Has Nvidia (NASDAQ:NVDA) been on fire or what? While the stock market has posted a very respectable rebound over the past few weeks, NVDA stock has gone bonkers.

Its shares have more than doubled from their lows, outpacing the S&P 500 and most tech stocks. Simply put, Nvidia was a steal below $200 a share, and now many investors are left wondering what to do with the stock near $300.

Let’s highlight three reasons why NVDA stock is a buy once the shares retreat meaningfully.

Business Is Booming for Nvidia

Nvidia’s businesses are uniquely positioned for non-cyclical growth. The company operates several main units, including gaming, data center, edge computing, automotive and professional visualization. First, these technologies are the backbone of future technology. Second, many of them are not being disrupted by the novel coronavirus, which is dealing a swift blow to many industries.

Admittedly, virtually all automakers, including Ford (NYSE:F) and Mercedes, are hitting the brakes on costs. That means their R&D spending on things like autonomous driving are likely to be on pause for at least a few quarters while they attempt to recover from the impact of the coronavirus.

However, their autonomous driving ambitions will not disappear overnight due to a short-term disruption in the global economy. So although Nvidia’s autonomous driving business is likely to suffer in the short-term, it still has tremendous long-term potential.

The company’s other units are not as likely to be impacted by the coronavirus and the recession. All the additional data being generated by those working at home and the increased strain on the internet will boost demand for Nvidia’s data center and edge computing products. Its gaming unit is likely to remain quite strong as well, as consumers turn to at-home entertainment options while they’re under lockdown.

Click to Enlarge

Estimates for Nvidia remain high. Analysts, on average, expect its revenue to jump 19% this year to $12.98 billion. The mean earnings estimates of $7.57 per share is actually up from $7.25 90 days ago, although it’s down from $7.80 a month ago.

The revisions came after the company’s better-than-expected fourth-quarter earnings report in February. That report helped propel NVDA stock over $300 to new all-time highs. Despite the short-lived party, the results showed that Nvidia “was back” and that bulls were in control.

Closing the Mellanox Deal

The current average earnings estimate represents 30% year-over-year growth. If the company’s results are in-line with the mean estimate, it will have delivered 19% revenue growth and 30% earnings growth in 2020. Those are very solid numbers.

That’s particularly true since many other companies have delivered flat or negative growth. However, there’s another catalyst that could make Nvidia even more attractive, and that’s Mellanox (NASDAQ:MLNX).

In March 2019, Mellanox agreed to be acquired by Nvidia in a $6.9 billion deal. NVDA stock rallied on the news because it was not difficult to figure out the advantages of the deal for Nvidia.

First, Nvidia didn’t overpay for Mellanox, which is the one big concern about acquisitions. A deal can make sense and the company that’s being bought can be great, but what price is the acquirer paying for the asset?

After agreeing to a fair price, Nvidia announced that the Mellanox acquisition would immediately increase its earnings, margins and free cash flow. In mid-April, Chinese regulators agreed to approve the deal. The addition of Mellanox will be one more positive development for Nvidia.

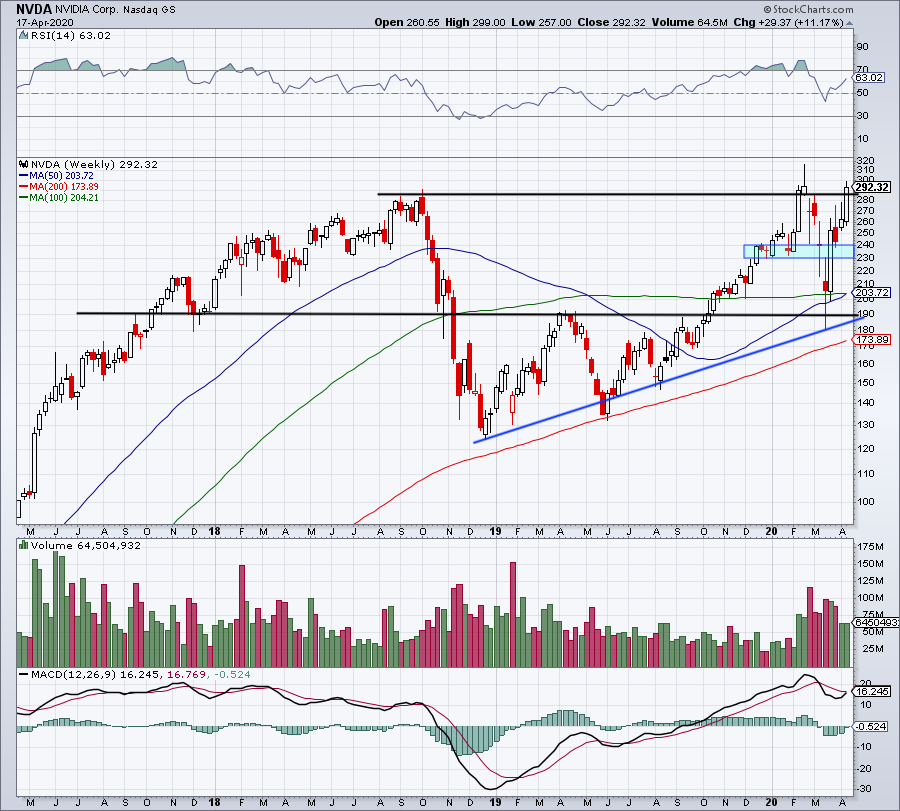

Nvidia Has Great Technicals

Click to Enlarge

As I highlighted at the beginning of the column, NVDA stock has been very resilient over the past few weeks. Its shares proved to be a steal near $200 and with the stock’s outperformance, it’s not hard to see why the shares should be bought on any weakness.

I love Nvidia’s long-term story and the way its growth is trouncing most other stocks. However, I am not willing to bid near $300 per share for this stock when it was at $180 just a few weeks ago and as it hovers near its all-time highs.

The stock’s relative strength both to its peers like AMD (NASDAQ:AMD) and the stock market is very attractive. Still, I would prefer to wait for a pullback before allocating more capital to this long-term winner.

On a dip, I’m first looking at the $240 area. That has been a consolidation area over the past few quarters and could serve as support on a dip. If the shares break below $230, they may sink to their 50-week and 100-week moving averages. That would give investors a possible opportunity to begin acquiring the stock.

Below that, the $190 level stands out, as does the 200-week moving average. A drop to those levels would give investors excellent buy-the-dip opportunities.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long NVDA.