PayPal Holdings (NASDAQ:PYPL) may have established the digital-payments industry, but there’s no denying that its rival, Square (NYSE:SQ) has won the war of publicity since the start of 2018.

There’s a secret that only owners of PayPal stock know, however, or at least realize. That is, after crushing it in 2017 and holding its ground in 2018, PayPal stock price is crushing it again this year.

This may not be the absolute most opportune time to buy PayPal stock if you haven’t done so yet; given the frothiness of PayPal stock price, PYPL stock is ripe for some profit-taking. But, there’s a reason PayPal stock price is still climbing as if PYPL was a new, high-growth company.

Still Chugging Along

If you want a number, it’s 35%. That’s how much PayPal stock price is up since the end of 2018, versus the S&P 500’s 15% advance.

Even more remarkable is that the big gain took shape at a time when few thought it would, or even could. Early last year eBay revealed it would begin featuring PaPal’s Dutch rival, Adyen. In the meantime, Square found a way to facilitate peer-to-peer payments every way except the primary way that PayPal serves consumers and small businesses. PYPL wasn’t (and still isn’t) interested in handling cryptocurrencies at a time when cryptocurrencies were all the rage. As of late-December, the consensus price target on PayPal stock was just under $100 per share.

None of it really mattered, though. As it turns out, PayPal is even better when it’s left alone and allowed to do its own thing without anyone standing over its shoulder.

The numbers tell the tale. PayPal’s revenue surged 13% last year,. and its non-GAAP earnings per share jumped 26%.

After, blasting past the consensus price target in April, PayPal stock closed yesterday at $112.15.

The Outlook of PayPal Stock

This year is expected to be even better for PayPal. Analysts are calling for more than 16% revenue growth in 2019, followed by more than 17% growth next year. Its EPS is expected to reach $2.98 this year and hit $3.51 in 2020.

That leaves little to complain about. The acquisition of Venmo and better cultivation of its Merchant Services arm — which is a stab right at Square — have been worth the expense and effort. In Q4, Merchant Services’ revenue jumped 29% year-over-year. After PayPal works to improve the integration of iZettle, which it acquired last year, the subsidiary should continue to grow by double-digit percentage levels.

The key for PayPal stock has been, according to BTIG analyst Mark Palmer, size that others like Square can’t match.

Palmer also notes that Venmo is nearing profitability, which could prove to be a major catalyst for PayPal stock. ”

“PayPal’s progress toward monetization of Venmo has accelerated,” noted the analyst earlier this month. He adds, “The app had 40 million users at the end of 1Q19 and at that point had an annual revenue run-rate of more than $300 million, a sizeable jump from the annual revenue run-rate for the app of more than $200 million that management had announced in January.”

All told, Palmer now thinks PayPal stock is worth $130 per share.

Not Yet

While the rest of the analyst community isn’t quite as enthused, given the consensus price target of $116, their unwillingness to raise their targets may have more to do with this year’s bullish surge and less to do with a lack of value.

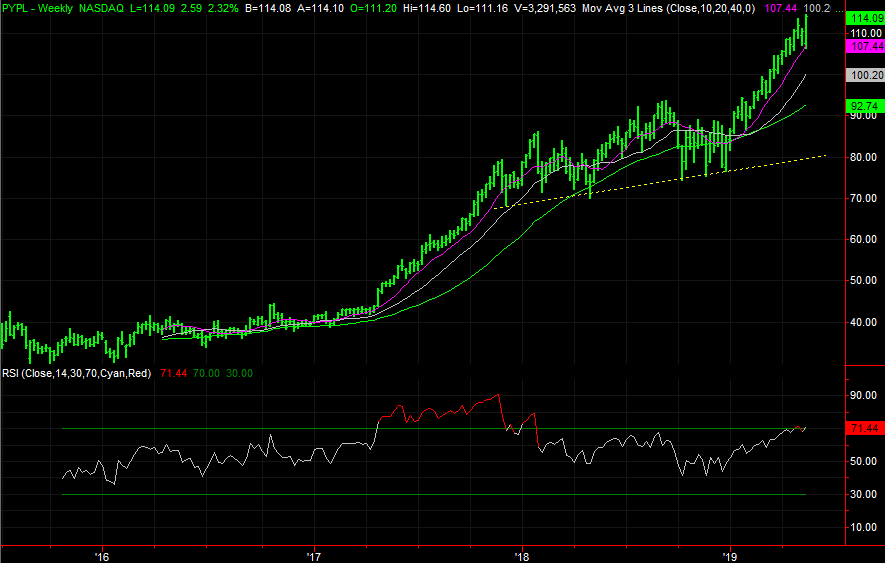

That crowd still has a point. The steep rally, while not unlike 2017’s big move, has pushed PYPL stock to prices that will be difficult to hold onto. This week’s snapback rally into new-record territory is exciting, but also uncomfortably hot.

Click to Enlarge

Where any pullback may finally stop and reverse is difficult to say. There’s a major support level near $80. A selloff of that scope seems unlikely given the company’s outlook, however. More plausibly, a retreat to one of the moving average lines around $100 or $93 will stop any bleeding of PayPal stock.

The toughest part of trading is being patient when waiting to buy stocks, and mustering the willingness to pull that trigger in the midst of a pullback. Don’t shoot for perfect timing, and don’t sweat it if you wade in too early. PYPL is a long-term trade driven by fundamentals that have remained surprisingly solid.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.