Admittedly, the turnaround story Under Armour (NYSE:UAA, NYSE:UA) is piecing together hasn’t always been pretty; at times it’s been difficult to comprehend. You’re not crazy, however, if you find yourself increasingly interested in owning Under Armour stock.

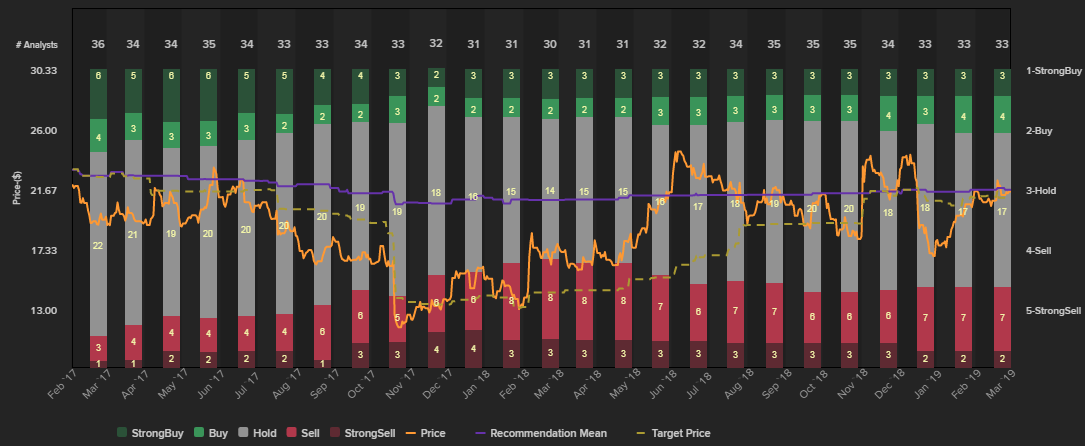

But that’s not the consensus opinion on Wall Street. Indeed, analysts’ consensus target price of $20.96 is actually below the current value of UAA stock. Meanwhile, analysts’ average rating on Under Armour stock is a “Hold,” but that’s likely due more to courtesy than anything else. The pros generally don’t give any stocks “Sell” ratings, and they’ve certainly shown no interest in upping their targets on UAA stock as the shares have risen meaningfully above their December lows. That’s a bit unusual, since analysts usually raise their price targets on stocks that are rallying.

This may be one of those relatively rare cases, however, in which individual investors are going to have to make their turnaround bets without the support of analysts.

Slowly But Surely

Under Armour’s turnaround began in 2016, though it didn’t fully gel until a year later. The turnaround is still fluid, with UAA recently cutting 400 jobs and implementing other cost-cutting measures. Under Armour has also created different strategies for different geographical markets.

The reasons why the turnaround is necessary have never really changed, though. Those reasons are competition from the likes of Nike (NYSE:NKE) and Adidas (OTCMKTS:ADDYY) in an environment in which consumers’ preferences are shifting.

Under Armour CEO Kevin Plank’s work on the turnaround has borne occasional, but uneven, fruit. Some analysts still doubt that the turnaround is working at all.

Canaccord Genuity analyst Camilo Lyon is one of those doubters. In December, he wrote: “Investor expectations already appear elevated, suggesting the company will rapidly return to high-single-digit earnings before interest and taxes margins on high single to low double-digit revenue growth over the outlook period (most likely three years),” but added he has “serious doubts about…how Under Armour will get there.”

The company’s fourth-quarter report

, however, once again indicates that UAA is lurching forward. Its sales increased 3%, excluding currency fluctuations, and its gross profits improved from 43.4% of its revenue to 45.0% of its revenue after UAA cut down on the discounts it offers.

Also noteworthy was the reduction of its long-term debt, which totaled $703.8 million last quarter versus $765.0 million as of the end of 2017. Consequently, its interest expenses fell from $9.3 million in Q4 of 2017 to only $7.3 million last quarter.

Perhaps most encouraging of all is how much Under Armour was able to grow its overseas business, offsetting the 2% decline in its revenue from North America, whose athletic-apparel market is becoming saturated.

UAA is rethinking everything from the top down, including its marketing and product-development efforts in North America.

UAA’s turnaround is not perfect. But it was never going to be. As Oppenheimer Funds analyst Brian Nagel commented after the company’s fourth-quarter results were released, “… here’s Under Armour turning its business around and getting back on its footing, it’s not doing that in a vacuum. It’s doing that against the likes of some very strong companies that are innovating in their own right.”

Still, the pros seem oddly insistent that the turnaround just isn’t working, and that the few flashes of brilliance seen in recent quarters won’t last.

Pessimism Abounds

Here are a couple of examples: Bloomberg Intelligence’s analysts wrote “The first phase of Under Armour’s turnaround — inventory reduction and margin expansion — is near completion, and focus shifts to reigniting the brand, which in our view could prove more challenging.” B.Riley’s Susan Anderson pointed out “Today’s report showed a worsening top line both from DTC (direct-to-consumer) and international, which are UAA’s two top growth drivers, and deteriorating international profit, which is expected to be a margin driver longer term.”

Both concerns, and other, similar warnings, are valid. But UAA’s turnaround was never going to be quick or easy.

Click to Enlarge

Institutional and even individual investors, conversely, sometimes have better vision than the professional stock pickers, who, by the way, despite their reservations, are still calling for respectable (even if not riveting) revenue and earnings growth this year and next. The latter situation is unusual, though not unheard of.

What’s Ahead for Under Armour Stock

There could soon come a time when many analysts have to upgrade Under Armour stock or face the risk of missing out on an opportunity.

When and if that happens, however, will largely depend on how UAA stock performs in the foreseeable future.

Though Under Armour stock is up since late 2017, the shares’ rally has been thwarted a couple of different times. The bears have drawn a clear line in the sand, though. A technical ceiling has taken shape around $24.60. If Under Armour stock can get past that hurdle, a breakout thrust could ensue and spark some upgrades, which often fan the bullish flames. Psychology remains a key factor in the performance of UAA stock.

Click to Enlarge

Kevin Plank and the rest of the company, in the meantime, have already been doing what they’re supposed to be doing to support such a rally.

The Bottom Line on Under Armour Stock

Investors arguably should not sweat analysts’ lackluster outlook on Under Armour stock. The analysts may have a jaded view of UAA based on the company’s past, and they may not have their fingers on the pulse of the company’s consumer-facing changes.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.