Depending on who you ask, stocks may or may not have have entered a bear market in late 2018. On an intraday basis, the S&P 500 , represented by the SPDR S&P 500 ETF Trust (NYSEARCA:SPY), did drop 20% off its recent highs in December. But, on a closing price basis, the index narrowly avoided a 20% drop, and has rebounded strongly ever since.

Regardless, concerns about a bear market have been swirling around financial markets for several months now. Against that backdrop, it was interesting to see a Barron’s article over the weekend which essentially said that stocks — despite being in the midst of the longest bull market ever — are on their worst 20-year stretch in terms of compounded returns since the Great Depression. Because of such, the article proposed that stocks could actually be in store for a big boom over the next 20 years.

Is this true? In the big picture, is it really possible that this longest bull market in history might go on for a lot longer?

Yes and no. On the yes side, valuations are low, the economy is healthy, earnings growth is strong and the outlook for the bull market to persist in 2019 and 2020 is favorable. On the no side, trailing compounded returns in every other window beside the 20-year window imply that we are due for a correction soon.

Thus, the broad takeaway here is that the bull market still has runway over the next few quarters and years. But, the prospects of this bull market lasting another five-plus years lack visibility and are historically unsupported. As such, investors have every reason to be bullish in 2019, but should exercise caution and carefully monitor the fundamentals thereafter.

What The Data Says About a Bull Market

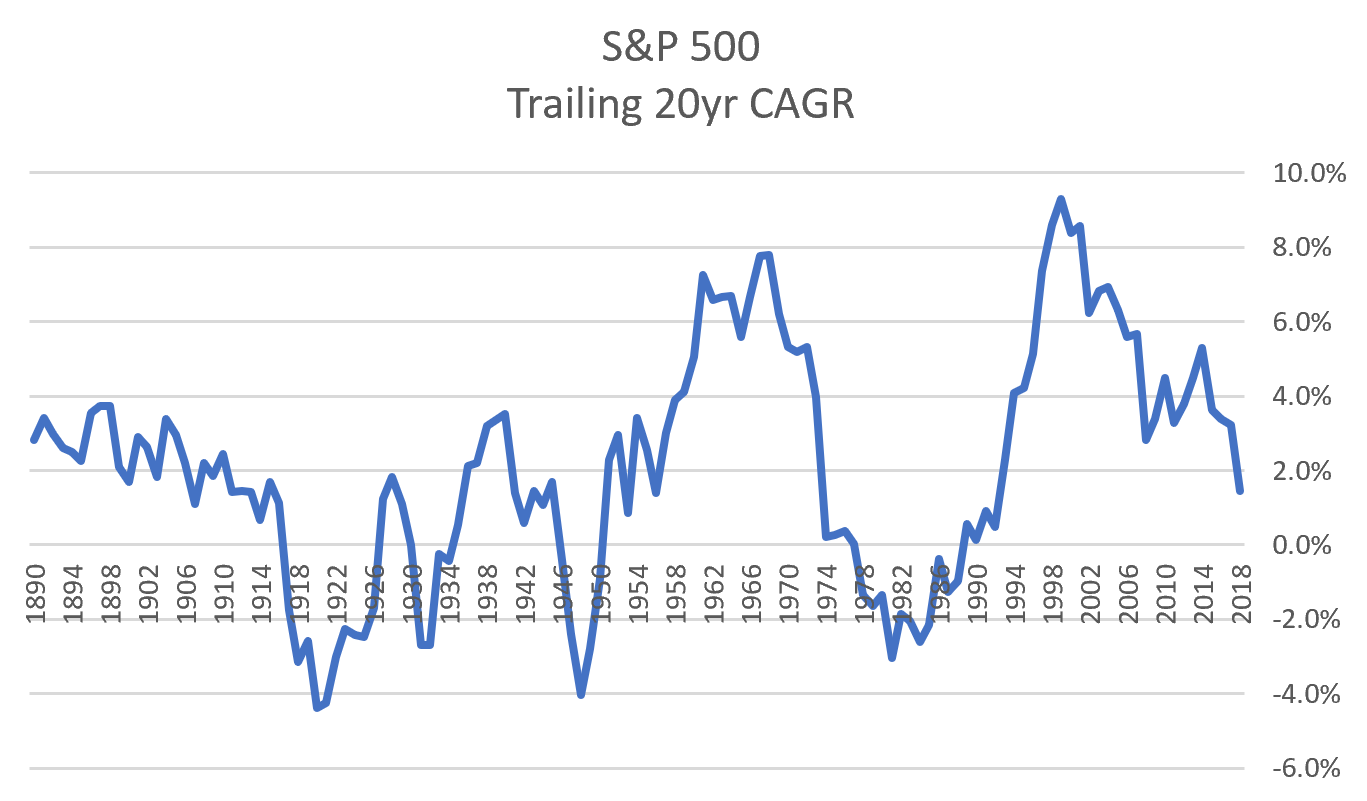

Click to Enlarge As the

Barron’s article correctly points out, stocks are on a bad 20-year stretch in terms of compounded returns. This is true even on an inflation adjusted basis. Over the past twenty years, inflation-adjusted compounded annual returns for the S&P 500 measure out to 1.5%. Since 1890, the average mark is 2.1%. Moreover, as the chart illustrates, trailing 20 year compounded returns run in cycles, and we are currently in a trough in that cycle.

But, this analysis misses one critical point. Twenty years ago, stocks were entering the peak of the Dot Com Bubble. Thus, the comparison year is artificially inflated by one of the biggest valuation bubbles in the history of the stock market. Naturally, that will dilute trailing-20-year returns.

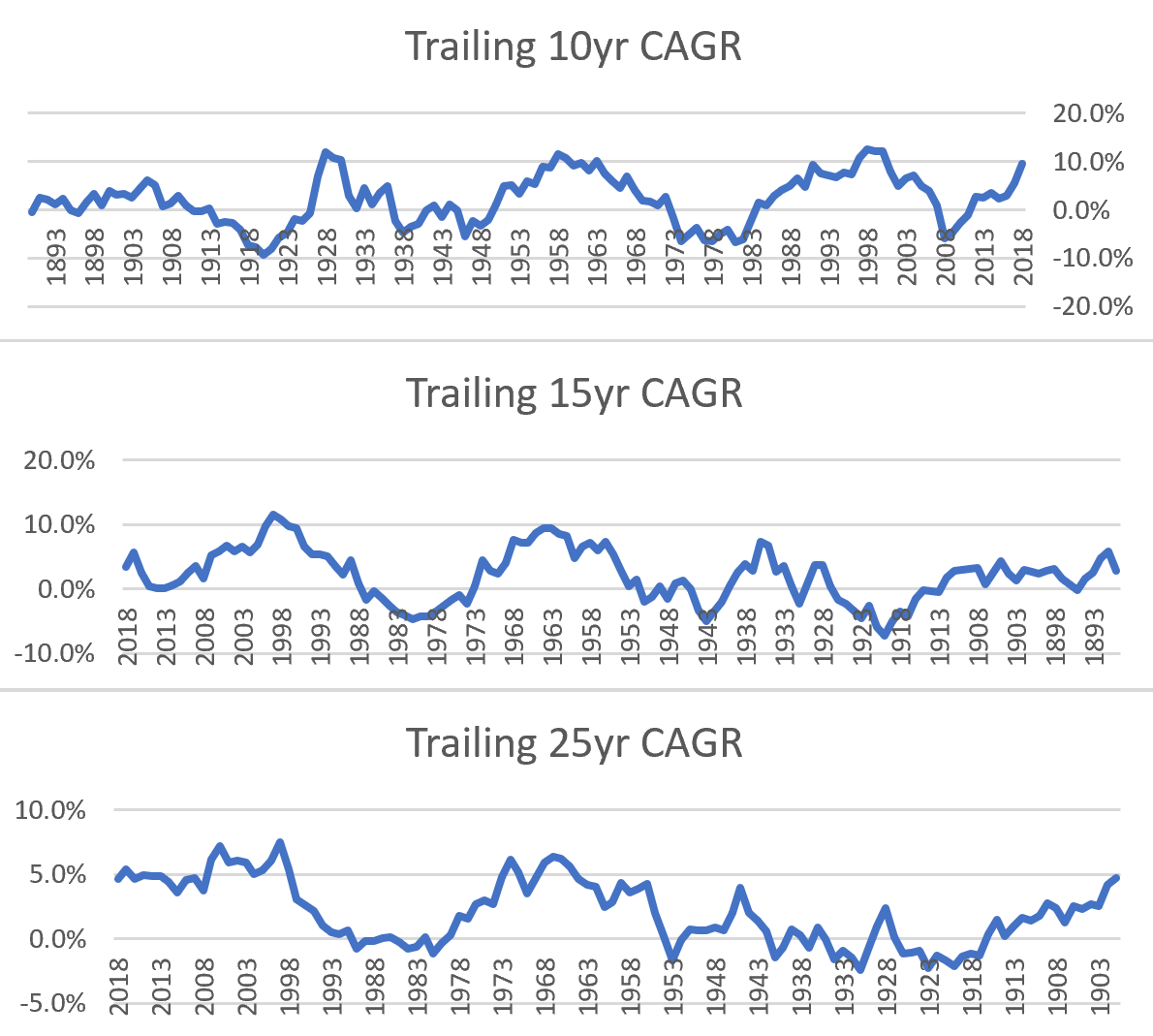

Indeed, if we look at trailing compounded returns through any other time period, the outlook is less bullish. On a trailing-10-year basis, inflation-adjusted compounded annual returns are just below 10% and at a peak. On a trailing-15-year basis, that mark is above 3% and also near a peak. Same is true on a trailing-25-year basis.

Click to Enlarge

Thus, if you look at essentially any other time frame beyond the trailing-20-year horizon, there’s no reason to believe that the next “x” years will be better than the past “x” years. Instead, the conclusion is that the next “x” years will likely be worse than the past “x” years.

How It Lines Up With Fundamentals

The aforementioned trailing compounded annual return analysis lines up with the fundamentals underlying financial markets at the current moment.

Heading into 2019, the outlook for the bull market to live on is quite favorable. Valuations are as low as they’ve been in several years, and are essentially pricing in a sizable economic slowdown. But earnings haven’t come off their all-time highs, nor are they projected to fall in the foreseeable future. The U.S. economy continues to add hundreds of thousands of jobs per month and sport a near-record-low unemployment rate. Consumer and business confidence remain very high. The rate hike headwind is backing off. Progress is being made on the trade war front.

All together, there are plenty of reasons to be optimistic about stocks in 2019. Stocks sold off in preparation of a recession. That recession isn’t coming anytime soon. As such, stocks should rebound.

Eventually, though, some black swan will emerge to kill this bull market. History says this black swan will come sooner rather than later. As such, after 2019, the outlook for stocks lacks visibility.

Bottom Line

Investors have every reason to bullish on stocks in 2019, but the idea that this bull market will live on forever is a pipe dream. Eventually, this bull market will be killed like all bull markets, and history says that will happen sooner rather than later.

As of this writing, Luke Lango did not hold a position in any of the aforementioned securities.