Typically, most financial analysts will steer you away from heavy exposure to resource mining firms like Piedmont Lithium (NASDAQ:PLL). Even with miners associated with fundamentally bullish markets, miners are not commodities. Thus, they have to keep the lights on, among other things. As a result, you ordinarily won’t find Piedmont Lithium stock in the portfolio holdings of conservative investors.

Of course, these aren’t ordinary times. Although the novel coronavirus pandemic imposed severe economic headwinds against multiple industries, the electric vehicle market has weathered the storm better than many anticipated. Part of that has to do with the realization that the global automotive supply chain is incredibly vulnerable to disruption. With fewer moving parts, EVs will likely be more resilient in the face of another disruptive event.

Tesla (NASDAQ:TSLA) has enjoyed ridiculous demand. Yes, there is the element of supply chain insulation that I just mentioned. But in addition, the brand name appeals to well-to-do folks. And these are the people whose personal economies have benefitted from the pandemic. Logically, higher demand for Tesla EVs translates to more revenue-making opportunities that should support Piedmont Lithium stock.

Recognizing this, Piedmont announced that it will raise money by selling equity shares. Management of this Australian firm has a goal of selling up to 1.5 million American depositary receipts. According to Barron’s Al Root, the “sale has the potential to bring in roughly $45 million to company coffers,” writing:

The company might use the cash toward the hard rock mine it is developing in North Carolina. (Most of the world’s lithium today comes from evaporating salt from brine ponds.) Early phases of Piedmont’s mine should cost about $170 million, according to CEO Keith Phillips.

Piedmont is also getting some money from Tesla. Piedmont stock soared more than 200% on Sept. 28, days after Telsa’s battery event, when Tesla signed a deal for five years of lithium-ore supply, with a possible extension for another five years. Deliveries from Piedmont to Telsa are expected to start around 2022.

On that note, everything seems to be moving favorably for Piedmont Lithium stock. However, shares have been all over the map since mid-September, raising the question about their future viability. Frankly, it’s something to consider before diving into PLLstock .

Piedmont Lithium Stock Could Be Rising on False Pretenses

If you’re not suffering from tunnel vision, it’s incredibly difficult to take the economic narrative presented before us — particularly by the Trump administration — without a few grains of salt. Yes, the national unemployment rate dropped to 7.9% in September, which of course is a welcome change. During the worst of the crisis, we were looking at double-digit unemployment.

At the same time, permanent job losses have accelerated to just under 3.8 million, a significant acceleration from February of this year. Plus, the number of weekly jobless claims remains stubbornly high. That’s why it’s difficult to just accept soaring housing prices as an indication of a recovering economy. We have data that simply contradict each other.

And that brings me to Piedmont Lithium stock. While I appreciate the argument that EV demand is rising, you want to be careful here. I’m not trying to necessarily dissuade you from PLL. Rather, if you’re going to gamble, do so with money that you can afford to lose without consternation.

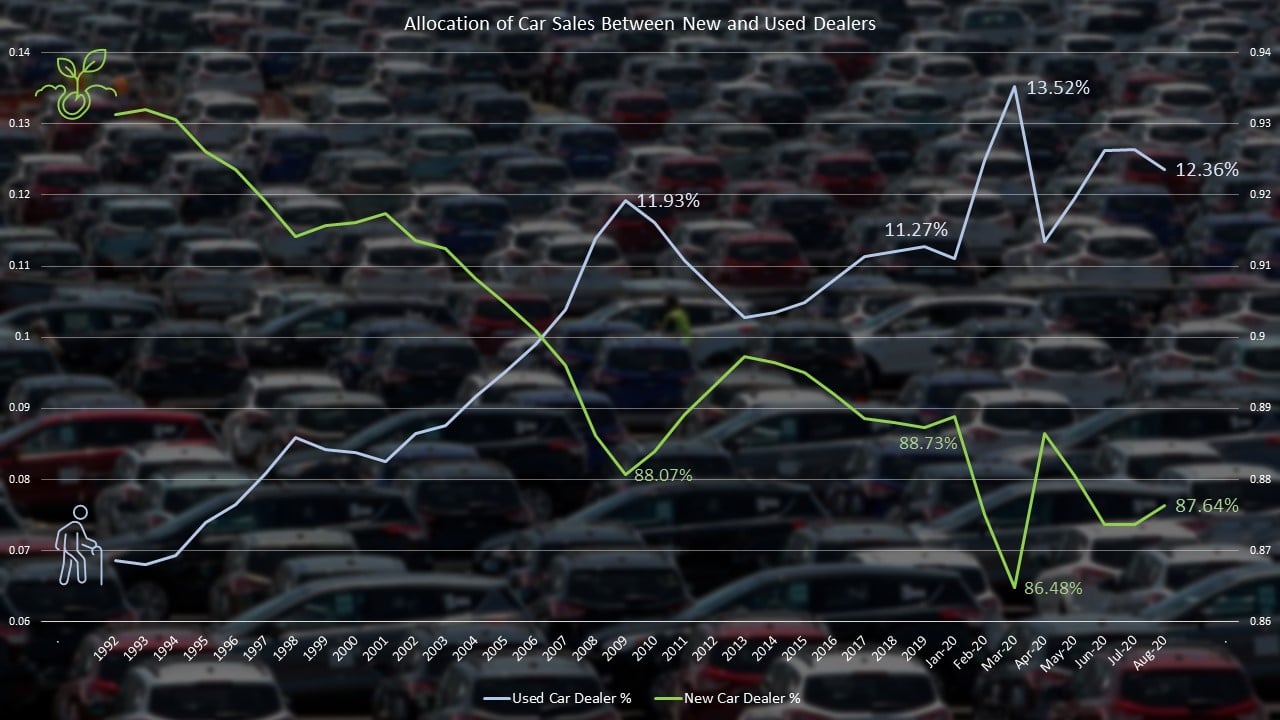

Primarily, I say this because the automotive economy does not look good. Historically, the share of

new dealership auto sales compared to used car dealerships has been overwhelmingly dominant. For instance, in the 1990s, new car dealer sales represented 92.4% of total dealership-based auto sales.

Click to Enlarge

However, the proportion of used car dealership sales increased to an average of 9.6% during the 2000s decade, which of course featured the beginning of the Great Recession. Thus, it’s not surprising that more people sought to purchase used cars.

But in the 2010s decade, averaged used car dealership sales still increased to nearly 11%. And in the year-to-date up to August (the latest data point available), used car dealership sales represent over 12% of total dealership sales.

If the economy was truly healthy, then we should see a normalization of the automotive sector. That means new cars should take much greater share of the retail market than they’re doing right now.

If we extend the logic further, new car sales may be hitting a peak. In August, new car dealership sales were down 2.2% year-over-year. For used cars over the same period, sales were up nearly 17%! That’s not good news for Piedmont Lithium stock because it implies that consumers are increasingly becoming price sensitive in the new normal.

Plus, Edmunds.com reports that the cheapest new EV is nearly $31,000. I’m sorry, but that’s not going to cut it during an economic crisis. Therefore, whatever new EVs were sold has probably reached or is reaching a peak. And that means there’s a risk that PLL is ramping up operations for demand that might not be there. Hence, I’m concerned about overexposure to Piedmont Lithium stock.

Best to Wait It Out

Granted, shares can rise on other factors. For instance, the digitization of everything incentivizes greater lithium demand. It’s not like Piedmont cares how its lithium products are used, so long as they’re used for something.

However, the company’s stock sale has been inspired significantly by Tesla and its forecasted demand. Thus, the fate of Piedmont Lithium stock depends greatly on the EV maker. It’s very much possible that the power of the Tesla brand can ride out a possible recession. After all, the rich are getting richer, which supports TSLA.

Still, with the regular consumer economy showing cracks, you may want to sit out Piedmont Lithium stock for now. Look, no matter how great the Tesla story may turn out to be, PLL is a derivative partner. And that means Tesla can always find an alternative while the opposite argument is likely not valid.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.