Last week I wrote an article on Whiting Petroleum (NYSE:WLL) showing the math behind the value for WLL stock. I argued that the convertible notes and secured debt were better bargains, given their right to own 97% of the equity in the restructured company. WLL equity owners will get just 3% of revised capitalization.

At the time I wrote that article, WLL stock closed at 84 cents. On Friday, June 5, it rose 62.5% and ended at $1.38 per share. I had shown that the stock might be worth as much as 96 cents per share. But that is still way below where the $1.38 price on Friday.

I also argued that the bonds were a better bargain. I have refined my analysis since writing that article. I want to share some of my thinking on the company and why the notes are a better buy.

Buy the Notes, Not WLL Stock

Whiting Petroleum has cut all its capex spending, but it still has cash flow from its existing wells. In Q1, the company’s cash flow from operations (CFFO) was $37.2 million. Now if you add back the interest expenses it will no longer have to pay going forward, the adjusted CFFO was $82.5 million.

Moreover, I believe the company had unprofitable hedges that are no longer included in its cash flow going forward. So the annualized CFFO going forward can be estimated, on a normalized basis, to be about $330 million. We can use this number to determine whether the notes are a better bargain than the stock.

First, I estimate there is about $3.565 billion in net debt outstanding. I may refine that number, based on upcoming developments.

Second, the notes seem to be trading in the range of between 16% and 18% of par right now. Let’s call it 17.5% on a weighted average basis. That gives them a market value in the newly restricted company (which should occur in several months) of about $624 million.

Third, this implies that the price-to-CFFO ratio for the notes is 1.95 times ($624 million divided by $330 million CFFO). Therefore buying the notes today is like buying the stock at 2 times cash flow, on a normalized basis.

Comparing WLL Stock Valuation to the Notes Valuation

Now if we compare that to the equity, we see the difference in valuation. For example, there are 91.412 million shares of WLL stock outstanding. At $1.38, that gives it a market value of $126 million.

Given that the WLL shareholders will receive only 3% of the implied equity, we can derive what the market cap will be after the restructuring. I used an algebra equation in my last article on WLL stock to derive the value. We can simplify this by just dividing $126 million by 3%. That brings an implied value for WLL stock of $4.2 billion.

That implies that the equity is trading at 12.7 times its annualized $300 million in CFFO. So you can see that the notes are much cheaper at just 2 times CFFO.

Which Value Will Be Correct in the End?

The price of WLL stock likely shot up based on revised hopes that the price of oil will start to surge. This is based on the hope that economic activity will spike, in a sort of V-like fashion.

Click to Enlarge

That is because the most recent U.S. Labor Department report said non-farm payrolls actually rose, rather than fell, by 2.5 million jobs.

But you can see that the implied multi-billion valuation implied for WLL stock after the restructuring is way too high. The notes, however, seem to be in line with comps.

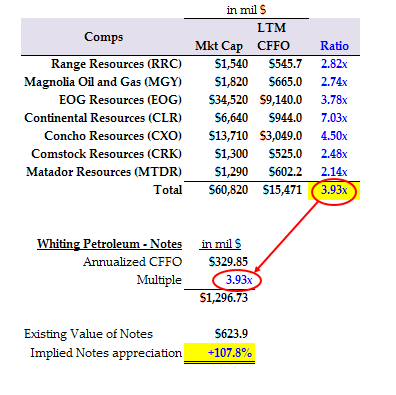

For example, the following table I have put together shows that the average ratio of a number of smaller E&P stocks have a market value of about 3.93 times their LTM CFFO.

Applying this ratio to the normalized CFFO for Whiting Petroleum shows it is worth over twice (+107.8%) the value of the price of the notes today. It puts the value of the revised WLL stock after restructuring at $1.3 billion.

Compare that to the revised implied value of $4.2 billion using the price of WLL stock today. That is a wide difference. I suspect that the true value is much closer to $1.3 billion. Therefore the notes seem like a much better bargain.

If you want more analysis on the WLL notes, I might be able to help, depending on my criteria, and you can contact me on LinkedIn.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide which you can review here.