The entire market has been mixed and choppy. The choppiness started before the election and after a strong, week-long rally, it’s back to choppy again. The same can be said for Apple (NASDAQ:AAPL), which has seemingly had trouble picking a direction.

As a result, it has investors wondering if now is an opportune time to buy the iPhone maker.

Unfortunately, there’s no crystal ball when it comes to investing. If the market takes a haircut — for political reasons or due to the novel coronavirus, for example — Apple will likely get hit too. But for long-term investors, Apple is one to consider owning. Here are three reasons why.

Product Refresh Amid Covid-19

Apple’s product launches have been a bit different this year due to the coronavirus. That said, Apple hasn’t slowed down on its products.

After using Intel (NASDAQ:INTC) for its CPU needs since 2006, Apple just unveiled the new M1 chip in its Macbook Air, Macbook Pro and Mac Mini. Customers can still buy some Apple computers with Intel’s chip, but the shift is happening now and from what we can see, the specs are pretty solid.

The company also unveiled four new iPhones in October: the iPhone 12 and 12 Mini, and the iPhone 12 Pro and the 12 Pro Max. With a range of prices, this should help generate revenue as Apple now offers its first 5G iPhone lineup. During the same event, it also unveiled the HomePod Mini.

Finally, in September the company updated its Apple Watch, the iPad and iPad Air, and introduced Apple One, its new Services bundle.

From September to November, Apple introduced and updated a number of key products. This should ensure solid sales during a robust work-from-home market and holiday season.

Apple Has Growth

Apple recently began its fiscal 2021 year. For the year, analysts expect 14.5% revenue growth to $314 billion. Consensus expectations call for an even better year of earnings growth, with estimates of 20.4%. That bodes well for margins in FY 2021 (the current year).

The estimates for FY 2022 may be conservative, particularly if we can get a significant rebound in the economy next year. In any regard, estimates call for 5% revenue growth and 9% earnings growth.

To me that is pretty solid growth and again, I could see Apple topping those figures next year. Particularly on the earnings front.

After the stock’s latest dip, shares trade at roughly 30 times this year’s earnings estimates. Now this is important, because I’ve heard this argument a lot, which says that Apple is a sell because the valuation is far beyond its typical range.

On a price-to-earnings ratio, that statement is valid. However, the argument — in my humble opinion — is not valid.

One part of that is Apple’s financial position. In short, the company has proven that it can grow with or without a pandemic. It also offers investors assurance with its mighty balance sheet.

But more than that, it deserves its higher valuation because of its Services business. In FY 2020, Services revenue came in at $53.76 billion. That was up 16.1% from 2019 and made up just under 20% of total revenue.

The growth is worth a premium, but the real value here are the margins. In FY 2020, Apple Products generated a gross margin of 31.5%, while gross margins for Services came in at 66%. That figure is almost double the Products business and given the growth of this unit, justifies the current valuation.

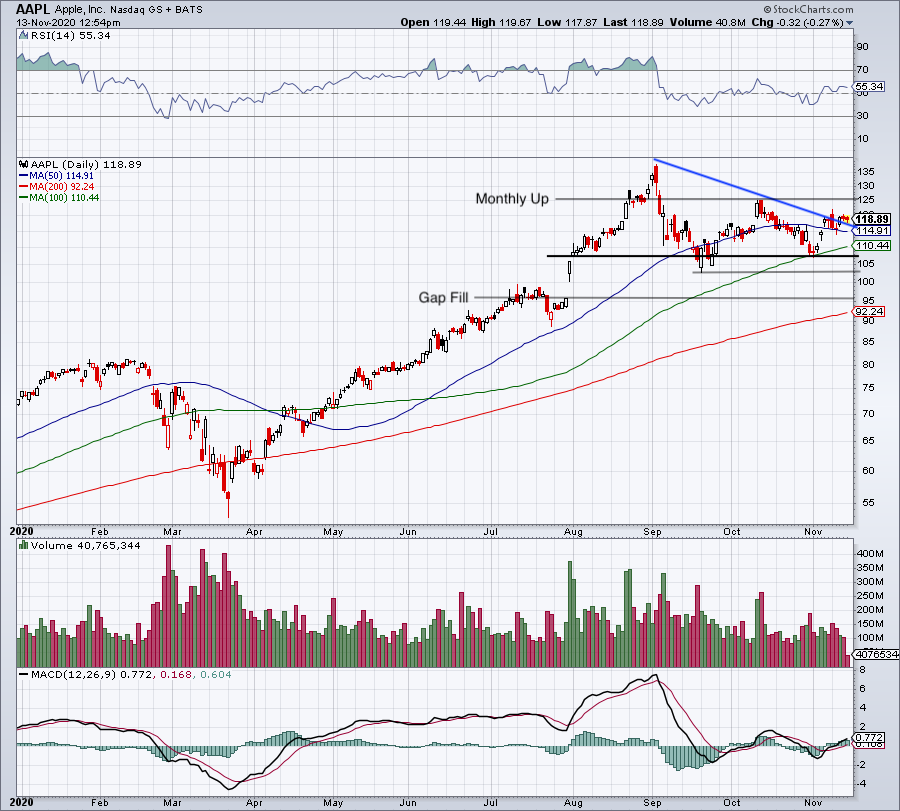

AAPL Stock Charts Are Bullish

Click to Enlarge

Finally, the charts are looking better. On the daily chart above, you can see that the stock has broken out over downtrend resistance (blue line). This looks similar to the S&P 500, but is better than the Nasdaq. The latter has yet to break out over downtrend resistance.

Now, this is just a start. For more nimble traders, they see this move and want to be long. However, to confirm their long bias, they want to see a rotation.

That rotation starts with a move over this month’s high, near $222. Above that puts the October high in play up near $225. If the stock can move above that, it could challenge its prior all-time highs near $237.

A move lower also makes Apple interesting, though.

If shares rotate below $114.13, it puts Apple below this week’s low. That could set up for a larger move down and give longer-term investors a better dip-buying opportunity.

On the date of publication, Bret Kenwell held a long position in AAPL.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell.