Churchill Capital IV (NYSE:CCIV), a SPAC (special purpose acquisition company) with an impending merger with Arizona-based electric vehicle company Lucid Motors looks undervalued. In the past several weeks CCIV stock has fallen alongside the market. As a result, I now believe that CCIV stock is 19% undervalued.

Since my last article on Lucid Motors and the SPAC merger, CCIV has dropped roughly $7 or about 23%. This is the main reason why I believe that the stock is worth $27.45, almost a third more than the March 31 price of $23.05. This is based on calculations of the company’s comp value.

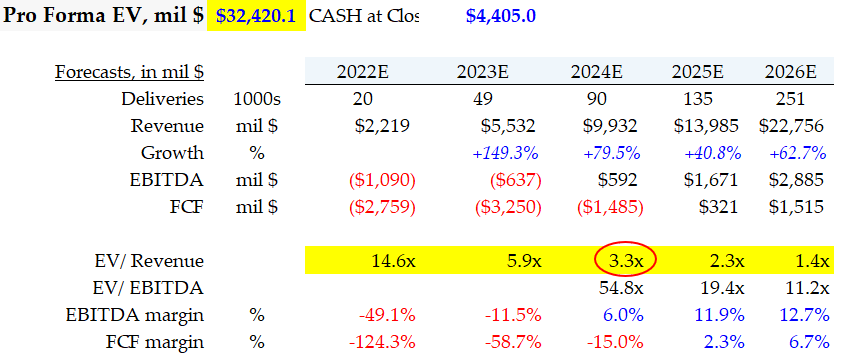

The pro forma market capitalization is now $36.8 billion. This is because the CCIV slide presentation (page 62) indicates there are 1,599 million shares outstanding.

Moreover, $4.4 billion in cash will be available to Lucid Motors at the closing of the SPAC merger. This implies that the enterprise value (EV) will be $32.4 billion.

Lucid Motors’ Pro Forma Target Value

Lucid expects to manufacture 365,000 electric luxury sedans (called the Lucid Air) per year starting with a production ramp-up in 2022. Revenue will be $2.2 billion and grow from there, assuming there is continued demand for these luxury EVs. The company recently announced it had sold out of preorders for its high end model.

Keep in mind that Lucid will be competing directly against Tesla (NASDAQ:TSLA) at this end of the EV market. And Tesla already has a huge lead over CCIV and every other EV car maker.

Revenue for 2024 is forecast to be $9.9 billion and deliveries of 90,000 Lucid Airs. Based on this CCIV stock trades for just 3.3 times EV-to-Sales, as you can see in the table on the right.

Click to Enlarge

This is the result of dividing the pro forma enterprise value (EV) of $32.4 billion as of today (Mar. 31) by the forecast $9.9 billion in revenue. This 3.3 EV-to-sales multiple is very cheap and is the reason I say this stock is now undervalued.

The table also shows that Lucid Motors expects to make EBITDA margins of 6% in 2024, rising to 11.9% in 2025 and 12.9% in 2026.

Lucid Motors expects to be free cash flow positive by 2025. According to the company’s projections, revenue should grow 149% in 2023 and 79% in 2024. This also explains why the stock appears cheap by 2024.

Click to Enlarge

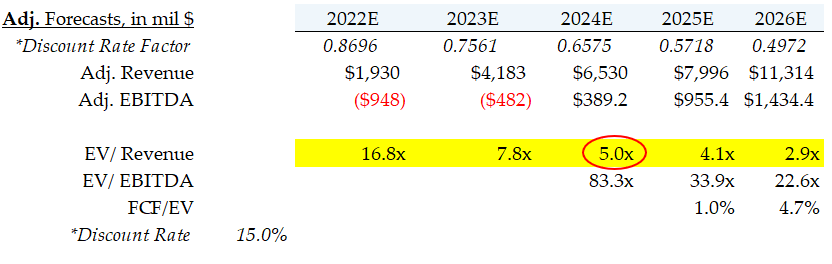

However, I decided to lower the revenue estimates in the future by adjusting them by a 15% discount rate. You can see this in the table at the right.

For example, instead of $9.9 billion in revenue in 2024, the present value of that figure today at a 15% discount rate is $6.5 billion. You can see in the table that lowers the valuation metric to 5.0 EV-to-Sales.

What CCIV Stock Is Really Worth

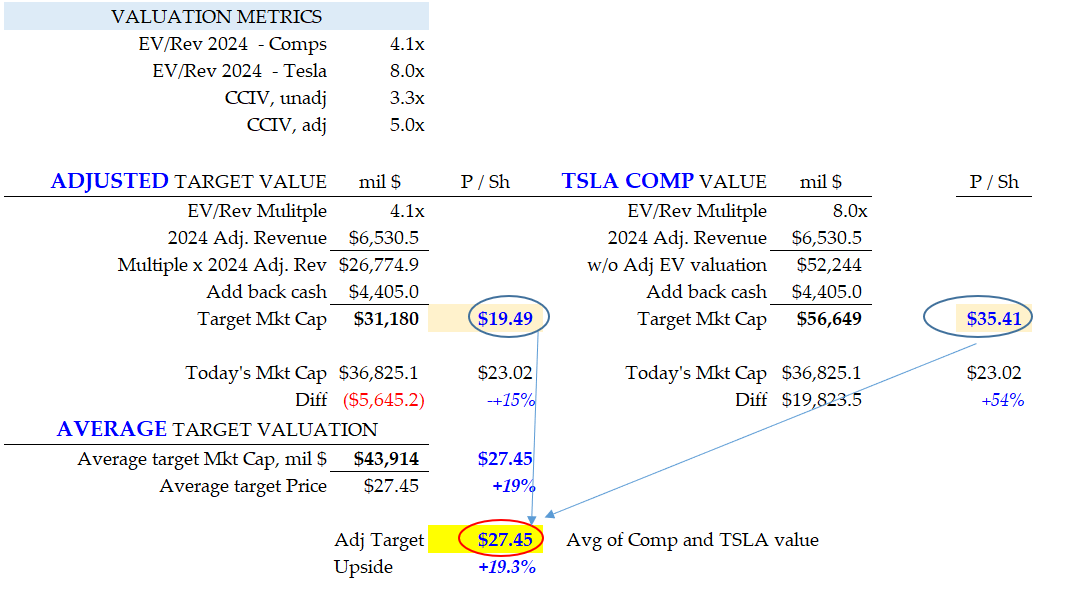

Using the same methodology as I did in my last article, we can compare Lucid with its peers and set its target value accordingly.

Compared to other EV stocks CCIV is cheap at 3.3 times EV-to-sales. However, at 5.0 times sales on a risk-adjusted basis, CCIV stock is overvalued. For example, for 2024, the median enterprise value-to-sale multiple of its peers is 4.1 times. according to the slide presentation (page 63).

Click to Enlarge

However, since Lucid Air is going to compete directly with Tesla, I also average in the Tesla valuation with the comp price to determine the CCIV stock target value.

Right now, Tesla stock is at about 8 times EV-to-sales. In my last article, I used 70% of this figure, but I think now given the lower valuation it is ok to use 100% of the Tesla multiple.

As a result, the table above shows that the comp value at 4.1 times discounted 2024 sales is $19.49 per share. But using the Tesla multiple, CCIV stock should be at $35.41. The average of these two is $27.45, 19% above today’s price.

What To Do With CCIV Stock

Assuming that Lucid Motors matches its own forecast, it is worth somewhere between $27.45 and $35.41. This represents gains of at least 19% to 54% above today’s price (Mar. 31) of $23.05 per share.

So far there are no analysts covering this SPAC stock, and that likely won’t change until the merger closes. They will have a much more detailed analysis and valuation methodology. What I have put together is very simple, but sometimes a simple model is all you need to get a bearing on where a stock’s value lies.

Look for CCIV stock to move up once the merger closes. This might be a good opportunity to acquire cheap shares of the EV maker.

On the date of publication, Mark R. Hake holds a long position in Tesla (TSLA).

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.