Bristol-Myers Squibb (NYSE:BMY) is a valuable dividend stock worth at least 20% more than today’s price. That was the conclusion of my last article on BMY stock.

Why does that matter? Well, Bristol-Myers is going to report its second-quarter earnings this week. The stock is very undervalued when you consider its dividend yield and price-earnings ratio. I believe BMY stock will move higher as the market realizes how cheap it really is.

Earnings estimates for Q2 are $1.47 per share based on Seeking Alpha‘s poll of analysts. Yahoo! Finance has an estimate of $1.48. These estimates represent a gain of over 25% from a year ago when EPS was $1.18. BMY stock, by the way, is up about 29% in the past year. I believe it has much further to go.

Using the Dividend Yield to Value Bristol-Myers

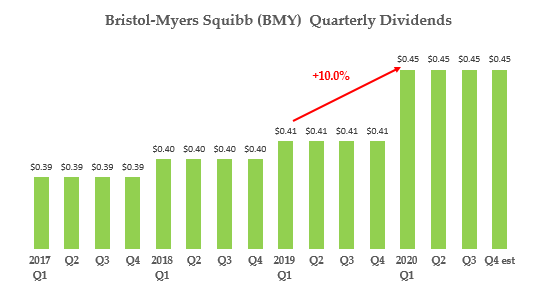

Why do I think BMY still has gas in the tank? One reason is that Bristol-Myers is likely to raise its dividend by at least 10% after the next quarterly dividend payment. I estimate that the new annualized dividend will be $1.98 per share for the next year.

You can see the historical dividend payments by the company over the past four years in the table at the right. It shows that the most recent increase in the dividend was 10%.

Click to Enlarge

Assuming Bristol-Myers raises its dividend another 10%, BMY stock trades now at a forward dividend yield of 3.4%. But the average dividend yield for the past four years, according to Seeking Alpha, was 2.97%.

Therefore, BMY stock should be worth $66.67. That represents a potential gain of over 13% for BMY stock.

BMY Stock Is Worth More Based on Its Historical P/E

Moreover, as I explained in my last article, Bristol-Myers has had an average price-earnings ratio of 27.7 times over the past five years. But this year, the stock is trading for just 9.5 times its expected 2020 earnings of $6.20 per share. And for 2021, BMY is incredibly cheap at just 7.94 times expected earnings of $7.38.

The idea here is that the stock will not stay at such a cheap P/E ratio given its history of trading much higher. Therefore, at the average P/E of 27.7 times, BMY stock is worth at least 193% more than today.

In other words, 27.7 times $6.20 per share equals $171.74. This represents a gain of 193% over the closing price on Friday, July 31, of $58.66 per share.

Now let’s assume it takes three years for BMY stock to rise to this P/E ratio. That implies its average annual gain will be 43% per year over the next three years.

What Should You Do With BMY Stock?

If earnings meet or beat the levels that analysts estimate, I suspect that the stock will start to rise based on a revaluation of its P/E ratio.

For example, even if the P/E ratio were to rise 65% to 13 times expected earnings of $6.20 this year, the stock would rise to $80.60. That represents a potential gain of 37% between now and the end of 2020 — or shortly thereafter.

Moreover, if BMY stock had a P/E of 16 times 2020 expected earnings, the average of its peers, it would rise to $99.20. That represents a potential gain of almost 70% from today’s price.

Therefore, the upside with this stock is substantial. Bristol-Myers should not be trading at this low a price-earnings ratio, especially given its expected growth.

The patient value investor will average cost into BMY stock. It has the potential to gain a substantial amount just based on a re-rating of its multiples.

Last quarter the stock rose after its earnings came out, as Barron’s Josh Nathan-Kazis reported. I suspect the same will happen this quarter. Moreover, the company has already guided for its earnings this year to be between $6 and $6.20 per share.

That is the earnings on which I based my revaluation of its P/E ratio. Therefore, I expect that most serious value investors will average cost into this stock to participate in its expected re-rating.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide, which you can review here.