Last month, I put to readers the proposition that if you love day trading based on data analytics, you may want to consider Marathon Oil (NYSE:MRO). The oil sector was one of the worst hit by the novel coronavirus pandemic — without much need for traveling and commuting, demand for petroleum-based products plummeted. And, among the deepest sufferers were speculative plays like MRO stock.

However, on a quantifiable basis, Marathon Oil wasn’t completely speculative in the way that I argued Whiting Petroleum (NYSE:WLL) was. Long story short, MRO stock featured a strong correlation with the underlying oil price. On the other hand, WLL did not have a meaningfully relevant correlation with oil. Therefore, buying WLL was akin to taking shots in the dark.

Of course, this wasn’t a wholesale approval of MRO stock. Again, we’re talking about a high-risk, high-reward name. However, as long as you believed in the oil recovery narrative, Marathon shares represented a solid bet. Basically, where oil goes, so too will MRO.

Up and Down With MRO Stock

But if a strong correlation exists, that means the opposite is also true. That is, if oil starts to lose trading sentiment, the market risks taking down MRO stock. Unfortunately, this is what might be happening right now.

Since the start of this month, oil prices — as mirrored in United States Oil Fund, LP (NYSEArca:USO) — have dipped, making for some uncomfortable moments. The exchange-traded fund is off 11.8% in the period. As well, the major indexes are shedding some of the new normal enthusiasm. Well, at least that’s the hope — a correction at this point is healthy.

Unfortunately, the bigger picture is an incredibly ugly one. Not only do we have health and economic crises, natural (or perhaps unnatural) disasters have ravaged the nation.

It’s All About Demand or Lack Thereof

Throughout this pandemic, I’ve consistently harped on what matters most to companies like Marathon Oil: demand. No surprise there, without demand for petroleum-based products, there’s no point in buy something like MRO stock. Without supportive fundamentals, shares will collapse.

Nevertheless, waiting for confirmation that demand will be back presents an opportunity cost. The best rewards typically entail the greatest risk. Put another way, you must assume that oil will make a comeback and gamble today accordingly. As it should be, the reward for betting on a sure thing is limited.

In that regard, the case for oil stocks is a confusing one. If you’ve read my stories on the oil market, you’ll know that I frequently depend on TomTom.com’s weekly automotive congestion level to determine real-time oil demand. If more cars are on the road, that’s obviously positive for oil prices.

But when I analyze congestion levels for high-traffic cities like Los Angeles, congestion is still down 60% or so against the year-ago period. Still, is TomTom.com a reliable source? After all, we’ve seen reports from other regions that indicate traffic has more or less normalized.

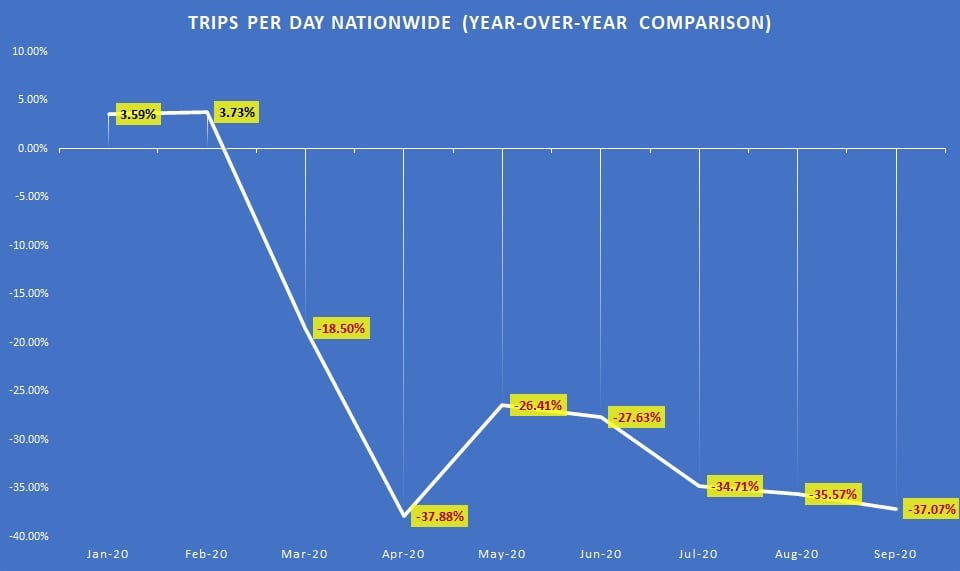

To get a better idea of demand, I turned to the Bureau of Transportation Statistics. Based on the government agency’s mobility trends, specifically the number of daily trips, I’m confident that TomTom.com’s bearish analytics reflect reality.

Click to Enlarge

For instance, in July and August, Americans took a daily average of 936 million trips (see chart, right). This amounted to an average decline of 35% year-over-year. Moreover, this is a negative outcome relative to the average trips seen in May and June (one billion trips or down 27% YOY).

Unfortunately, most Americans aren’t getting out as often as they used to and why should they?

Marathon Faces an Uncertain Fundamental Future

Perhaps what bothers me the most about MRO stock and the oil sector in general is the timing of the underlying market’s volatility. Naturally, I understood why oil prices were muted during the peak of the crisis. And I can appreciate why price growth started to fade in June and July.

Simply, with coronavirus cases rising, piling into MRO stock didn’t make much sense for conservative investors. But with cases falling now, you’d expect on one level for oil to pick back up.

Clearly, it’s not doing that, quite the opposite in fact. And that may be a clue that Wall Street believes — on good evidence — that we’ll hit a second wave. If so, this really damages the narrative for the oil market. And don’t misread this. I’m not picking on the sector just to be mean. Honestly, this is a matter of looking at the facts.

A return of the coronavirus means at the very least that companies that operating remotely will continue doing so. As well, a resurgence will kill travel demand. All this points to a rough outing for Marathon Oil. Unless you have an extraordinarily high conviction that “black gold” will make a comeback, I’d steer clear of MRO.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.