A look back at its recent headlines and results doesn’t exactly make Chesapeake Energy (NYSE:CHK) out to be a “must-have” kind of name. Although CHK stock has held up better than the broad market this month, so too have peers like Cabot Oil & Gas (NYSE:COG) and Southwestern Energy (NYSE:SWN). The resilience from Chesapeake Energy stock may have more to do with the resilient price of oil and gas than it has to do with the company itself.

On the other hand, while it’s difficult to see through the fog of change, a myriad of efforts are on the verge of finally coming together for Chesapeake Energy — all at the same time. Once they do, not only will the recent strength make sense, the market could easily justify much higher highs for CHK stock.

Weighed Down

As has been the case for most energy names, Chesapeake Energy has been a work in progress for a while. One could even argue that Chesapeake has had a tougher time than others shrugging off the impact of the 2014/2015 implosion of the fossil fuel market.

Case in point: As Thomas Scarlett pointed out less than a month ago, the most recently reported quarter indicated capital expenditures still in excess of EBITDA, while Dana Blankenhorn explained earlier this month

that higher-interest rates on new debt issued to replace old debt — waiting on its Powder River Basin projects to reach full stride — was a dangerous game.

In the meantime, though natural gas prices are up 20% from the multi-year low hit early this year, they’re still down from their late 2016 peak… after oil prices were well on the road to recovery.

The stars aren’t exactly lining up for Chesapeake Energy. But, maybe, they’re about to.

Daybreak

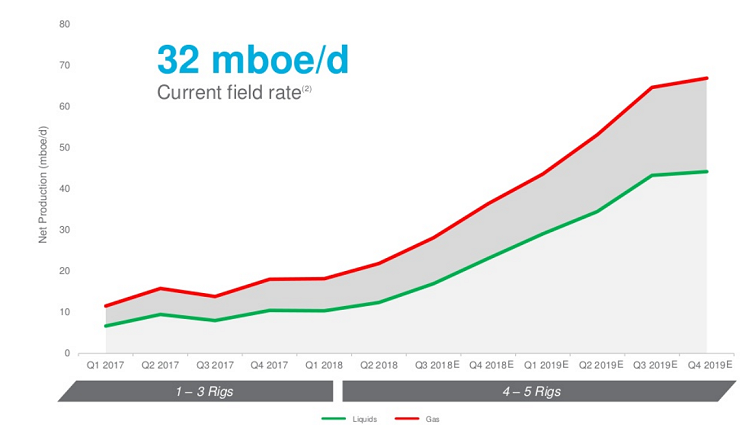

Any fan or follower of CHK stock has to recognize by now that its Powder River Basin projects are expected to be its growth engine of the future. It said as much, literally, when it officially announced the sale of its Utica Shale property in July. The statement from the company:

“The Powder River Basin in Wyoming continues to develop into the oil growth engine of the company, as recently demonstrated by a 78 percent increase in net production compared to the average 2017 fourth quarter rate. On July 22, 2018, total net production hit a new record of approximately 32,000 net boe per day (42% oil, 41% natural gas and 17% natural gas liquids), compared to an average 2017 fourth quarter rate of 18,000 boe per day. Chesapeake now projects net production from the area will reach approximately 38,000 boe per day by year-end 2018, and expects total net annual production from the PRB to more than double in 2019 compared to 2018.”

Nothing’s changed in the meantime, except the current date on the calendar. We’re closer to the end of 2018 than not, and 2019 is right around the corner. Chesapeake Energy’s business outlook posted last month still points to a doubling of the Powder River Basin’s output by the end of next year.

Click to Enlarge

The ramp-up of the Powder River Basin’s projects is already underway though, setting the stage for what could prove to be an explosive response to its third-quarter and fourth-quarter reports for this year, the first of which is slated for Nov. 1. Despite negative free cash flow for the better part of the past few years, the company is now talking about “free cash flow neutrality.”

When exactly that might happen isn’t perfectly clear — probably not even to the company. Oil and gas price volatility as well as geopolitical turmoil makes any suggested timeframe a moving target. It wouldn’t be out of line, however, to suggest we could see measurable progress on that front in the upcoming quarterly reports.

Bottom Line for CHK Stock

Against this sort of backdrop, the seemingly unlikely strength seen from CHK stock in recent weeks makes some sense. In fact, there’s an argument to be made that Chesapeake Energy stock may actually under-reflect the potential fiscal improvements that loom ahead.

In that vein, the forward-looking operating price-to-earnins ratio of 5.9 is inviting — and them some. It’s also a valuation measure that requires a major footnote. That is, the gap between GAAP and non-GAAP results is still significant from time to time, even if not gaping. The gap is narrowing though, and that projected valuation is based on earnings figures that won’t be too far away from Chesapeake’s actual, GAAP bottom line a year from now.

The next step? Getting more investors to believe in the turnaround enough to get CHK stock over its technical hump.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.