Mastercard (NYSE:MA) is up over 19% year-to-date and most of that gain came in the last month which showed a 16%+ rise. The bottom line now is that MA stock is simply too expensive.

Most investors should probably wait for a pullback in the stock before taking a position in this fine company. At that point, there might at least be a notion of a margin of safety in buying it.

The stock’s rise in August came after Mastercard reported its second-quarter earnings on July 30. Analysts were expecting adjusted earnings per share (EPS) of $1.18, but the company outperformed with adjusted EPS of $1.36. However, this was still down 28% from last year.

Looking at the Valuation Carefully

The company indicated in its presentation and its conference call that it would not provide any guidance for Q3 or even for the year. That helps, thank you very much. Just when analysts and investors need some guidance, there is no way to tell if things are improving.

We will have to wait until the company provides its Q3 numbers, probably at the end of October. Let’s look at what some analysts are projecting.

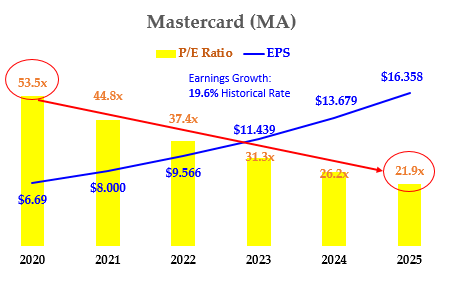

Here is where MA stock stands now, in terms of valuation. Yahoo polled 31 analysts who estimate on average that 2020 EPS will be $6.69. That puts MA stock on an astounding 54 times 2020 earnings.

Here is what that means. If you bought 100% of Mastercard’s shares today, it would take 54 years for your purchase price to reach breakeven. This assumes that earnings don’t rise or fall.

But what if earnings grew on average 10% per year for 10 years. By year 10, earnings would have compounded by 236% to $15.35 by the end of 2029. Moreover, the cumulative earnings would add up to $106.62.

That works out to 29.8% of today’s price of about $359. In fact, it would take between 22 and 23 years for all the cumulative earnings to equal today’s price.

That is a long time to wait for breakeven, and it illustrates how highly expensive MA stock is at present. Even if you take into account projected earnings for 2021, at $8.71, it still trades for over 42 times earnings. To put it succinctly, this is not a bargain stock.

Long-Term Growth Vs. Valuation

Ten years ago, in 2009 the company made $11.19 per share, fully diluted. However, on Jan. 22, 2014, there was a 10-for-1 stock split. So, in effect, earnings per share were $1.119 in 2009 on an adjusted basis.

Therefore, earnings over the past 10 years have risen from $1.119 to $6.69 this year, or 5.97 times. But, on a compounded annualized growth rate (CAGR) basis, that represents 19.58% growth every year.

I am impressed with that level of growth. That is twice the 10% number assumed in our calculation above. For example, now if you bought 100% of MA stock, it would take just 14 to 15 years to reach breakeven with its historical 19.6% annual growth rate.

That is much earlier than the earlier estimate of 22 to 23 years with a 10% annual growth.

Click to Enlarge

It also explains why investors are willing to buy a sliver of the company at today’s estimated 54 times earnings. For example, using its historical growth rate, in 1o years, EPS will be five times higher at $33.45 per share.

In other words, in 10 years the stock’s price today of $359.19 is only 10.7 times its earnings. In fact, in just five years, the EPS would be $16.358 per share.

As the chart on the right show, that would mean it is selling for just 21.9 times earnings in five years. Now the stock looks much cheaper – in just five years. That is how investors justify paying today’s high price. They assume the company’s 20% earnings growth rates justify the high P/E ratio.

What to Do With MA Stock

That is fine unless you think that a $356 billion market capitalization stock may eventually succumb to the law of large numbers. In other words, Mastercard’s historical 19.6% growth rate might begin to slow due to its size.

I tend to believe that it will. Therefore, absent any guidance from the company, I believe that paying 54 times earnings, even if it means 21 times earnings in five years, is too expensive.

I suspect that there will be an opportunity to buy the stock cheaper some time in the future.

On the date of publication, Mark R. Hake did not have (either directly or indirectly) any positions in any of the securities mentioned in this article.

Mark Hake runs the Total Yield Value Guide which you can review here.