Prior to the novel coronavirus-fueled downturn turning really ugly, many analysts argued that the big banks, such as Bank of America (NYSE:BAC), Citigroup (NYSE:C) and JPMorgan Chase (NYSE:JPM) represented relatively safe places to park your money. The poster child of corporate excess and greed during the Great Recession, the industry allegedly repented of their ways. Armed with a much more stable balance sheet, investments like BAC stock should theoretically perform well.

However, I have my doubts.

Mainly, a stable balance sheet in this case means that the big banks no longer carry the kind of toxic assets on their books that once threatened to undermine the global financial system. Essentially, these too big to fail institutions learned their lesson. And now, we’re supposed to trust BAC stock and its ilk?

Before I get into my criticism of Bank of America – and this applies to many other big banks – let’s briefly examine the events leading up to the Great Recession. For that, I’m going to rely heavily on The Balance contributor Kimberly Amadeo and her expert summary.

Financial deregulation allowed banks to access derivative financial instruments for quick and easy profits. This involved a five-spoke wheel consisting of: a mortgage-issuing bank, a hedge fund to package mortgages into securities, investors that bought those securities, insurance companies that insured against the risks associated with buying mortgage-backed securities, and finally, a homebuyer.

Through every turn of this ridiculous circus, everybody got a cut or a benefit. But when greedy banks sold too many mortgages to subprime borrowers, the house of cards fell.

In retrospect, BAC stock is lucky that it’s still trading. But that luck might end.

Misguided Bailouts Threaten Both BAC Stock and the Nation

By now, you know the story. With the country’s top financial institutions in tatters, the federal government stepped in to stop the hemorrhaging. In theory, by saving the big firms, you end up saving jobs and vital infrastructure. But what it really did was give a pass to corporate malfeasance and abandon most of working America.

Right before the coronavirus, President Donald Trump boasted about creating the greatest economy ever. That might have been on paper. But in reality, the wealth gap between the top 10% of Americans and everybody else widened to the extreme.

Under this scenario, it doesn’t really matter what lessons BofA or any of the previous bad actors learned. If the platform in which they operate is now toxic, strength in the balance sheet is a moot point.

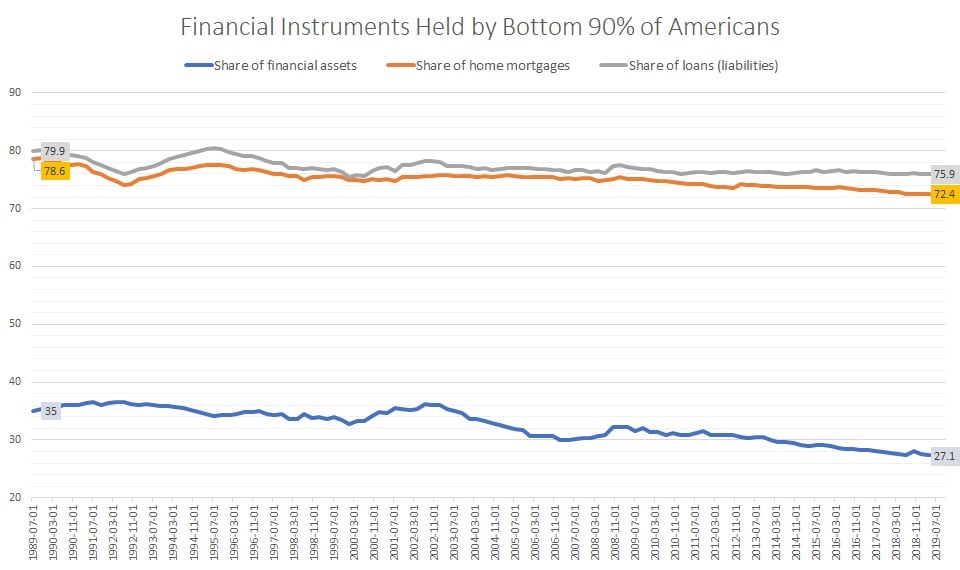

Specifically, the bottom 90% of Americans have for decades carried a disproportionate amount of the nation’s liabilities. In the fourth quarter of 2019, everyone not among the top ten wealth percentiles carried nearly 76% of loans (liabilities). Additionally, they held 72.4% of all home mortgages. These statistics have remained largely stable since at least Q4 1989.

Click to Enlarge

On the other hand, in Q4 2019, the bottom 90% held only 27.1% of the financial assets in this country. Moreover, this is a sizable drop from 35% in Q4 1989.

If that wasn’t bad enough, consider who the coronavirus has impacted the most. Out of the 20.5 million jobs lost in April, most were low-skilled, entry-level positions. For banks to survive this time around, they would need to rely on an American workforce that carries most of the liabilities, the least of the assets, and the biggest wounds of the crisis.

Sure, BAC stock is no longer toxic. But its consumer base is dying.

The Government Needs to Help the People

I applaud Trump and Congress in pushing through the coronavirus relief bill. But it has a severe weakness – it’s simply not enough.

In order to save this country, and by logical deduction BAC stock, the federal government needs to open the monetary spigot to the exclusive benefit of the American people and small businesses. By allowing any further relief to big corporations, the government would only exacerbate this nation’s desperately imbalanced wealth gap.

Honestly, it’s we the people who are too big to fail. Without the millions of anonymous worker bees plying away at their trade, none of the extravagant wealth that only a very small minority get to enjoy would be possible. It’s time for those who have been blessed so exponentially to step up.

As far as banks, bailing out the American people is really the only hope. When only 10% of the country have the good stuff (assets) and the rest have little to show for their work but the liabilities, something will break. That could be our economic viability unless our political elites take this stark reality to heart.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.