On Tuesday July 14, Delta Air Lines (NYSE:DAL) helped kick off the second-quarter earnings season. It was joined by banks like JPMorgan (NYSE:JPM) and Citigroup (NYSE:C), as investors turn to DAL stock and others to get an early read on several sectors.

Investors wanted to hear from JPMorgan (NYSE:JPM) to get management’s thoughts on the industry and the economy. They wanted to hear from Delta to see how the airline sector is performing.

In short, the airlines are not doing well.

Breaking Down Delta’s Earnings

Delta’s revenue, excluding some items, plunged 91% to $1.2 billion, which surprisingly beat analysts’ average estimate by $70 million. However, the airline’s loss of $4.43 per share missed the mean estimate by 19 cents as the airline’s system capacity fell 85% year-over-year.

For Q2 of 2019, Delta reported EPS of $2.32 on revenue of $12.56 billion. That highlights just how painful the airline’s Q2 results were this year.

Delta’s adjusted loss came in at $3.9 billion, which excludes $3.2 billion of “items directly related to the impact of COVID-19 and the company’s response, including fleet-related restructuring charges, write-downs related to certain of Delta’s equity investments, and the benefit of the CARES Act grant recognized in the quarter.”

There were some positive aspects of the company’s results, though. It ended the quarter with $15.7 billion of liquidity. And its management is working overtime to make Delta a smaller, leaner airline in order to help it cope with the sudden plunge of demand for flights.

In Q2, Delta’s daily cash burn averaged $43 million, but it was able to reduce that figure to $27 million in June. That’s not great, but it’s down 70% versus late March. Further, management hopes to “achieve breakeven cash burn by year end.”

Delta is reducing its cash burn and has plenty of liquidity. Its business most likely bottomed in Q2 and is recovering.

But the company is still burning plenty of cash, and its last four months was monstrously bad. Delta is starting to recover, but it’s bouncing back slowly and not enjoying the V-shape recovery many were hoping for. Finally, this comment from Delta CEO Ed Bastian doesn’t make me feel better about its short-term outlook:

“Given the combined effects of the pandemic and {the} associated financial impact on the global economy, we continue to believe that it will be more than two years before we see a sustainable recovery.”

What Should Investors Do With DAL Stock?

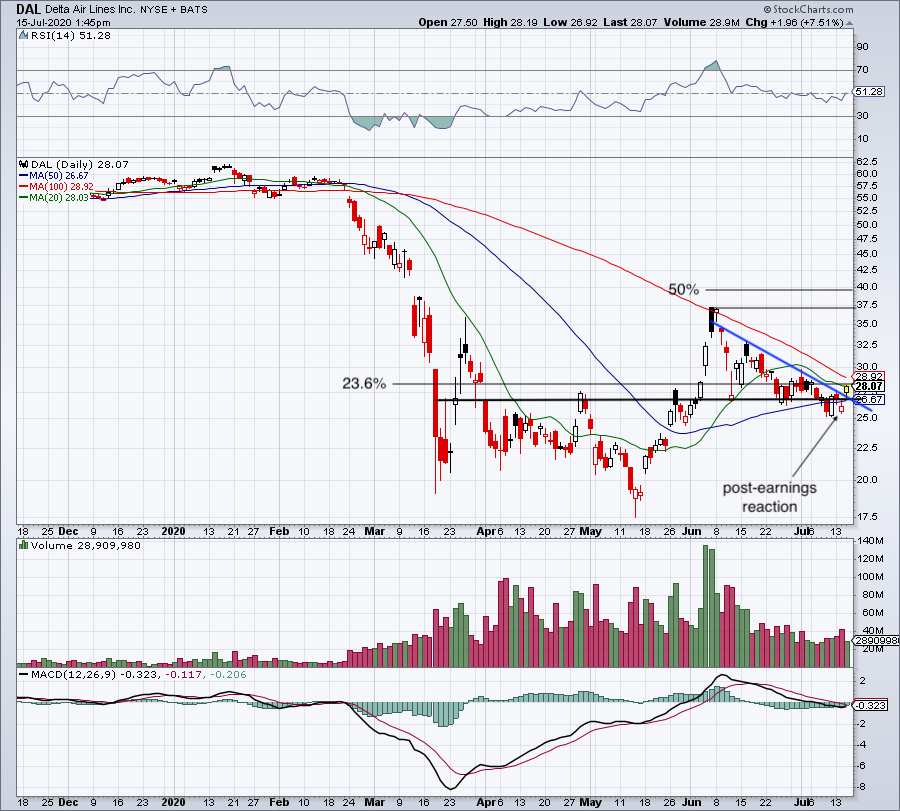

Click to Enlarge

What are we supposed to make of this report? On the one hand, it’s not very encouraging. Sure, Delta will survive, but it will be some time before it begins to thrive. That said, the stock did not drop tremendously in the wake of the report, and that might be the most telling signal.

The initial reaction was discouraging, but not catastrophic. DAL stock broke below its 50-day moving average, but fell just 2.6% in its first trading session after it announced its earnings. As I outlined in a previous article, a move below $25 by the stock would have been bleak. Even after yesterday’s 9.5% rebound by the shares, that statement remains true.

From a technical standpoint, Delta is not out of the woods. As much as I like the fact that the shares reclaimed their 50-day moving average, they still have work to do.

Specifically, I want to see DAL stock climb above its 20-day moving average and clear its declining 100-day moving average. The latter metric acted as the stock’s resistance in June. If the shares rise above $30, the door will be open to its June highs near $37, and they could even reach the 50% retracement level, which is near $40.

You heard it right from the horse’s mouth when Bastian said he believes it will take more than two years to see a sustainable recovery. That’s a tough pill to swallow, even though the charts seem to be ignoring the warning for now.

I pay attention when I see a stock holding up despite poor news. That’s why DAL stock may be worth trading if it clears $29. However, those who want to invest in the stock over the long-term will probably have a turbulent ride.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.