To little surprise, Lyft (NASDAQ:LYFT) did not report a good earnings result on Aug. 12. Wall Street saw that coming from a mile away, given how hard the economy and the travel industry were hit by the novel coronavirus. However, investors were hopeful that Lyft stock would rally despite the result.

When a stock rallies despite bad news — or falls even though the news is good — it’s a sign for investors to pay attention.

Unfortunately, that’s not the action we’re getting in Lyft, which continues to struggle. Let’s look at the quarter, then the stock.

Lyft’s Earnings Needed a Lift

A loss of $1.41 per share beat expectations by 10 cents, while revenue of $339.3 million missed consensus estimates by $10 million. That sales figure slumped almost 61% year-over-year.

While rides were up 78% in July vs. the lows in April, active riders were down 60% to 8.7 million. That was well short of estimates looking for 10.5 million active riders in the quarter.

CFO Brian Roberts said that Lyft is on track to realize $300 million in annualized cost savings by year end. “These steps position the Company to achieve adjusted EBITDA profitability with 20 – 25% fewer rides than originally contemplated in our fourth quarter 2021 target.”

The company ended the quarter with $2.8 billion in cash and short-term investments, which should buy it some time as it pertains to liquidity.

The quarter itself is excusable, but investors have to see “the turn.” That is, we know the worst is behind Lyft, Uber (NYSE:UBER), Delta Air Lines (NYSE:DAL) and others. But airlines are telling us that demand has plateaued, and without Lyft or Uber telling us that demand growth persists and rides are climbing in a fairly robust manner, investors are left wanting more.

That’s as we’ve already seen the stocks rally. Even with Lyft’s post-earnings dip of roughly 5%, shares are still up 100% from the lows.

Admittedly, the stock deserved a bounce from the lows as business has improved drastically from the lows. We need a drastic improvement from here to justify another leg higher and that’s where Lyft stock runs into trouble.

Breaking Down Lyft Stock

The market is being divided into the haves, the have-nots and the neutrals. Essentially, there are companies with growth (now fetching a premium), without growth (badly lagging the indices) and those that are lost at sea (performing about in-line with markets).

As travel trends pick up and as life returns to normalcy, there will eventually be demand for Uber and Lyft rides. But without sporting events and concerts, lower employment and downbeat travel trends, there is simply a lack of demand for ride services.

Current forecasts call for a 26% decline in sales this year and for a loss of $2.40 per share. 2021 estimates are better, though. They call for a loss of 94 cents per share on roughly 50% revenue growth. Sales are forecast to come in at $4 billion that year, ahead of 2019’s tally of $3.62 billion.

So there is some promise for 2021, but keep in mind, the uncertainty here is quite high. Rather than bottom fish with Lyft, I would rather stick with the stocks in strong uptrends and those with growth.

The exception here is rotation. If there is a rotation out of tech and into the beaten-down sectors, Lyft stock may be ripe for a bounce. However, that bounce may not be long lasting without some sort of significant improvement in the underlying business.

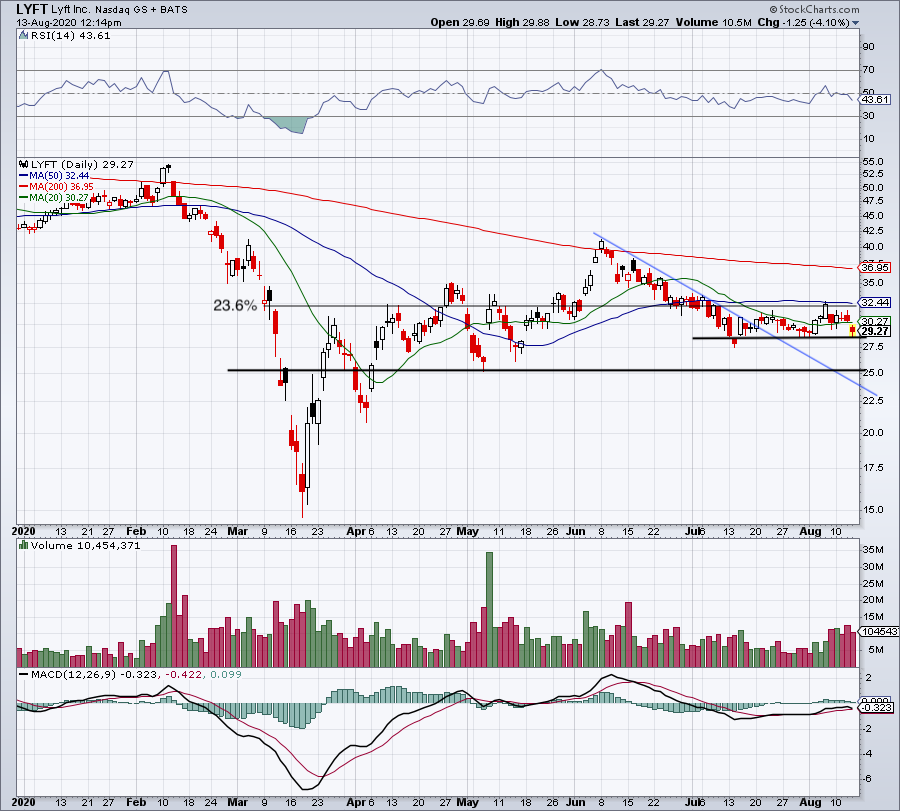

Trading Lyft

Click to Enlarge

So far, the action is pretty muted, but bulls don’t want to see Lyft stock lose the $28 area. Below the July low at $27.51 could put the May low near $25 in play. Based on the reaction so far, that may not be in the cards without a broader stock market correction.

Below $25 and this one could get ugly. On the upside, it’s hard to get too bullish on this name while it’s below its 20-day and 50-day moving averages, as well as the 23.6% retracement.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.