Shares of chipmaker Nvidia (NASDAQ:NVDA) started off 2019 on the right foot, rallying from $130 in late 2018 to nearly $200 by April 2019. This jump occurred against the backdrop of improving semiconductor, economic and financial market conditions. But that rally has since short-circuited. Over the past two months, we’ve learned that demand broadly remains weak in the global semi market. Furthermore, NVDA didn’t have a good first quarter, and that the trade war with China may just be beginning.

As investors learned all that, they stopped buying, and started selling. Net net, NVDA stock has dropped from nearly $200 in April to below $150 today.

But in the big picture, the recent downdraft in the Nvidia stock price is a buying opportunity. Long-term growth trends indicate that 2019’s revenue and gross-margin retreat is nothing unusual. Such a retreat is par for the course, and it’s healthy and normal for a semi company like Nvidia. After such a reset, revenues and margins find a bottom, and then resume on their longer-term uptrend.

As such, present weakness in Nvidia’s numbers is ephemeral. That condition translates to NVDA shares too. Once the numbers improve — and they should improve soon — the Nvidia stock price will bounce back towards $200.

Long-Term Trends Are Healthy

If you just looked at Nvidia’s Q1 2020 numbers and nothing else, you would probably walk away very alarmed. In that quarter, Nvidia saw its revenues drop 31% year-over-year, and gross margins declined 610 basis points. Meanwhile, for next quarter, Nvidia projects a near 20% YOY decline in revenues, and a greater than 400 basis point hit on margins.

Those numbers are awful. Why, then, would anyone buy NVDA stock?

Because Nvidia is a semiconductor company, and in the semiconductor world, such volatility is par for the course. For a stretch of several years, the semi market will be defined by big demand and limited supply. This allows for big revenue growth and strong margin expansion for companies like Nvidia.

Then, in order catch up with demand, supply expands. Often that supply growth is too late. It coincides with a demand slowdown. So, then you get a stretch of several quarters where demand slows and supply rises. That pushes revenues and margins.

Right now, we are going through one of those down eras. Semiconductor demand is waning in the face of escalating global economic uncertainty and trade tensions. At the same time, in anticipation of massive secular demand in industries like Internet of Things and artificial intelligence, supply in the semi market has expanded tremendously over the past few years. Net result? Slowing demand on growing supply. That dynamic produces 20%-plus revenue declines and several hundred basis points of margin compression for NVDA.

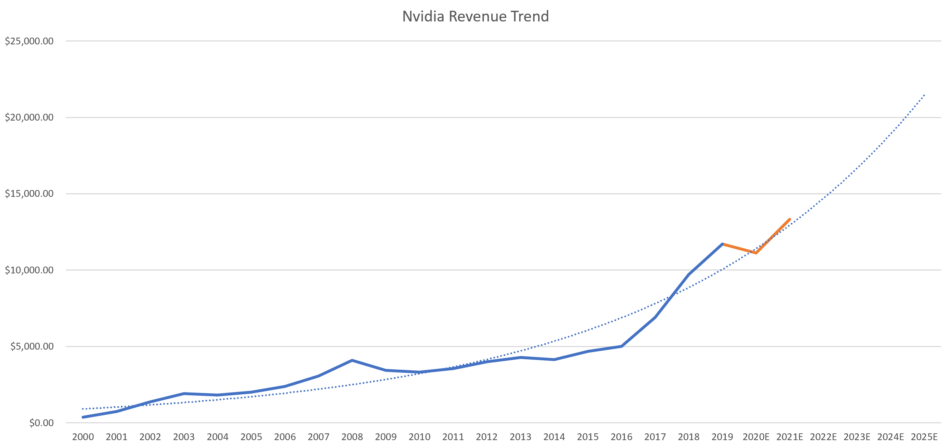

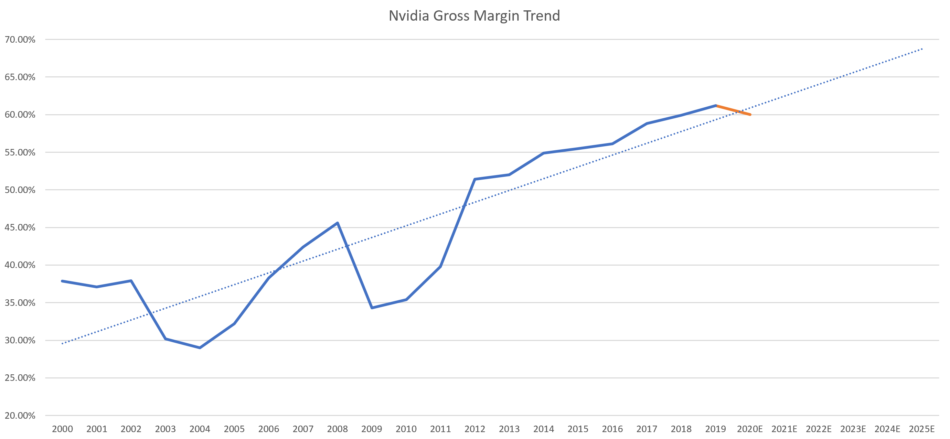

Click to Enlarge But if you look at Nvidia’s long-term revenue and margin trends, this is nothing alarming. Instead, heading into fiscal 2020, both revenues and margins were moving ahead of their trend-lines. Thus, the 2020 reset seems completely normal and 100% healthy in the broader context. Further, these trend-lines support the notion that growth should return robustly in a reset year.

Overall, then, the long-term revenue and margin trends here indicate that there is nothing unusual about 2020 being a reset year, and that growth should resume in 2021.

Nvidia Stock Should Rebound Soon

There are reasons to believe that a bullish reversal in Nvidia stock is just around the corner, and that such a turnaround will push the stock closer to $200.

First, history basically says that while things will improve for Nvidia, they need to improve first before the stock rebounds. Fortunately, we’re already seeing signs of improvement. Revenue declines are expected to be less than 20% this quarter versus a 30%-plus decline last quarter. Gross margins are expected to fall just 400 basis points versus approximately 600 basis points of compression last quarter. Further, full-year revenue growth is pegged down 11%, so the third and fourth quarters should show continued sequential improvement in growth trends.

If things do play out like this — improving revenue and margin trends throughout 2019 — then investors will increasingly believe that the worst is over for Nvidia, and that 2021 will be a big growth year. As that thesis becomes the consensus, Nvidia stock will move higher.

How much higher? Well, the long-term trend-lines here basically imply that Nvidia should grow revenues to over $20 billion by 2025. Further, gross margins should march towards 70%. To be conservative, let’s call it $20 billion even in revenue by 2025 on 65% gross margins. Assuming some opex leverage, that should produce somewhere around $13 in earnings per share.

Based on a historically average 20-times forward-earnings multiple, that implies a 2024 price target for Nvidia stock of $260. Discounted back by 10% per year, that equates to a reasonable 2020 price target of roughly $180.

Bottom Line on NVDA Stock

So far this year, Nvidia stock has produced some massive gains and staggering losses. The next shift will likely be another strong upswing. It increasingly appears that the worst is over for this company, and that growth will come back into the picture by the end of this year. That gives the runway for NVDA to start acting like a winner again.

As of this writing, Luke Lango did not hold a position in any of the aforementioned securities.