Etsy (NASDAQ:ETSY) stock has been red-hot from the lows. This name sold off with the rest of the market, but ETSY stock came back to life when investors realized it was benefiting from the novel coronavirus situation.

Since then, the stock has been barreling higher, climbing to new all-time highs. Given the run in FAANG, the Nasdaq and e-commerce platforms, the surge in Etsy isn’t that surprising.

But here’s the thing. When there is a secular growth stock in play, it can be hard to buy. Not because the story isn’t convincing enough, but because the stock tends to rip and it feels like you’re stuck chasing.

Here are three reasons to consider Etsy stock on the long side.

You’re Not Chasing

Click to Enlarge

Take a look at the chart above, which highlights two things. First, shares exploded lower off the March lows. Etsy bottomed near $30, put in a higher low around $35 (blue circle) and ultimately flew up toward $140.

However, the second thing it shows is a beautiful consolidation. Shares tagged a high of $141.41 on Aug. 10. Since then though, the stock has slowly drifted lower. The correction was not fast or violent. Instead, it was orderly as investors saw the stock react strongly on both tests of the $105 area.

That’s proving to be an area where investors are clearly willing to step up and own the stock.

In any regard, shares remain about 15% below the all-time high, while correcting as much 27% from the August highs when Etsy hit its recent low. Now taking back the 20-day and 50-day moving averages, bulls are starting to regain momentum.

A close over the 50-day puts the three-times range extension in play near $130. Above that and the $141.41 high is back in play, along with a possible run to the 361.8% extension near $150.

On a move back below the 20-day and 50-day moving averages, see if we get another test of the low-$100s. Below could put $96 in play, near the two-times range extension and the prior support area.

Etsy Stock Has Growth

It’s hard to avoid chasing a stock when it’s screaming higher and hitting new highs, especially

when it’s a high-growth name. That makes the recent dip all the more attractive.

Etsy is forecast to grow revenue 83.7% this year, while earnings expectations call for 155% growth. That’s monstrous growth, underscoring how the Covid-19 situation is helping to fuel Etsy’s revenue.

There’s a downside though, which is next year. Estimates slow dramatically to earnings and revenue growth of just 9.3% and 13.7%, respectively.

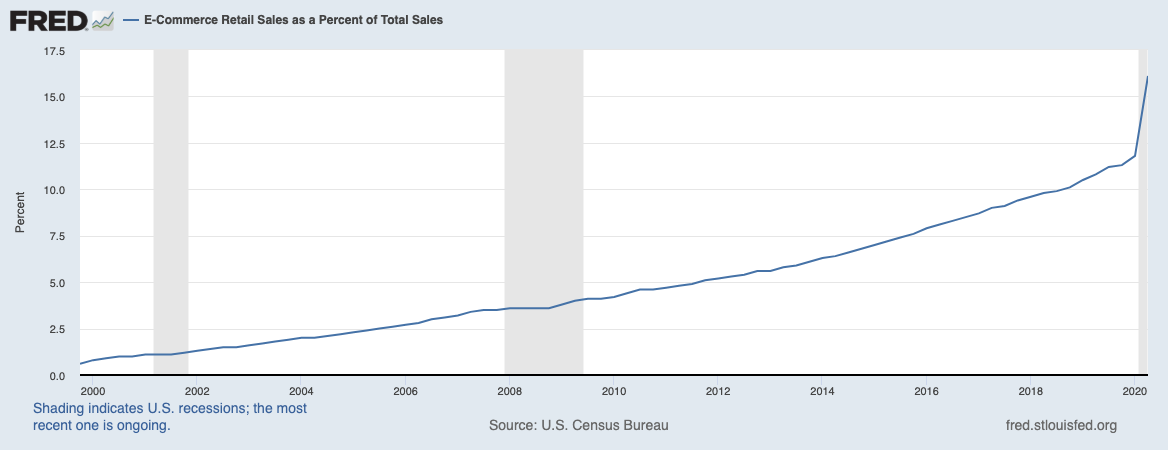

There are two ways to look at these estimates. First, we can argue that they are far too conservative given the influx into e-commerce platforms. This paradigm shift (illustrated below) is part of a broader, secular theme and will benefit Etsy stock in the short- and long-term.

The other ways of looking at next year’s estimates? By simply being impressed that Etsy will still find a way to grow after such an accelerated year of business. 2020 isn’t proving to be a pull-forward year. That’s where we see big growth in one year and a “reversion to the mean” as revenue falls off to a more “normal level” of business.

No, instead we’re seeing additional growth after an explosive growth year.

Click to Enlarge

The Fundamentals Are Solid

Competition has picked up in this space, but like other dominant platforms, Etsy has held its own. It’s consumers’ choice for buying unique and handmade items. As a result, Etsy commands a noteworthy moat.

Beyond that, we’re talking about a company with solid financials as well.

This isn’t 1999 or 2000, where dot-com names are going public with no revenue, bloated balance sheets and a pipe dream. Etsy boasts more than $1.1 billion in trailing revenue, is profitable and free cash flow positive. The last of that list is a big one, as cash flow is a key metric for investors. Get a load of Etsy over the last few years:

| Year | Free Cash Flow |

| 2016 | ($991,000) |

| 2017 | $54.2 million |

| 2018 | $142.9 million |

| 2019 | $189 million |

| Trailing 12 Months | $364.6 million |

Finally, the company has $1.19 billion in current assets vs. just $279 million in current liabilities. The former is more than four times the size of the latter. Cash and equivalents grew to more than $1 billion in the most recent quarter, while Etsy has no current debt.

While it does have about $800 million in long-term debt, that’s little to worry about for a company that can turn revenue into profit and already has a strong balance sheet. Particularly for a smaller, high-growth company.

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now.