Facebook (NASDAQ:FB) is a free cash flow (FCF) machine, pumping out billions in FCF each quarter. And I think Facebook stock will benefit from its improving FCF margins, advertising pricing and Average Revenue Per User (ARPU).

Free cash flow is the purest form of profit that a company generates. In the last quarter, FB made its highest level of FCF ever, topping $5.6 billion.

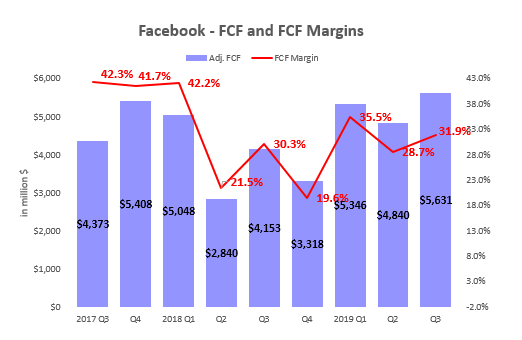

In addition, 32% of every revenue dollar flows down to FCF. This margin is not as high as last year, but it is improving. You can see this in the chart below which I put together for InvestorPlace readers.

Higher FCF Margins

Click to Enlarge

This chart shows that FB made of $5.6 billion in FCF in the third quarter, its highest ever quarterly level of FCF. In addition, you can see that the FCF margins have risen dramatically since last Q4, where they were at 19%.

Part of the reason for this is FB’s pricing and ARPU has been increasing. Facebook’s ARPU has risen from $6.01 in Q3 2018 to $7.15 in Q3 2019 for every worldwide monthly user.

Essentially that means its pricing for ads online has improved. So with the combination of more users and higher ARPU, the result is that revenue and FCF increased significantly over the last year.

In addition, FB has kept its costs under control. Last year its operating margins were 42%. This past quarter they were 41%. As a result, with higher revenue and ARPU, FB’s FCF margins have been soaring.

Facebook’s Guidance Implies Higher FCF

During Facebook’s

Q3 conference call, Facebook said that its Q4 revenue growth rate would “decelerate by a mid to high single-digit percentage compared to our Q3 rate.” Here is what that means. Since Q3 revenue increased by 28% (31% on a constant currency basis), then estimated Q4 growth will be 28% less 7% or 8%.

Let’s call it 8%. So Y/Y growth in sales will be 20%. That means that Facebook’s Q4 revenue will be $16.9 billion times 120%, or $20.3 billion. Now, using this past quarter’s FCF margin, we can estimate that free cash flow will be $6.48 billion.

That will be another record quarterly for this metric. Why is this important? We can use it to estimate the Facebook stock market value.

Estimating Facebook Stock Value Based on its FCF and Margin

Facebook stock has traded at an FCF yield of about 3.75% over the past two years. This means that its market value has been 27 times its run-rate FCF generated for the quarter.

So using the estimate we derived for Q4 FCF, $6.48 billion, FB’s run-rate FCF will be $25.9 billion. So the Facebook stock market value implied the 27 historical multiple is $691 billion. Since FB has 2.851 billion shares outstanding, the value per share is $242.22 per share.

This represents an upside of 19.9% for Facebook stock. That represents a good return for Facebook shareholders and new investors.

What Should Investors Do?

This upside does not include any increase in Facebook’s user base or ARPU, nor any improvement in FCF margins over the next year. All of these metrics have been improving incrementally in the past few quarters.

This implies that Facebook stock could rise even further over the next year. So expect a higher return than 20%.

In addition, Facebook has been buying back its shares over the past two years. It had managed to lower its share count by 1.7% in the past two years. This buyback effort also includes any net new shares it has issued to its employees. That means that Facebook has been using its free cash flow to return value to its shareholders.

I would expect that the share count will continue to fall, perhaps even more aggressively. Facebook did not discuss this in its latest earnings call. But it seems clear that the buybacks will continue.

For example, In the last 12 months, Facebook has used 45% of its FCF to buy back its own shares. If that were to continue over the next 12 months, up to $10 billion in shares could be bought back. That represents 1.8% of Facebook’s stock market value.

So it’s safe to say that between the higher FCF and increased share buybacks, Facebook stock will likely be a good investment over the next year.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide which you can review here. The Guide focuses on high total yield value stocks. Subscribers a two-week free trial.