Editor’s note: This column is part of InvestorPlace.com’s Best Stocks for 2021 contest. Charles Sizemore’s pick for the contest is Enterprise Products Partners (NYSE:EPD).

This time last year, the world was “normal.” We had heard a little something about a virus coming out of China, but it seemed a world away — and the best stocks were still thriving. Then, just months later, the entire world turned upside down.

I don’t know what 2021 will bring us. If anything, 2020 taught us why it’s important to be humble in our forecasts. But after a chaotic start to the year, which will likely include the worst months yet of the pandemic, I expect the theme for the year to be normal. Stuffy, boring, normal.

That said, for the InvestorPlace Best Stocks for 2021 contest, I’m going with one of the most stuffy, boring, normal stocks you can buy in pipeline giant Enterprise Products Partners (NYSE:EPD). The company moves natural gas and natural gas liquids from point A to point B. It owns more than 50,000 miles of assorted pipelines, 260 million barrels of storage capacity and other infrastructure assets.

That’s it. There’s no cutting edge new technology here. In fact, if the green energy tech visionaries are successful, EPD might not even be in business 20 or 30 years from now. But in the meantime, we stand to make a lot of money in one of the few truly cheap sectors left in an otherwise pricey market.

The Lowdown on Enterprise Products

Overall, enterprise is considered by most industry watchers to be one of the bluest of blue chips in this space. In an industry known for being run by risk-seeking cowboys, Enterprise has long been the buttoned-up, sober voice of reason. The company has always kept its debt levels reasonable, refusing to follow the path of many of its peers toward leverage-fueled excess. As of December, the company reported debt at 3.5 times annual EBITDA. To put that in perspective, rival Kinder Morgan

(NYSE:KMI) sports a leverage ratio of 5.7 times.

Furthermore, EPD’s revenue stream is almost entirely fee based, with only 13% of its revenues tied to commodity prices.

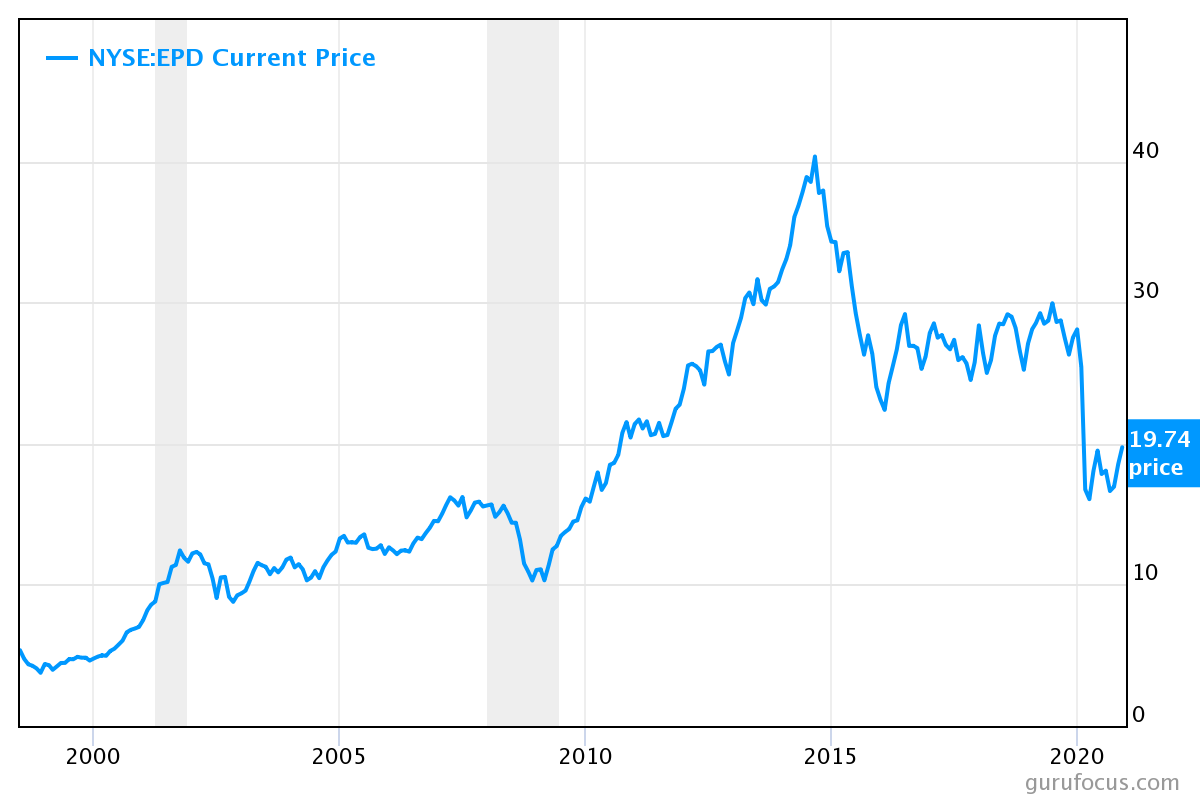

For such a boring, predictable company, EPD’s stock price has been anything but boring and predictable over the past decade.

Click to Enlarge

EPD became a hot stock in the low-yield years following the 2008 meltdown. Then — as now — short-term interest rates were pegged at zero, and long-term bond yields crawled along near all-time lows. In turn, EPD’s high and consistent quarterly distribution (dividend) made it wildly attractive to income investors desperate for yield.

Between the bottom in 2008 and the top in late 2014, EPD stock rose by more than a factor of four as investors tripped over themselves to get into the pipeline space. It helped that the fracking story was still new at the time and gave the pipeline operators a growth story.

Overall, it was too much too fast. The great fracking boom led to a massive oversupply of crude oil, which in turn led to widespread weakness across the energy patch. Banks became a lot more reluctant to lend, which forced pipeline operators across the board to depend more on internal financing. This meant less cash for distributions, of course, and many of EPD’s peers were forced to slash their payouts.

Enterprise Products, because of its conservative profile, weathered the storm just fine. EPD never cut its distribution. In fact, it continued to raise it, as it has for the past 21 consecutive years. EPD has raised its payout at a 6% annualized clip over its more than two decades as a public company. You could set your watch to it.

After the 2015 rout, EPD settled into a stable trading range. This held until the 2020 bear market upset the applecart. Energy stocks were obliterated in 2020, even blue chips like EPD that continued to plod along with no real difficulties. It was a classic case of the baby being thrown out with the bathwater. And herein lies our opportunity.

If Enterprise merely returns to pre-2020 levels, we’re looking at 50% capital gains. And if you want to see why I think those kinds of gains are likely, let’s return to EPD’s yield.

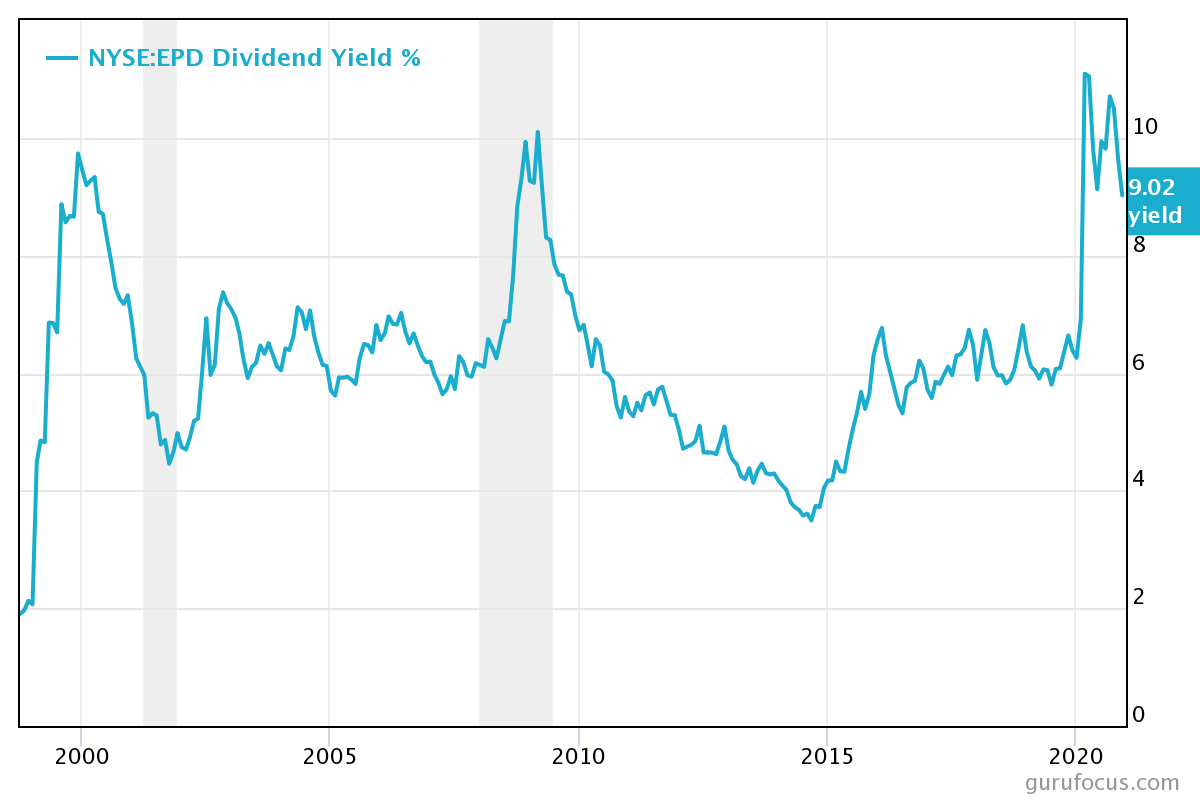

Click to Enlarge

At current prices, EPD yields an absurd 9%. Over the course of its life as a public company, it’s only traded at a yield that high twice, in the very late 1990s and during the 2008 meltdown. And I would emphasize that the yield is even more absurdly high today because bond yields are lower across the entire yield curve today.

Normally, a 9% yield is cause for concern. It implies that Wall Street expects the payout to be cut. But EPD pays out only 68% of its cash flow from operations, and its cash position was strong enough in 2020 to do a share buyback of 8.3 million units. I don’t pretend to know what 2021 will bring us, but I can be certain that a distribution cut by EPD is not in the cards.

Nature hates a vacuum, and safe 9% yields don’t stick around for long. Investors will gravitate to EPD’s market-beating yield, pushing the shares higher. Between the yield itself and the capital gains, I expect that as the shares bounce back to a more normal range, we could very easily see total returns of 40% to 60% in 2021.

And all of this in what may be the most boring stock on the New York Stock Exchange. Boring is beautiful!

On the date of publication, Charles Sizemore has a long positions in EPD and KMI.

Charles Sizemore, CFA is the principal of Sizemore Capital Management, a registered investment adviser based in Dallas, Texas specializing in income and retirment strategies.