It’s often a sign to buy when big pension fund managers up their stake in a stock. In the first quarter, Dutch-based PGGM upped its investment in Verizon Communications (NYSE:VZ) by 46% to $218.3 million, prompting me to wonder if now’s the time to buy VZ stock.

Here’s a simple yes-and-no answer to this question.

VZ Stock is a Buy

PGGM is the second-largest pension fund manager in the Netherlands, managing assets worth EUR 211 billion ($236 billion) for different pension funds. If you look at PGGM’s history when it comes to VZ stock, you’ll see that it’s gone hot and cold over the past couple of years.

It held 3.93 million shares of Verizon stock at the end of September 2017. By the end of that year, PGGM pared that position by 64% to 1.4 million shares. It then held steady over the next three quarters until adding 1.3 million shares in the fourth quarter of 2018 and another 1.0 million shares in the first quarter of 2019.

As far as its $20-billion portfolio of U.S. stocks, Verizon is the 23rd-largest position out of 254 stocks, an indication of how confident the fund managers are about VZ stock.

Of course, I don’t expect you to buy its stock solely because a multi-billion-dollar fund owns it. There also have to be compelling reasons why its business will grow over the next three to five years.

And there is.

An Essential Component

InvestorPlace contributor Will Healy recently sung the company’s praises focusing on the 5G opportunity that lies in front of Verizon.

“As 5G becomes an essential component of the economy, Verizon’s strategy to bet primarily on wireless could make VZ stock less risky than its more content-dependent peer, AT&T (NYSE:T),” Healy wrote April 3.

However, it wasn’t what Healy said about 5G that caught my attention, but rather Verizon’s decision to put much less emphasis on its media business than its competitor.

As InvestorPlace contributor Todd Shriber

highlighted recently, Verizon has $110 billion in debt or about 47% of its market cap compared to AT&T which has approximately $170 billion in debt or 76% of its market cap.

I’ve got a list of reasons why I wouldn’t invest in AT&T, but its debt situation is definitely at the top. I generally don’t like to invest in companies whose debt is 50% or more of its market cap.

I also like the fact that Verizon is more of a 5G pure play than AT&T. Together, these two reasons make VZ stock the more logical and conservative investment.

Verizon Isn’t a Buy

The “all-in” 5G strategy is a bold one, but it does have a downside.

Verizon has said it will spend between $17 billion to $18 billion on its business in 2019 including the expansion of its 5G network. That’s on top of $16.7 billion it spent in 2018. That’s a lot of money for a technology that most consumers likely won’t need.

However, because it’s grabbed first-mover advantage on the 5G front, it can’t afford to step off the gas, or it will lose the marketing edge it has on its peers. Meanwhile, companies such as AT&T can take their time rolling out 5G to find the most profitable pathway to national coverage.

MoffattNathanson founder Craig Moffett recently suggested that 5G won’t be available everywhere in the U.S. for at least two years, likely longer, due to the fact there isn’t enough wireless spectrum to support it.

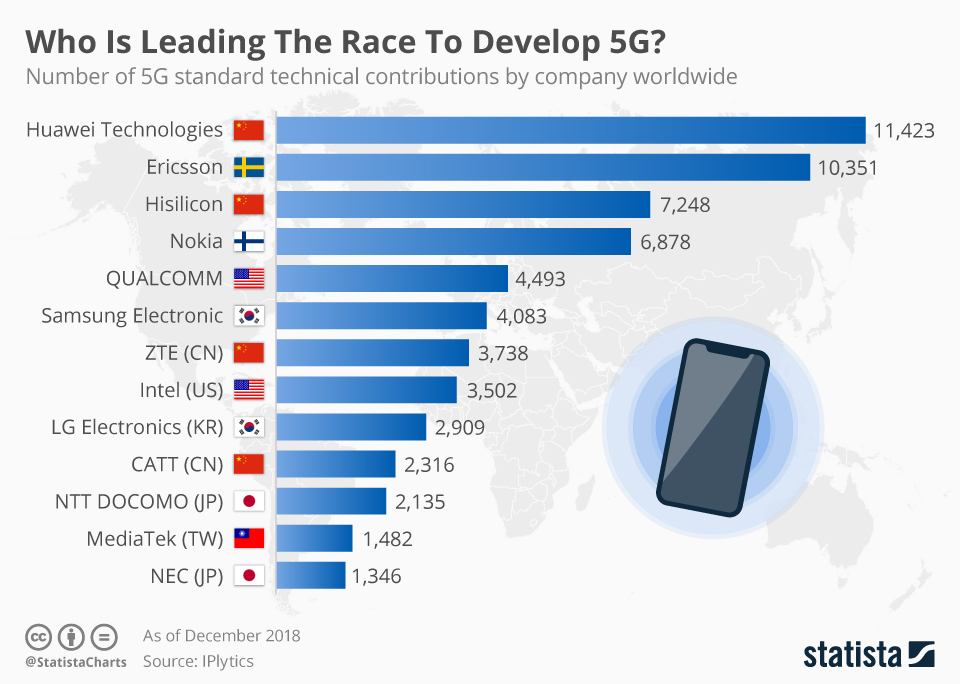

Source: Statista

“There is a zero chance that 5G is a ubiquitous technology by 2021,” Moffett said in an April CNBC interview. “The standards of 5G were set for insanely wide blocks of spectrum. You can’t find insanely wide blocks of spectrum anywhere but these stratospheric high frequencies.”

Which means Verizon could be spending a lot of money for a much smaller return on investment than initially anticipated.

In the near term, 5G is not a guarantee of enormous profits, and that’s something Verizon shareholders should understand if they’re going to hold for the long run.

The Verdict on Verizon Stock

If you’re looking to buy Verizon stock solely because of its 4.1% dividend yield, you might want to look at the AT&T dividend instead, with its 6.51% payout.

However, if you want to own a stock that’s not debt-laden and has a good long-term plan for 5G, VZ stock is a much better buy than T in my opinion.

VZ stock is up 1.5% in 2019. T stock up less than 1%. The iShares U.S. Telecommunications ETF (BATS:IYZ), with Verizon and AT&T among its top four holdings, is up 15.8%.

The fact that one of Europe’s biggest pension fund managers has dramatically increased its Verizon holdings cements that view.

At the time of this writing Will Ashworth did not hold a position in any of the aforementioned securities.