Amid the wild extremes in the markets caused by the novel coronavirus, publicly traded credit card companies like Mastercard (NYSE:MA) and Visa (NYSE:V) present a conundrum. On one hand, their underlying products work perfectly with digital and touchless platforms, making them extremely relevant today. But on the flip side, consumer sentiment has taken a huge hit, which is problematic for MA stock along with V shares.

Recently, though, the narrative appears to have shifted favorably for the credit industry. Last week, both Mastercard and Visa reported earnings. In the former’s first quarter, the company delivered earnings per share of $1.83 on revenue of $4 billion. This beat expectations of $1.74 and $3.97 billion, respectively.

Likewise, Visa disclosed encouraging numbers for its fiscal Q2, with EPS of $1.39 and revenue of $5.9 billion, beating consensus targets of $1.35 and $5.75 billion, respectively. Yet neither V nor MA stock responded positively in session following their earnings disclosures.

However, the bulls will probably be quick to point out that the major indices all flashed deeply red to start the new month. Therefore, the volatility could be due to the “sell in May and go away” effect. Certainly, some traders would love securing some profits after a tumultuous period.

As I mentioned at the top, credit cards naturally fit in with the cashless society push. Well before the coronavirus popularized social distancing protocols, the advent of fintech solutions bolstered the idea of going cashless. Now, the pandemic has likely accelerated the drive for digital payments.

But before you dive into MA stock, you better look at the other side of the coin. Some worrying trends may dissuade you from your enthusiasm.

MA Stock Is About to Hit an Unsustainable Environment

Interestingly, during Mastercard’s earnings conference, management stated that the consumer spending appeared to be stabilizing. Obviously, this is what the company needs if MA stock is to enjoy a relatively quick recovery. Unfortunately, I just don’t see where they’re coming from.

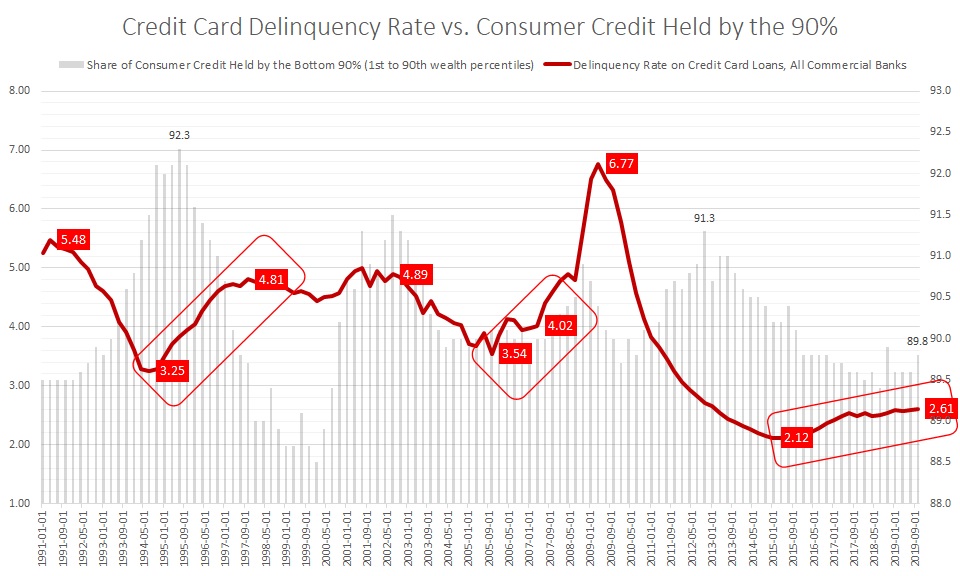

To put it bluntly, most Americans (the first to 90th wealth percentile) own nearly 90% of consumer credit. At the same time, the credit card delinquency rate from all commercial banks has been steadily rising since 2015. Combined with the fact that 30 million Americans have filed for unemployment benefits

since Covid-19 first imposed an economic impact, this is not a sustainable situation.

Of course, the immediate counterargument is that the coronavirus is a black swan event. Once the entire U.S. economy reopens, we’ll be back, stronger than ever. While I’d love to believe that – and I hope to be proven wrong – credit card delinquencies have been rising for years.

When you break down the delinquencies by demographics, you realize that certain age brackets are encountering onerous challenges that prior generations have not suffered. For instance, younger credit card holders typically have lower incomes and huge student loan burdens. Older demos may have trouble balancing their earnings with higher medical costs. Logically, the coronavirus will exacerbate these challenges, not ameliorate them.

Click to Enlarge

Moreover, a significant rise (double-digit percentage gains) in credit card delinquencies has been a leading indicator in the last two recessions (the tech bubble bursting and the Great Recession). Could this third time be signaling the mother of all downturns?

I don’t want to get too ahead of myself. However, I don’t have much confidence in MA stock when I bring in the historical context. Sadly, our economy was worse than advertised heading into this crisis.

Approach This Sector Cautiously

As you might imagine, the 30 million who have filed for unemployment benefits only tell part of the story. In reality, the process for filing is complex. Further, because state benefits offices utilize yesteryear communications infrastructures, the total official figure is probably understated.

Unless a miracle occurs, the delinquency rate for credit cards will skyrocket over the months ahead. That’s because, in addition to the economic pain, the federal aid promised to the American people have yet to be fully distributed.

However, people need money now. Already, millions of Americans are delinquent on their rent. Naturally, this suggests that much credit card usage will be for stretching personal budgets, not actual consumption, as Mastercard would define it. Thus, this is a negative for MA stock.

Right now, the markets don’t recognize it as such; hence, shares are holding onto a tight consolidation pattern. But as the ugliness starts to generate headline after headline, Mastercard won’t be able to deny gravity indefinitely. For the time being, I’d stay away from MA until we get a real picture of the economy.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.