From the perspective of American Airlines (NASDAQ:AAL), Federal Reserve Chair Jerome Powell might as well be a deity. A little more than a week ago, Powell stated that he will “act as appropriate” to sustain the economic recovery. Immediately, that sent AAL stock flying as it implied more inflation, which would theoretically reduce the underlying company’s debt burden.

The following day after Powell broadcast his accommodative intentions, the government released the May jobs report. Frankly, it was stunning, revealing that the economy added 2.5 million jobs. Not only was it confirmation that the worst was behind us, it was also a repudiation of the many doom and gloom prognostications that preceded the report. This too gave AAL stock a hearty lift.

But recently, the Fed Chair played the role of the killjoy. Despite encouraging labor market dynamics, Powell warned that the economy faced “a long road” to recovery. And the day after this stark discussion, the Department of Labor revealed that 1.54 million workers filed for initial jobless claims. Though some of these numbers reflect backlogs due to mass overruns in weeks past, that the tally remains stubbornly high suggests that economic pain is spreading to multiple job categories.

Powell giveth and he taketh away.

Of course, it’s not fair to dump everything on him. For one thing, the competition, including United Airlines (NASDAQ:UAL) and Delta Air Lines (NYSE:DAL) suffered badly as well. Also, the painful reversal in AAL stock was a reminder that the bulls had gotten carried away.

To the Fed Chair’s point, getting past the worst of the crisis doesn’t mean overcoming it. And for American Airlines, it has another problem: math.

A Very Poor Equation Clouds AAL Stock

Personally, I find the subject of airliners in the pandemic era a fascinating one. Few industries reflect the disconnect between real-time fundamentals and technical enthusiasm quite like airline stocks. Perhaps investors were deep diving the discount bin on a misguided narrative.

Whatever the case, I believe some sanity will soon return to this sector. When it does, I wouldn’t want to be overly levered to AAL stock.

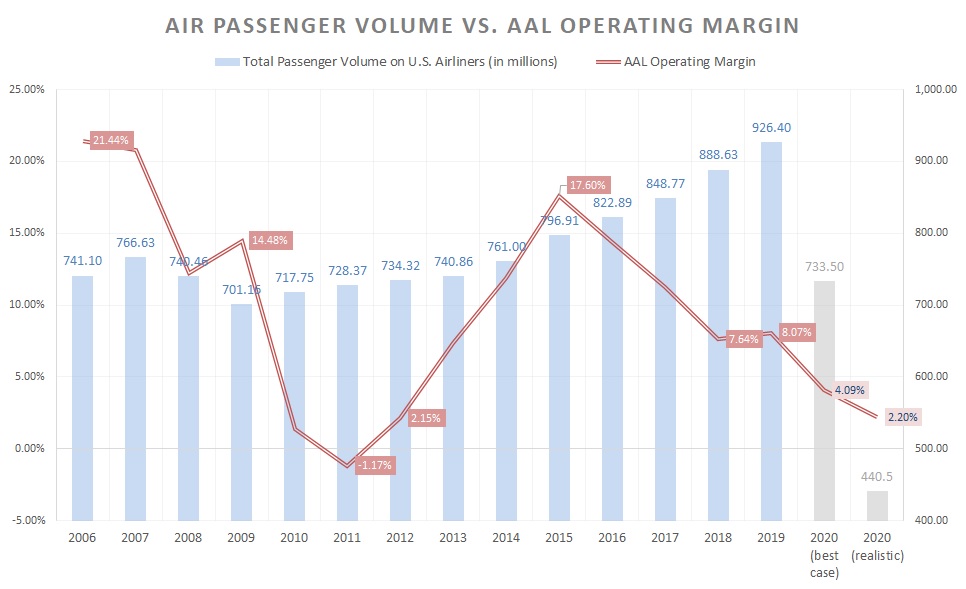

Simply put, the math is extremely unfavorable for American Airlines and almost all its competitors. Even in the best of times, AAL’s operating margins became razor thin – not that they were ever great. But in 2019, passenger volume for those boarding U.S.-based airliners hit 926.4 million. Yet during that year, American Airlines’

operating margin was only 8.07%.

Of course, the novel coronavirus has completely ruptured the travel industry’s paradigm. And here’s where it gets ugly for AAL stock. If we assume a best-case scenario – that is, air travel capacity bounces right back to 2019 levels immediately – total passenger volume would come in at year’s end at a staggeringly low 733.5 million.

Click to Enlarge

In such a situation, I see AAL generating about $27.3 billion in revenue. This is assuming the company maintains its 17.5% market share and its $212.70 revenue per passenger. If so, backing out an adjusted cost of goods sold, along with an assumed operating expense 75% that of 2019 levels, yields an operating margin of just under 4.1%.

That’s a best-case scenario for AAL stock. However, airline experts predict a 52% reduction in global airline demand from 2020’s pre-pandemic forecast. If so, we could see U.S. passenger volume fall to 440.5 million in 2020.

Worryingly, this could see AAL’s operating margin fall to around 2% or lower.

The Room Is Closing In

Let me caveat the above by saying that you shouldn’t take my numbers as gospel. Multiple variables go into profitability margins. Ultimately, the real figure could be lower or higher. But what I’m trying to do is to give you a visual of what to expect for AAL stock.

Nevertheless, what all investors should worry about is the passenger volume forecast for the rest of this year. Again, in an absolute best-case scenario, you’re looking at 733 million U.S. passengers, which is near Great Recession levels. However, I think the expert forecast scenario of 440 million is very realistic.

But the craziest thing is that, either way, it’s terrible for AAL stock. Along with cutting everything they reasonably can, management must also contend with a very poor balance sheet. Essentially, the longer this drought continues, the more the math works against American Airlines.

If that wasn’t enough, the outside fundamentals are hardly supportive. For instance, nationwide protests have likely chilled consumer demand for travel. Further, we’re seeing an uptick in coronavirus cases, which is exactly what this industry doesn’t need.

So, whether you’re a numbers-based investor or a narrative-based one, it’s the same story. We’re just debating how ugly the ending will be.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.