Recently Plug Power (NASDAQ:PLUG) completed an offering of 40 million shares which will raise $104.7 million after the offering expenses. The prospectus also says that the underwriters for Plug Power stock can buy six million more shares at the $2.75 offering price. That would bring in another $16.4 million, according to the prospectus.

But here’s the thing: The final prospectus is full of dire warnings about the company. If you want to know what could go wrong with a potential investment, always read the “Risk” section of their annual 10-K or prospectus. The prospectus filed on Dec. 6, 2019, has the latest risks.

Let’s take a look at some of these, which seem pretty dire.

Risks of Investing in PLUG — According to the Company

The very first risk the company wants you to know is that they have “incurred losses and anticipate continuing to incur losses.” The prospectus then states that the company has not achieved profitability in any quarter since its formation. In fact, the company is bluntly honest about its failures:

We incurred net losses attributable to common stockholders of $73.8 million for the nine months ended September 30, 2019 and $78.2 million, $130.2 million and $57.6 million for the years ended December 31, 2018, 2017, and 2016, respectively, and had an accumulated deficit of $1.3 billion at September 30, 2019. We anticipate that we will continue to incur losses until we can produce and sell our products on a large-scale and cost-effective basis.

The prospectus then goes on to point out all the hurdles that it must cross in order to achieve profitability. It states:

If we are unable to successfully take these steps, we may never operate profitably, and, even if we do achieve profitability, we may be unable to sustain or increase our profitability in the future.

More Hurdles that Plug Power Stock Has to Cross

Now, as if that dire warning is not enough, the company goes further. It points out that there is an issue with the long-term viability of its alternative energy products in the marketplace:

… if we are unable to successfully develop future products that are competitive with competing technologies in terms of price, reliability and longevity, customers may not buy our products. The profitability of our products depends largely on material and manufacturing costs and the market price of hydrogen. We cannot guarantee that we will be able to lower these costs to the levels to assure market acceptance in conjunction with other critical customer criteria in performance and reliability.

Another major risk is that PLUG cannot guarantee that it will need more financing. This could be either from a debt source or more dilution from equity financing.

The prospectus states this in a strange way. Most offering memos state something like the proceeds will allow the company to fund itself for the next 12 months, even if it is losing money.

But Plug Power’s prospectus gives no such assurances. It does not state if the money raised will last more than one year. That implies there is little faith at the senior exec level that PLUG will pull out of losses anytime soon.

Honesty Is the Best Policy

Most people think the prospectus language is just boilerplate legal jargon, but it isn’t. The company is required to be deathly honest about its downfalls.

In this case, Plug Power goes on to name 13 additional risks that investors should consider before buying Plug Power stock.

Here is a statement they made that I found kind of funny:

Our management might not apply our net proceeds in ways that ultimately increase the value of your investment …Our failure to apply these funds effectively could have a material adverse effect on our business, delay the development of our products and cause the price of our common stock to decline.

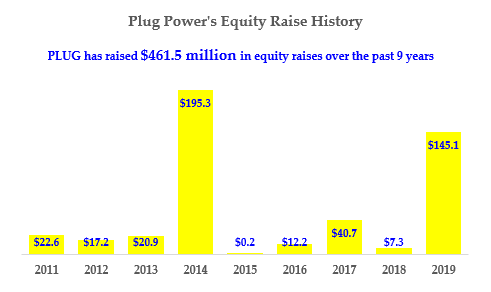

History of PLUG Stock Capital Raises

This is funny since Plug Power has raised over $461 million over the past nine years in equity capital. This includes the amount raised in the most recent offering.

Click to Enlarge

The table at the right shows that every five years or so Plug Power needs to juice up again with another major capital raise. That includes the most recent capital raise.

What does PLUG have to show for all these capital raises? Nothing but losses, by its own admission. And remember, that is over nine years, not two or three or even five years.

And Plug Power stock has gone nowhere over the past nine years since 2011, despite all those capital raises.

So, it is funny that Plug Power finds the need to warn investors. They know they have to be honest. Management might not apply the proceeds of the capital in a way that raises the investors’ investment. That is an understatement.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide which you can review here. The Guide focuses on high total yield value stocks, which includes both dividend and buyback yields. In addition, subscribers a two-week free trial.