Apple (NASDAQ:AAPL) is off its lows, but it hasn’t been an easy ride for Apple stock. At one point it was worth more than $1 trillion, and the company’s stock was immune to the initial fourth-quarter breakdown. Its tanker-like size deflected the growing waves of volatility with ease, seemingly safe while others names were swept up in the storm.

Then it cracked.

Apple stock got hit and the tanker started taking on water. Then a lot of water. From peak to trough, AAPL stock fell more 40%. But that’s not something we haven’t seen before and in fact, has historically been a great buying opportunity. Do we have that opportunity once again?

Apple’s Business Model

The company’s lifeblood is the iPhone, but it has an array of other revenue lines too, including: Mac, iPad, Services and Wearables, Home and Accessories.

Critics will quickly point out that China revenue fell 26% year-over-year (YoY) in the latest quarter, while iPhone revenue stumbled 15%. This led to a 4.5% YoY decline in overall sales. That’s not good, especially with Apple emerging from the holiday period. But it’s also true that the Chinese economy is under pressure from the trade war, which hurts iPhone demand, and thus revenue. It’s not solely an Apple issue.

Further, can we even pretend that $52 billion in iPhone sales is really that disappointing? Especially when Services churned out $10.9 billion in sales or that Wearables, Home and Accessories did $7.3 billion in sales, up 19% and 33% YoY, respectively.

These categories, which were negligible according to critics not all that long ago, accounted for more than $17 billion in revenue or roughly 21% of total sales. But the growth rate is the truly impressive part of these categories. It’s what will carry the company’s long-term revenue growth and help drive profitability. By the way, the Services unit that’s at a $40 billion a year run rate and growing, is kicking out gross margin of almost 63%, almost 70% more than the company’s overall gross margin of around 37.5%.

Is Apple perfect? Of course not. But its business model is akin to the razor/razor blade model — provided the razor company is selling its razor for an immense profit too.

Balance Sheet and Value for AAPL Stock

While many like to chide Apple for its buyback and seeming lack of innovation, what else is Apple to do? Admittedly, past M&A would have been accretive in hindsight, but we could say the same for almost any large cap company, Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) and Microsoft

(NASDAQ:MSFT) included. Plus, the company can only pour so much into R&D.

Its strong cash flow generation has allowed Apple to amass a war chest of capital. Over the past 12 months, Apple has generated operating cash flow and free cash flow of ~$76 billion and ~$62 billion, respectively. Future cash flows aren’t guaranteed, but thanks to Apple’s superior business model laid out above (profitable product sale + high-margin Services revenue via product use), it’s slowly turning it toward a software and services company with a subscription-like hardware business. Even with flat sales each year and stable margins, the company would be generated close to $60 billion in annual free cash flow.

With more than $85 billion in cash and short-term securities, Apple has more than enough cash on hand. Total current assets outweigh total current liabilities $140.8 billion to $108.2 billion. Total assets of $373.7 billion is $110 billion more than the $255.8 billion in total liabilities.

Admittedly, earnings and revenue growth are each forecast to fall about 4% this year. In that sense, some investors may not find Apple stock attractive at 15 times earnings. But with this strong of a balance sheet and surely another capital distribution plan to be announced on the next earnings call, there are worse stocks to bite into.

Trading Apple Stock

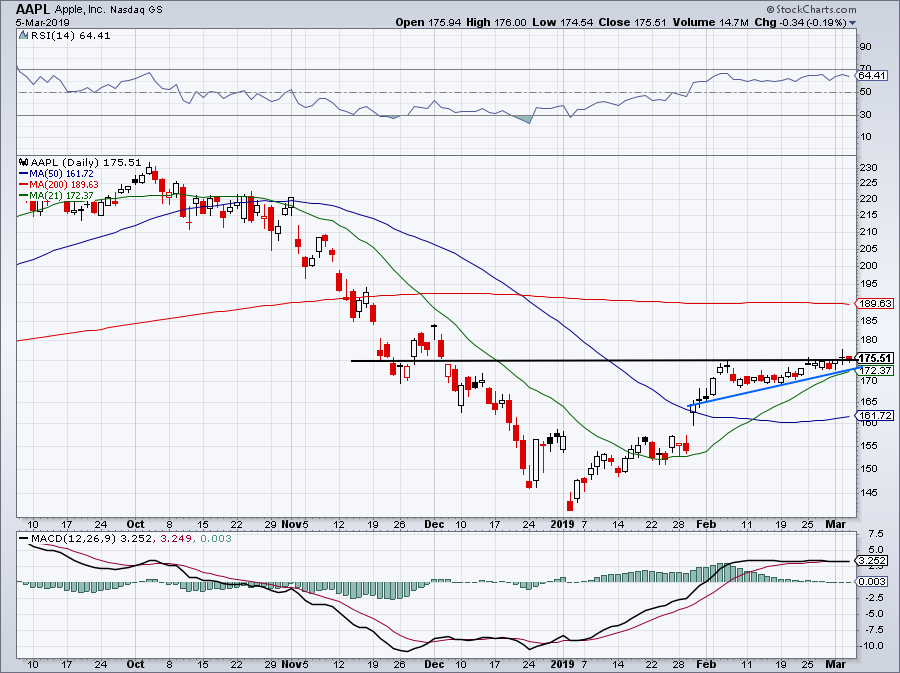

Click to Enlarge

The Apple stock price continues to move in a super tight range. Uptrend support and the 21-day moving average continue to grind AAPL stock up to $175 resistance. The level is seemingly giving way, but we’re not seeing any fireworks just yet.

If Apple can take off, it could have room up to $185 and possibly $190. The latter of the two levels brings in the 200-day moving average. Below uptrend support and the 21-day moving average, and Apple stock will need to reset. It may test the 50-day in the meantime, should support give way.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AAPL and GOOGL.