With Aphria (NYSE:APHA) releasing a disappointing earnings result for its fiscal second quarter, most investors have probably either thrown in the towel or are close to it. Unsurprisingly, Aphria stock tumbled on the news, dropping over 8% against the prior day’s session. But in the midst of this setback, I’m seeing a risky but not unreasonable contrarian opportunity.

Admittedly, I’m sure embattled stakeholders, prospective buyers and casual observers are tired of this sentiment. I’m tired of giving it. Despite the transformative nature of the cannabis industry – we are, after all, talking about a black market becoming a legal, taxable one – Aphria stock hasn’t lived up to expectations.

Of course, that’s not a knock against the underlying company. From superstars like Cronos Group (NASDAQ:CRON) and Canopy Growth (NYSE:CGC) down to the minor-league players, cannabis was supposed to deliver some green. Instead, the sector has printed almost nothing but red ink.

On the surface, Aphria did nothing in its fiscal Q2 to shift the narrative positively. Heading into the report, industry believers hoped that “Cannabis 2.0,” or the initiative to bring derivative products like vapes, edibles and beverages into the Canadian market, would bolster Aphria stock. Instead, management produced metrics that again frustrated Wall Street.

Citing difficulties in Aphria’s domestic market, the leadership team cut its fiscal 2020 revenue target to a range between 575 million CAD to 625 million CAD. Previously, executives estimated top-line sales to come in between 650 million CAD to 700 million CAD.

To be fair, the rough going in Canada’s marijuana retail market impacts everyone. But with Aphria not demonstrating the greatest fiscal stability, investors are losing patience with its shares.

Even the Math Shows Canada’s Cannabis Market Is Wacky

I’m not going to sugarcoat it. For the people who are done with Aphria stock – or similar investment – I don’t blame them. Unfortunately, legalization has been a harsh lesson in the juxtaposition between theory and reality.

Yet I’m also cautiously optimistic. While the marijuana firm’s Q2 report was disastrous, I was interested in why it was so. Specifically, management called out the “slower than expected retail location rollout in Ontario.” To which I say, no flippin’ spit (or something like that).

Earlier this month, I criticized how the Canadian government rolled out their broader cannabis initiative. Despite the fact that robust demand continued to grow across the nation’s provinces, it failed to deliver retail rationality. A long story short, the distribution of cannabis licenses demonstrated no discernible logic. Instead, store openings occurred rather haphazardly.

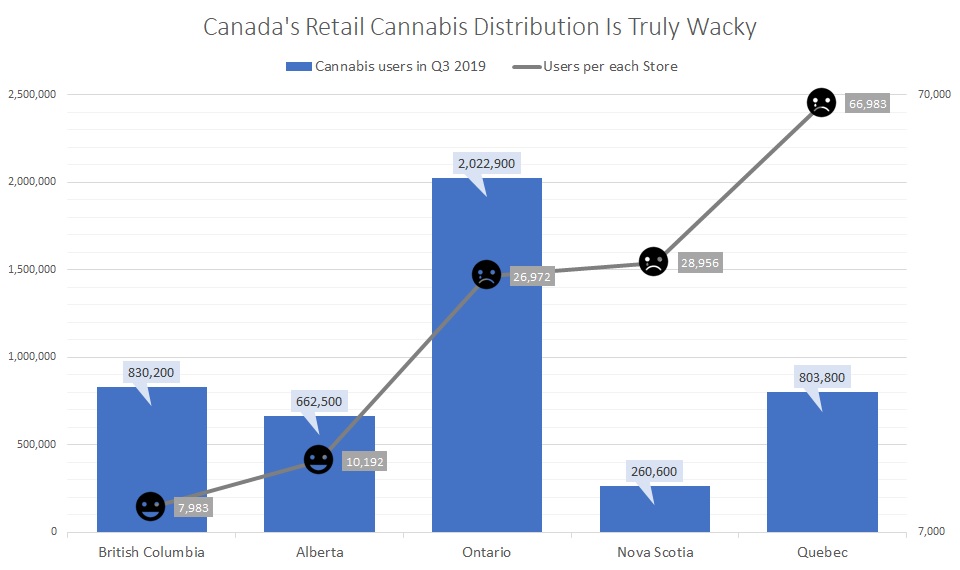

This agonizingly frustrating irrationality is most evident with Ontario, the province that Aphria called out. According to Canadian government statistics, Ontario had over two million adult cannabis users in calendar Q3 2019. That represents the biggest user base in the country. Yet it only had 75 stores to service them all, or nearly 27,000 users per each store.

Click to Enlarge

Then you have a province like Quebec. At nearly 804,000 cannabis users, it too is a respectably large market. Yet out of the 15 approved stores, only 12 were open in Q3 2019. That leaves each store to serve nearly 67,000 people.

Even more maddening, you have Alberta with 662,500 cannabis users. However, the province has 65 stores, leaving each one to serve only 10,192 users.

When I calculated the correlation between cannabis users and users per each store, I got a correlation coefficient of 0.15%. In other words, government stupidity is stymieing an otherwise viable retail market.

Alphria Stock Is Still a High-risk Play

Because high-level ineptitude forced Aphria and its peers into an impossible circumstance, I’m willing to cut the company some slack. Among contrarian plays, this is one of the most compelling because not too many folks appreciate the supply chain absurdity.

However, Aphria stock is also among the riskiest names to go against the grain. I don’t want to give the impression that government incompetence is the only headwind to hurt the sector. Plus, we don’t know when (or if) Canada will get their act together. Finally, the loss of patience on the Street makes any cannabis stock a dangerous endeavor.

That said, I’m ultimately intrigued with Aphria. Given the currently illogical market that we have in Canada, it helps to explain prior sector headwinds. For instance, illicit marijuana sales continued to grow despite legalization. Now, evidence suggests that this dynamic was due to the lack of practical accessibility across the provinces.

But my bet is that this will change. It has to. Even though Canada fumbled the ball, they can still pick it up and run with it. When it does, the narrative for the cannabis industry will finally shift positively.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities. However, he is considering a position in Aphria stock over the next 48 hours.