, consensus expectations call for 5.5% revenue growth this year and 6.5% growth next year. Earnings are forecast to grow 42% in 2018 and more than 20% in 2019.

That’s pretty darn good in my book.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.