Warren Buffett’s Berkshire Hathway (NYSE:BRK.A) has increased its stake in Amazon (NASDAQ:AMZN) while also having close to a $50 billion stake in Apple (NASDAQ:AAPL). Berkshire’s stake in Amazon is now close to $1 billion.

Apple’s market cap is over $1 trillion, while Amazon’s market cap is almost $900 billion. However, both of these companies have completely divergent metrics when we look at P/E ratio, EPS growth, and revenue growth.

Apple stock has shown 69% year-to-date growth in stock price while Amazon stock has shown only 20% growth. Amazon’s price growth has been lower than the S&P 500’s, which has risen by 28% in 2019. However, an in-depth look into different metrics shows the upside for AMZN stock compared to AAPL stock.

Advantage Within Apple and Amazon Stock

The biggest advantage of owning Apple stock is the massive scale of buybacks. This ensures that Apple can keep on reducing the outstanding stock which helps to improve the EPS growth.

Over the last five years, Apple’s revenue has increased by close to 41% with a similar increase in net income. However, due to its massive buyback program, the EPS has increased by 82.5% during this time. Apple has reduced its outstanding stock by one-fifth during this period. Investors looking to make a long-term commitment should look at the buyback rate of Apple closely.

In the recent quarter, Apple’s net cash position was $102 billion. This is down from $130 billion at the end of 2018. Hence, Apple has reduced $28 billion from its net cash position despite having large cash flows. If this rate of stock purchases continues, we should expect a net cash-neutral position for AAPL by the end of 2020. Due to the massive increase in video streaming budget and expenses on other services and products, we could see a cash-neutral position sooner.

Once Apple reaches a cash-neutral level, it will have to significantly reduce its buyback pace. This will obviously have a negative impact on EPS growth and the valuation multiple of AAPL stock. Investors making a long-term bet on Apple stock should look at this emerging trend.

Amazon does not spend on buybacks or dividends. However, faster revenue growth and margin expansion have helped in substantial improvement of EPS in the last few quarters.

In the last three years, Amazon has increased its EPS and net income by 350%. This improvement can continue as the revenue share of higher-margin businesses, like AWS and advertising, increases within AMZN. This is a big advantage for long-term investors who can see good bullish sentiment in Amazon stock due to rapidly increasing EPS.

AAPL and AMZN Growth Profile

Apple and Amazon have completely different growth profiles. Apple’s core iPhone revenue has stagnated in the U.S., while it is falling in Greater China and Europe. The wearables growth is higher, but the revenue share of this segment is very small. Apple is trying to build new services like video streaming, gaming and news platforms, but all these segments have a lower margin compared to the App Store. This can cause a dip in net income for the company in the near-term.

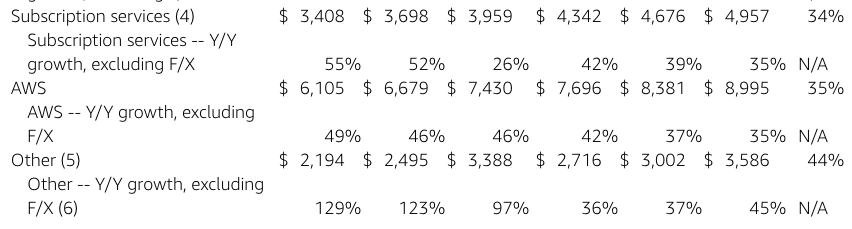

On the other hand, Amazon’s growth has also slowed a bit in the last few quarters, but it was still a respectable 25% in the last quarter. At the same time, the higher-margin segments like AWS, advertising and even subscription revenues have continued to show faster growth in 30% to 40% range.

Source: Amazon Filings

Hence, the main culprit for a slowdown in overall growth rate for Amazon is its low-margin online stores segment. AWS, advertising and subscription revenues now make up about 25% of the total revenue base of Amazon. As the revenue share of these high margin segments increases, we should see better profit and revenue growth from the company.

Valuation

This is where most analysts differ about Apple and Amazon. Many bullish AAPL analysts see it as a value buy due to its P/E ratio of 21-22, while bullish analysts for AMZN point to rapid EPS growth, which will help in bringing down the P/E ratio for the stock which is currently close to 80.

Despite buybacks of close to $80 billion over the last year, Apple’s EPS has fallen by 2% while Amazon’s EPS has increased by 12%. Amazon’s future EPS growth is also much more promising. The company can show continuous improvement in operating margin as advertising and AWS revenues increase.

Due to these reasons, I believe Amazon stock is a better bet for long-term investors compared to Apple stock. AMZN has not started any program for returning excess capital to investors through buybacks or dividends. We could see this happen once the company maximizes its investments in growth segments. This should also provide additional upside to Amazon stock. On the other hand, Apple would need to curb its buybacks and reduce the growth of dividends as it reaches a cash-neutral position.

Investor Takeaway on AAPL Stock and AMZN Stock

Buffett has invested in both Apple stock and Amazon stock. There are strong reasons for choosing either of these two giants for long-term investments. However, Amazon wins the comparison with Apple when we look at revenue growth runway, EPS growth, and improvement in margins. Apple is also at a disadvantage from long-term investment potential because it will soon lose the capacity of making huge buybacks as the company reaches a cash-neutral position.

Amazon’s valuation multiple is currently higher than Apple, but rapid margin and EPS growth should bring down the P/E ratio to more attractive levels. Rapid improvement in revenue and profits has always been cheered by Wall Street which should help in continuing a bullish sentiment towards Amazon stock.

As of this writing, Rohit Chhatwal did not hold a position in any of the aforementioned securities.