People are watching more TV while they are in stuck at home. This is good for media stocks since the companies should be making more money. Moreover, a number of these stocks are very cheap with huge upside potential.

Comscore (NASDAQ:SCOR), a media analytics company, says TV viewing is “surging” — up 33% year-over-year — in its latest comparison. Additionally, it also says that video-on-demand transactions are up 30% year-over-year.

This is good news in the long run for content producers and TV station owners. Also, a number of these stocks are selling for very cheap prices in terms of their long-term valuations.

The following are six cheap media stocks that have forward price-to-earnings ratios below 10 times. In addition, half of them are dividend stocks with nice yields. That said, the media stocks have huge upside potential and are worth looking into are:

- AMC Networks (NASDAQ:AMCX)

- ViacomCBS (NASDAQ:VIAC, NASDAQ:VIACA)

- Discovery Inc (NASDAQ:DISCA, NASDAQ:DISCK)

- Gray Television (NYSE:GTN)

- E.W. Scripps (NASDAQ:SSP)

- Nexstar Media Group (NASDAQ:NXST)

With all of that in mind, let’s dive into the media stocks.

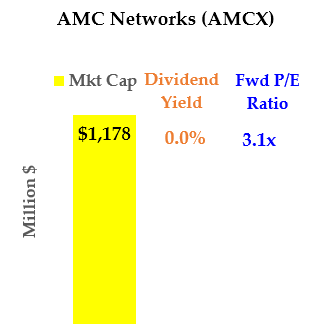

Cheap Media Stocks: AMC Networks (AMCX)

Click to Enlarge

AMC Networks produces TV content for the following brand channels: AMC, WE tv, BBC America, IFC and SundanceTV. The company is known for its The Walking Dead franchise and also has several up and coming programs, like Killing Eve and Into the Badlands. By the way, don’t confuse this stock with AMC Entertainment (NYSE:AMC) — the movie chain company.

AMC Networks makes money from distribution fees (68% of revenue) from its partners like cable companies, TV stations and phone companies. The remaining money is from advertising. The company is also trying to move into subscription video on demand (SVOD) and advertising video on demand (AVOD) from on-demand subscription services. Right now, AMC Networks has no programming costs during the novel coronavirus pandemic.

But here is the thing. AMC Networks is extremely profitable. For example, last year the company made an adjusted operating income of $904 million on revenue of $2.37 billion. That is a fantastic operating margin of 38%, and many businesses would love to have that.

Also, keep in mind its market cap is just $1.18 billion or so. That puts AMCX stock on a forward earnings profile of just 3 times or so. AMC Networks clearly has very high earnings power, and it has withdrawn its earnings outlook. But at some point in the future, it will have higher earnings like in 2019. And in turn, this makes the stock very cheap.

AMCX is off almost $35 from its 52-week high of $59.62, or almost 58%. At some point, I suspect the stock will trade at least 50 to 100% higher to a forward P/E ratio of twice its present valuation.

AMC Networks comes out with its first-quarter earnings on May 5. And this may offer an opportunity for value investors to begin picking away at AMCX stock.

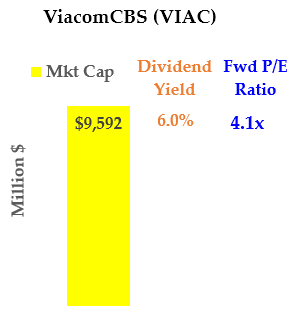

ViacomCBS (VIAC, VIACA)

Click to Enlarge

Viacom and CBS merged on Dec. 4, so the company has still not had one full year together. But on paper, it is selling for a very cheap multiple of just four times. Moreover, VIAC stock sports an attractive dividend yield of 5.5%.

Viacom is off more than 70% since its 52-week high and over 62% since the beginning of 2020. But here is the value proposition: analysts expect earnings per share this year of at least $3.75, even though the stock is at just $19 per share. That put is it on a forward price-to-earnings ratio of just over three times. This is incredibly cheap, and it assumes almost the worst for the company.

For example,

Barron’s ran a negative story on VIAC stock on March 26 — right after a recent bottom — highlighting why analysts don’t like ViacomCBS. They don’t like the merger, the company’s programming, its out-of-step distribution model and its major shareholder — National Amusements — a movie theater company.

However, who cares? If you are a value investor, you want to know the company’s earnings power. Last year, ViacomCBS made $5.00 per share on an adjusted diluted basis, and in 2018 it made $5.87. This shows that the combined company has significantly higher earnings power than the $3.77 expected this year.

ViacomCBS will report its Q1 earnings on May 7, so look for an opportunity to get in this cheap media stock if it falls out-of-bed again.

Discovery (DISCA, DISCK)

Click to Enlarge

Discovery is another cheap media stock which makes money from both distribution fees and advertising. However, DISCA is off only 24% since the beginning of 2020. This is much better than other media stocks.

Moreover, the stock trades for just 7.1 times its forward earnings. This is very cheap for a company with roughly a $10 billion market cap. In the long run this valuation really just does not make any sense.

For one, Discovery is a powerhouse of programming assets. Its channel line up includes the following: Discovery Channel, HGTV, Food Network, TLC, Investigation Discovery, Travel Channel, Motor Trend, Animal Planet, and Science Channel, as well as OWN (Oprah Winfrey Network).

Second, its earnings power is impressive. Last year, Discovery generated more than $3.1 billion in free cash flow. At $10.5 billion in market cap, the stock trades for just 3.4 times its recent annual FCF. This shows that the company has tremendous earnings power.

The bottom line is that people love to watch Discovery’s shows, and this translates into very high earnings power for the company.

Discovery comes out with its Q1 earnings on May 6. That said, look for a chance to buy in at a cheap price with this member of the media stocks.

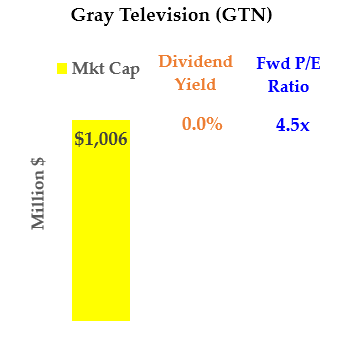

Gray Television (GTN)

Click to Enlarge

Gray Television owns and operates TV stations in 93 markets in the U.S. with all the four broadcast networks, as well as The CW. Moreover, GTN is very cheap at 4.5 times earnings.

If you look at its national footprint, most of its stations are based in the midwest and southeast. In fact, Gray TV is based on Atlanta. They reach approximately 24% of US television households.

The point is that this company makes most of its revenue from advertising from a good cross-section of U.S. businesses. In a way, it represents Middle American business.

Gray TV has significant earnings power. Last year it generated $2.1 billion in revenue and $275 million in free cash flow. So you can see that its present valuation of just $1 billion markets the stock very cheap. Moreover, this year the company expects to see a significant pickup in advertising revenue due to political ads.

Overall, GTN stock is off nearly 50% from its 52-week peak. That said, look for a chance to move closer to its previous valuation.

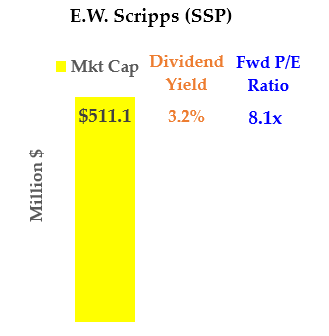

E.W. Scripps (SSP)

Click to Enlarge

E.W. Scripps is a large independent TV station owner just like Gray Television. It owns 60 stations in 42 markets that reach about 31% of U.S. television households. But, again, SSP stock is just too cheap. It trades for just 3.07 times earnings. Moreover, the stock has an attractive 2.9% dividend yield.

The company is very similar to Gray TV. For example, it has affiliations with the four major broadcast networks — as well as The CW. Its advertising revenue represents Middle America business, just like Gray Television.

But Scripps’ market value is half that of GTN stock, at nearly $510 million. Even though its revenue was 62% of Gray Television’s, it produced negative free cash flow. That is probably why its market cap is only 50% of GTN stock.

Nevertheless, this is a play on advertising business returning once the pandemic restrictions are lifted. In addition, the political season would help produce higher earnings and cash flow for the company. This is important as the company is the fourth-largest broadcast TV owner in the U.S.

Scripps will report its earnings for Q1 2020 on May 8, so look for the company to show the way forward through this difficult period. Value investors will also look for an opportunity to pick up the stock cheaply over the next several months.

Nexstar Media Group (NXST)

Click to Enlarge

Nexstar is the largest TV station owner in the U.S. It owns 197 stations in 115 markets or about 64% of U.S households. This $2.7 billion market value stock is very cheap at just 4.6 times prospective 2020 earnings. It also has an attractive 3.3% dividend yield.

Nexstar has been on an acquisition binge. In fact, it bought Tribune Media Company in November 2019. That cost the company $7.19 billion in cash ($4.1 billion) and NXST stock. But it was able to selloff over $2.72 billion in other TV station assets to pay for it.

The problem now, though, is the market cap for NXST stock is only $2.7 billion. So, the company’s timing was not very good. But, of course, who could have known there would be a global pandemic in late 2019?

Going forward, I suspect the market will begin to warm up to NXST stock. In a way, it represents the resurgence of small American businesses as the effects of the pandemic and local restrictions ease.

In other words, as companies start to revive their businesses, they will start to advertise for their goods and services. That will feed directly into Nexstar’s earnings.

Nexstar will report its Q1 earnings on May 6. At that point, look for an opportunity to pick up the stock on the cheap.

Mark Hake runs the Total Yield Value Guide which you can review here. The Guide focuses on high total yield value stocks. Subscribers receive a two-week free trial. As of this writing, he did not hold a position in any of the aforementioned securities.